Fading US dollar bills in foreground with gold bars, a modern house, and stock market charts in the sharp background, symbolizing wealth protection against currency devaluation

The purchasing power of the US dollar has declined roughly 98% since the Federal Reserve's creation in 1913. While that erosion happened gradually, the possibility of rapid devaluation—or even collapse—keeps many Americans awake at night. Understanding which assets retain value when currency crumbles isn't just academic curiosity; it's practical preparation for scenarios that have played out repeatedly throughout monetary history.

Most people confuse steady inflation with currency collapse. The difference matters enormously when you're deciding where to park your savings. A 3% annual inflation rate eats away at purchasing power over decades. A collapse can wipe out wealth in months or even weeks.

This guide examines which assets historically preserve wealth during dollar weakness, what mistakes to avoid, and how to build a balanced approach that doesn't require you to become a doomsday prepper or abandon conventional investments entirely.

What Does a Dollar Collapse Actually Mean?

