Volatility determines how much profit—or loss—a trader can experience within a given timeframe. Some currency pairs swing hundreds of pips in a single session, while others barely move 30. Understanding which pairs exhibit the highest price fluctuations and why they behave this way separates disciplined traders from those who blow accounts chasing movement without preparation.

What Makes Currency Pairs Volatile

Currency pair volatility stems from a combination of structural and event-driven factors. Liquidity plays a foundational role: pairs with fewer participants and lower trading volumes experience sharper price swings when large orders hit the market. A $10 million trade in EUR/USD barely registers, but the same order in USD/TRY can shift the market several percentage points.

Economic instability amplifies volatility. Countries experiencing high inflation, uncertain monetary policy, or fiscal imbalances see their currencies react violently to news releases. Turkey's lira, for example, has experienced double-digit intraday swings during periods of central bank intervention or policy announcements that surprised markets.

Interest rate differentials create carry trade dynamics that magnify reactions. When a central bank signals an unexpected shift in policy stance, traders unwind positions rapidly. The Reserve Bank of New Zealand's surprise rate decisions have historically caused 150+ pip moves in NZD/USD within minutes.

Geopolitical events inject unpredictable volatility. Elections, trade disputes, military conflicts, and diplomatic breakdowns trigger rapid repricing. The British pound saw extraordinary volatility during Brexit negotiations, with GBP/USD moving 400+ pips in single sessions on procedural votes.

Market participation levels vary by session. The overlap between London and New York sessions (8 AM–12 PM EST) concentrates the highest volume and volatility for most pairs. Asian session trading in EUR/USD might show 40-pip ranges, while the same pair moves 120 pips during European hours.

High volatility currency characteristics include: exposure to commodity prices (CAD, AUD, NOK), emerging market status (MXN, ZAR, BRL), small economy size relative to global capital flows (NZD, SEK), and recent history of central bank intervention (CHF, JPY during specific periods).

Author: Ethan Blackwell;

Source: martinskikulis.com

How Volatility Is Measured in Forex

Traders use several methods to quantify and compare currency pair volatility. The most common approach examines historical price movement over defined periods, while more sophisticated techniques incorporate statistical models and derivative pricing.

Measuring currency pair volatility requires standardized metrics because different pairs trade at different price levels. A 100-pip move means something entirely different for GBP/JPY (trading near 190.00) versus EUR/USD (trading near 1.0500). Percentage-based measurements and normalized indicators solve this comparison problem.

Historical volatility calculations analyze past price ranges. Traders measure the standard deviation of returns over 20, 50, or 100 periods to understand typical movement patterns. A pair with annualized volatility of 12% experiences roughly twice the price swings of one with 6% volatility.

Using ATR to Compare Currency Pairs

The Average True Range (ATR) indicator provides the most practical volatility measurement for forex traders. ATR in forex pairs calculates the average of true ranges over a specified period—typically 14 days. The true range accounts for gaps between sessions by measuring the greatest of: current high minus current low, absolute value of current high minus previous close, or absolute value of current low minus previous close.

ATR values appear in the quote currency's pips. GBP/JPY with an ATR of 180 means the pair averages 180 pips of movement per day over the past 14 sessions. Comparing ATR across pairs reveals relative volatility regardless of price level.

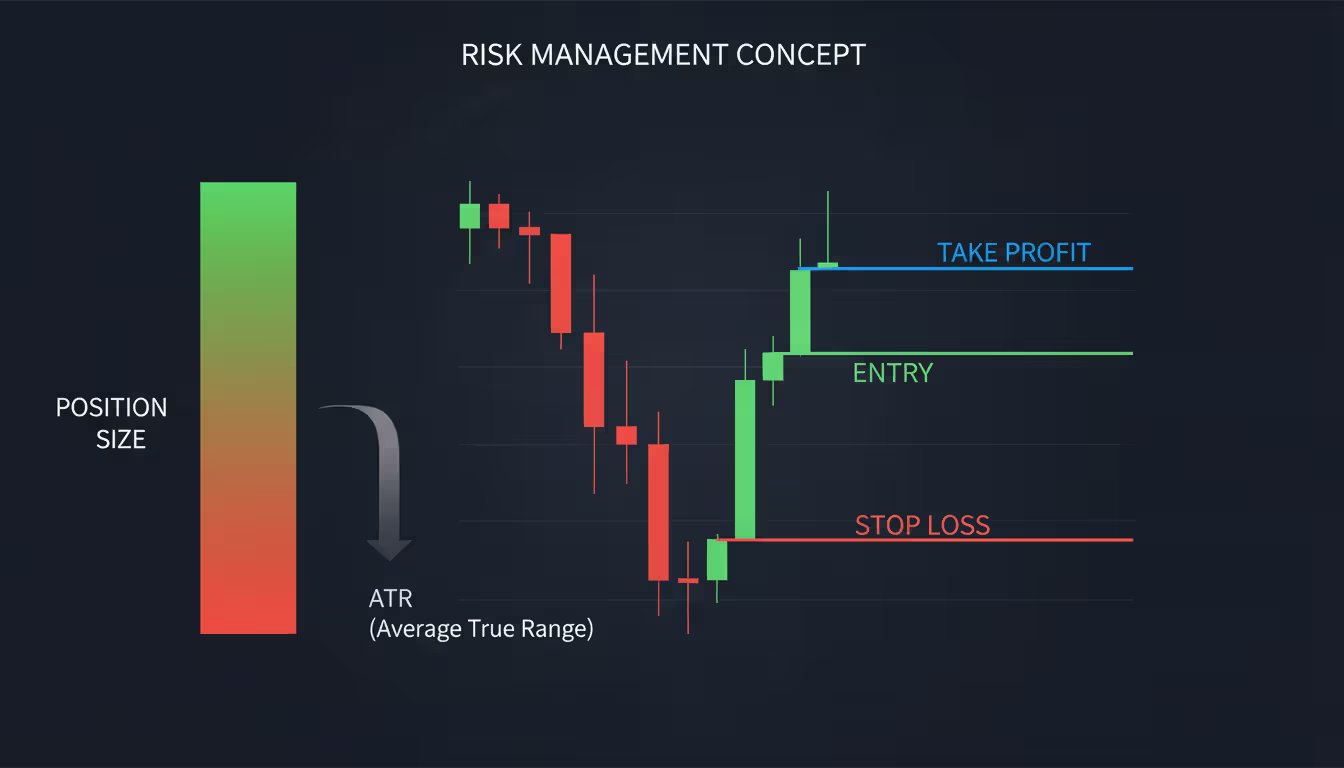

Traders adjust position sizes based on ATR. A strategy risking 50 pips on EUR/USD (ATR 70) requires different position sizing than the same 50-pip risk on GBP/JPY (ATR 180). The volatile pair needs smaller lot sizes to maintain equivalent dollar risk.

Daily Average Pip Range by Pair

Daily average pip ranges provide quick volatility comparisons. Major pairs like EUR/USD typically range 70–90 pips daily during normal conditions, expanding to 120+ during high-impact news. GBP/USD shows 100–130 pip averages, while GBP/JPY often exceeds 150 pips.

Exotic pairs dwarf these figures. USD/TRY can move 300–500 pips daily during calm periods and thousands of pips during currency crises. USD/ZAR frequently ranges 200+ pips, with volatility spiking around South African economic releases or political developments.

Time of day dramatically affects ranges. EUR/USD might move 20 pips during Tokyo session, 60 pips during London morning, and another 50 pips during New York overlap. Traders tracking hourly volatility patterns identify optimal entry windows.

Major Currency Pairs With High Volatility

The major currency category includes the most liquid pairs, but several exhibit substantial volatility despite tight spreads and deep markets. These pairs offer the best combination of movement and tradability for active traders.

GBP/JPY consistently ranks as the most volatile major pair. The combination of the pound's sensitivity to UK economic data and the yen's safe-haven flows creates explosive moves. Daily ranges of 150–200 pips are standard, with 300+ pip days occurring during risk-off events or Bank of England announcements. The pair trends strongly when established, making it popular for swing traders who can handle the swings.

GBP/USD delivers substantial volatility with better liquidity than GBP/JPY. The "cable" responds sharply to both US and UK data releases, often moving 100–150 pips daily. UK employment reports, inflation data, and Monetary Policy Committee decisions trigger immediate 80+ pip reactions. The pair's volatility increases during US-UK rate differential shifts.

Author: Ethan Blackwell;

Source: martinskikulis.com

USD/CAD volatility spikes during oil price swings and Canadian employment data. The loonie's 70% correlation with crude oil prices means energy market volatility directly transfers to the currency pair. When oil moves 5% in a day, USD/CAD often swings 120+ pips. The pair also reacts to US-Canada trade relationship developments and Bank of Canada policy surprises.

AUD/JPY combines Australian dollar commodity exposure with yen safe-haven dynamics. Risk-on sessions see aggressive rallies as traders buy higher-yielding AUD and sell defensive JPY. Risk-off reversals can erase 200 pips in hours. Chinese economic data adds another volatility layer since Australia's export economy depends heavily on Chinese demand.

Which currency pairs are most volatile among majors depends on current market conditions. During global risk events, yen crosses dominate. During commodity price swings, CAD, AUD, and NZD pairs lead. Sterling pairs spike around UK-specific events.

Exotic Pairs and Emerging Market Volatility

Exotic currency pair volatility operates on a different scale than major pairs. These crosses involving emerging market currencies experience structural volatility from economic instability, political risk, lower liquidity, and wider spreads that amplify price swings.

USD/TRY exemplifies extreme volatility in emerging market currencies. Turkey's history of high inflation, unconventional monetary policy, and geopolitical tensions creates an environment where 5–10% daily moves occur during crisis periods. The pair traded near 7.00 in early 2021, then surged past 32.00 by late 2024 before settling around 28.00 in 2026. Intraday swings of 500+ pips are routine during Turkish central bank decisions or political developments.

Liquidity issues magnify every move. A $5 million order in EUR/USD executes without visible impact, but the same size in USD/TRY can push the market 50 pips. Spreads widen to 20–50 pips during volatile periods, making precise entries nearly impossible. Overnight gaps of 200+ pips occur after weekend developments.

USD/ZAR reflects South African economic challenges and global risk sentiment. The pair ranges 150–250 pips daily under normal conditions, expanding to 400+ during emerging market selloffs or South African political uncertainty. Load-shedding energy crises, mining sector strikes, and fiscal policy debates all trigger sharp moves. Correlation with gold prices adds another volatility dimension.

Author: Ethan Blackwell;

Source: martinskikulis.com

USD/MXN responds to US-Mexico trade relations, oil prices, and Federal Reserve policy. The peso's sensitivity to US interest rate expectations creates volatility around FOMC meetings, often producing 150+ pip swings. Nearshoring trends and manufacturing data from both countries drive medium-term volatility. The pair typically ranges 100–180 pips daily.

USD/BRL volatility stems from Brazil's commodity exposure, fiscal challenges, and political cycles. The real experiences dramatic swings around Brazilian central bank decisions and presidential elections. Daily ranges of 200+ pips are common, with crisis periods seeing 500+ pip moves. Wide spreads (often 15–30 pips) and limited trading hours outside São Paulo sessions create execution challenges.

Volatility in emerging market currencies correlates strongly during global risk events. When the Federal Reserve signals aggressive tightening or geopolitical tensions escalate, capital flows out of all emerging markets simultaneously. USD/TRY, USD/ZAR, and USD/BRL often move in the same direction with amplified volatility.

Low Volatility Currency Pairs and When to Trade Them

Not every trading strategy benefits from wild price swings. Low volatility currency pairs suit range-bound strategies, carry trades, and traders who prefer predictable movement patterns with smaller stop-loss requirements.

EUR/CHF historically exhibited minimal volatility due to the Swiss National Bank's euro peg (until its dramatic removal in 2015). Post-peg, the pair still shows relatively contained ranges of 40–60 pips daily. The economic similarity between the Eurozone and Switzerland, combined with their trade relationship, limits divergence. Traders use EUR/CHF for range strategies, selling resistance and buying support with tight stops.

EUR/GBP moves slowly despite both currencies' individual volatility against the dollar. The pair averages 50–70 pips daily because UK and Eurozone economic cycles often align. Both economies trade heavily with each other, and their central banks face similar inflation and growth challenges. The pair trends gradually rather than spiking, making it suitable for position traders who hold for weeks.

AUD/NZD shows contained volatility because both economies share commodity exposure, geographic proximity, and similar central bank policies. Daily ranges of 40–60 pips are typical. The pair responds to relative economic performance between Australia and New Zealand rather than global risk sentiment. Dairy price changes (affecting NZD) versus iron ore and coal prices (affecting AUD) drive gradual trends.

Low volatility pairs reduce emotional trading pressure. A 30-pip stop-loss provides reasonable protection on EUR/CHF, while the same stop on GBP/JPY gets hit by normal market noise. Beginners often find low volatility pairs easier to manage psychologically.

However, low volatility creates trade-offs. Profit potential per trade is smaller, requiring larger position sizes to achieve meaningful returns. Spreads consume a higher percentage of the average daily range—a 2-pip spread on a 50-pip range pair costs 4% of potential profit, while the same spread on a 150-pip range pair costs only 1.3%.

Trading Strategies for High Volatility Pairs

High volatility currency pairs demand different approaches than stable pairs. The same strategies that work on EUR/CHF often fail spectacularly on USD/TRY. Risk management, timing, and position sizing require adjustment.

Position sizing should scale inversely with volatility. If your risk model allows 100,000 units on EUR/USD (ATR 70), the same risk on GBP/JPY (ATR 180) requires roughly 39,000 units. Many traders ignore this principle and use identical lot sizes across pairs, resulting in outsized losses when volatile pairs move against them.

Stop-loss placement must account for normal volatility. Setting a 30-pip stop on GBP/JPY guarantees getting stopped out by routine market noise. A rule of thumb: place stops at 1.5–2.0 times the pair's ATR to survive normal fluctuations while protecting against genuine reversals. For GBP/JPY with 180 ATR, that means 270–360 pip stops—which requires proportionally smaller position sizes.

Author: Ethan Blackwell;

Source: martinskikulis.com

Session timing dramatically affects success rates. Trading GBP/USD during Asian session produces frequent false breakouts because low liquidity allows small orders to push price temporarily. The same breakout strategy during London session has higher follow-through probability because volume confirms moves.

Breakout strategies suit high volatility pairs during news releases. GBP/JPY often trends 150+ pips after breaking key levels on strong UK data. Place entry orders above resistance and below support with stops beyond the recent range. The volatility provides profit potential that justifies the wider stops.

Range strategies work during low-volume sessions. Even volatile pairs consolidate during off-hours. Identify 50–80 pip ranges during Asian session on GBP/USD, sell the top, buy the bottom, and exit before London open. The strategy fails if you hold through session transitions when volatility returns.

Correlation awareness prevents overexposure. Going long GBP/USD and GBP/JPY simultaneously doubles your GBP exposure. If sterling collapses on unexpected news, both positions lose simultaneously. High volatility amplifies correlation risk.

Common Mistakes When Trading Volatile Currencies

Volatility is neither good nor bad—it's simply a characteristic that must match your trading style and risk tolerance. The biggest mistake traders make is choosing pairs based on profit potential alone without considering whether their account size and psychological makeup can handle the inevitable drawdowns that come with high volatility instruments

— Kathy Lien

Overleveraging kills more accounts than any other mistake. A trader using 50:1 leverage on USD/TRY during a 5% adverse move loses 250% of capital. Volatile pairs require conservative leverage—10:1 or less—to survive normal fluctuations. The temptation to use high leverage because "the pair is definitely going up" ignores the reality that volatile pairs spike against you before trending your direction.

Ignoring spread costs destroys profitability on exotic pairs. USD/ZAR with a 15-pip spread means you start every trade down 15 pips. If your average winner is 80 pips and average loser is 60 pips, the spread consumes 19% of wins and 25% of losses, dramatically shifting your required win rate. Many strategies profitable on EUR/USD fail on exotics purely due to spread costs.

Trading during news without preparation is gambling, not trading. A trader who happens to be long GBP/JPY when the Bank of England surprises with a 50-basis-point hike might profit 200 pips—or lose 200 pips if the hike disappoints expectations. News volatility is non-directional chaos for the first 60 seconds. Either exit before major releases or wait 15 minutes for initial volatility to settle.

Misjudging correlation leads to unexpected losses. AUD/USD and NZD/USD correlate 85%+ most of the time, but during Australia-specific news, the correlation breaks. Traders hedging AUD exposure with NZD positions discover their hedge fails exactly when needed.

Poor timing—entering trades at session ends—guarantees getting caught in overnight gaps. Entering USD/TRY long at 4 PM EST means holding through 16 hours of illiquid Asian and European sessions where news can gap the pair 200 pips against you before you can react.

Chasing moves after they've already happened is expensive on volatile pairs. GBP/JPY rallies 180 pips in two hours, and FOMO drives a trader to buy at the high. The pair immediately retraces 100 pips, stopping them out. Volatile pairs mean-revert aggressively after extended runs. Wait for pullbacks or skip the trade entirely.

Average Daily Volatility Comparison by Currency Pair

Currency Pair

Average Daily Pip Range

ATR (14-period)

Volatility Classification

Typical Spread

GBP/JPY

150–200

180

Very High

2–3 pips

GBP/USD

100–140

110

High

1–2 pips

USD/TRY

300–600

450

Extreme

20–50 pips

AUD/JPY

120–160

140

High

2–3 pips

USD/ZAR

180–280

220

Very High

10–20 pips

USD/CAD

80–120

95

Medium-High

1–2 pips

EUR/USD

70–95

75

Medium

0.5–1 pip

USD/MXN

120–200

160

High

8–15 pips

EUR/GBP

50–75

60

Low-Medium

1–2 pips

EUR/CHF

40–65

50

Low

1–2 pips

AUD/NZD

45–70

55

Low

2–4 pips

USD/JPY

70–100

80

Medium

1–2 pips

Data represents typical conditions during 2026; volatility increases significantly during crisis periods or major news events.

Frequently Asked Questions

What is the most volatile currency pair to trade?

USD/TRY consistently ranks as the most volatile major currency pair available to retail traders, with daily ranges frequently exceeding 300 pips and crisis periods seeing 1,000+ pip moves. Among liquid major pairs, GBP/JPY exhibits the highest volatility with 150–200 pip average daily ranges. The choice depends on your broker's offerings and risk tolerance—exotic pairs offer extreme volatility but wider spreads and execution challenges.

Are volatile currency pairs better for day trading?

Volatile pairs provide more intraday profit opportunities because they move enough to justify the transaction costs of entering and exiting within a session. A day trader needs 50+ pip moves to profit after spreads; EUR/CHF rarely provides this, while GBP/USD frequently does. However, volatile pairs also trigger more stop-losses and require larger capital to maintain proper position sizing. They're better for experienced day traders with solid risk management, not beginners.

How does volatility affect forex spreads?

Spreads widen proportionally to volatility, especially during news releases and low-liquidity sessions. EUR/USD might trade at 0.5 pips during calm London hours but spike to 3–5 pips during NFP releases. Exotic pairs show extreme spread expansion—USD/TRY spreads can balloon from 25 pips to 80+ pips during Turkish central bank announcements. This spread expansion can stop you out even if price ultimately moves your direction, making entries during peak volatility particularly risky.

Which currency pairs have the lowest volatility?

EUR/CHF, EUR/GBP, and AUD/NZD consistently show the lowest volatility among tradable pairs, with daily ranges typically between 40–70 pips. These pairs involve economically similar countries or regions with aligned central bank policies. The low volatility makes them suitable for range trading strategies and traders who prefer smaller stop-losses, though profit potential per trade is correspondingly limited.

What time of day are currency pairs most volatile?

Currency pairs show highest volatility during their primary geographic trading sessions. EUR/USD peaks during the London-New York overlap (8 AM–12 PM EST) when both European and US traders are active. GBP/USD volatility concentrates during London session (3 AM–12 PM EST). USD/JPY sees increased movement during Tokyo session (7 PM–4 AM EST) and New York session. The first hour after major economic releases (typically 8:30 AM EST for US data) produces the most extreme volatility spikes.

Is high volatility good or bad for forex traders?

High volatility is neutral—its value depends entirely on your trading strategy, risk management, and psychological tolerance. Volatility creates profit opportunities by moving price enough to overcome transaction costs, benefiting active traders with solid risk controls. It simultaneously increases the probability of stop-loss triggers and demands larger capital for proper position sizing. Traders who match their strategy to volatility levels succeed; those who fight against a pair's natural volatility characteristics struggle regardless of market direction.

Volatility defines the forex trading experience more than any other characteristic. The difference between a 50-pip daily range and a 200-pip range determines position sizing, stop-loss placement, profit targets, and psychological stress levels. GBP/JPY and USD/TRY offer dramatically different trading experiences than EUR/CHF, despite all being currency pairs.

Successful traders match pair selection to their strategy requirements. Scalpers need volatile pairs during high-volume sessions to generate multiple opportunities. Position traders might prefer moderate volatility that trends consistently without stopping them out on noise. Range traders seek low volatility pairs that respect technical levels.

The measurement tools—ATR, daily pip ranges, historical volatility—provide objective comparisons that prevent emotional pair selection. A trader who calculates that their 2% risk rule allows only 10,000 units on GBP/JPY but 35,000 units on EUR/USD makes informed decisions rather than guessing.

Risk management must scale with volatility. The same 50-pip stop-loss represents conservative protection on EUR/USD but reckless exposure on USD/TRY. Position sizing, leverage limits, and correlation awareness become critical when trading pairs that can move 300 pips in an afternoon.

The exotic pairs—Turkish lira, South African rand, Mexican peso—offer extraordinary profit potential alongside extraordinary risk. Their structural characteristics (wide spreads, limited liquidity, economic instability) make them unsuitable for most retail traders, regardless of the tempting pip ranges. The few traders who succeed with exotics typically specialize exclusively in those markets, developing expertise that casual traders cannot match.

Ultimately, understanding which currency pairs are most volatile and why they behave that way allows you to build a trading approach that works with market characteristics rather than against them. The pair doesn't determine success—the match between pair volatility and your strategy does.

The purchasing power of the US dollar has declined roughly 98% since 1913. While gradual erosion differs from collapse, understanding which assets retain value during currency crises provides practical preparation for scenarios that have played out repeatedly throughout monetary history

The forex market processes $7.5+ trillion daily, yet a handful of pairs dominate volume. Learn which currency pairs traders prefer, why EUR/USD captures 24% of global transactions, and how liquidity, spreads, and volatility shape pair selection for different trading strategies

Major currencies represent the backbone of global foreign exchange markets. These monetary units from economically stable nations account for over 90% of daily forex turnover. Understanding which currencies dominate trading, how they're classified, and why they matter helps traders and investors navigate international markets

Discover the full scope of world currencies in 2026—from the 180+ recognized legal tenders to the major players in forex markets. Learn currency names by country, understand fiat vs. digital money, and get actionable advice for travel and international business

The content on this website is provided for general informational and educational purposes only. It is intended to explain concepts related to Forex (FX) trading, currency markets, leverage, hedging, and risk management.

All information on this website, including articles, guides, and examples, is presented for general educational purposes. Forex trading carries significant risk, and outcomes may vary depending on market conditions, leverage, and individual decisions.

This website does not provide financial, investment, or trading advice, and the information presented should not be used as a substitute for consultation with qualified financial professionals.

The website and its authors are not responsible for any errors or omissions, or for any outcomes resulting from decisions made based on the information provided on this website.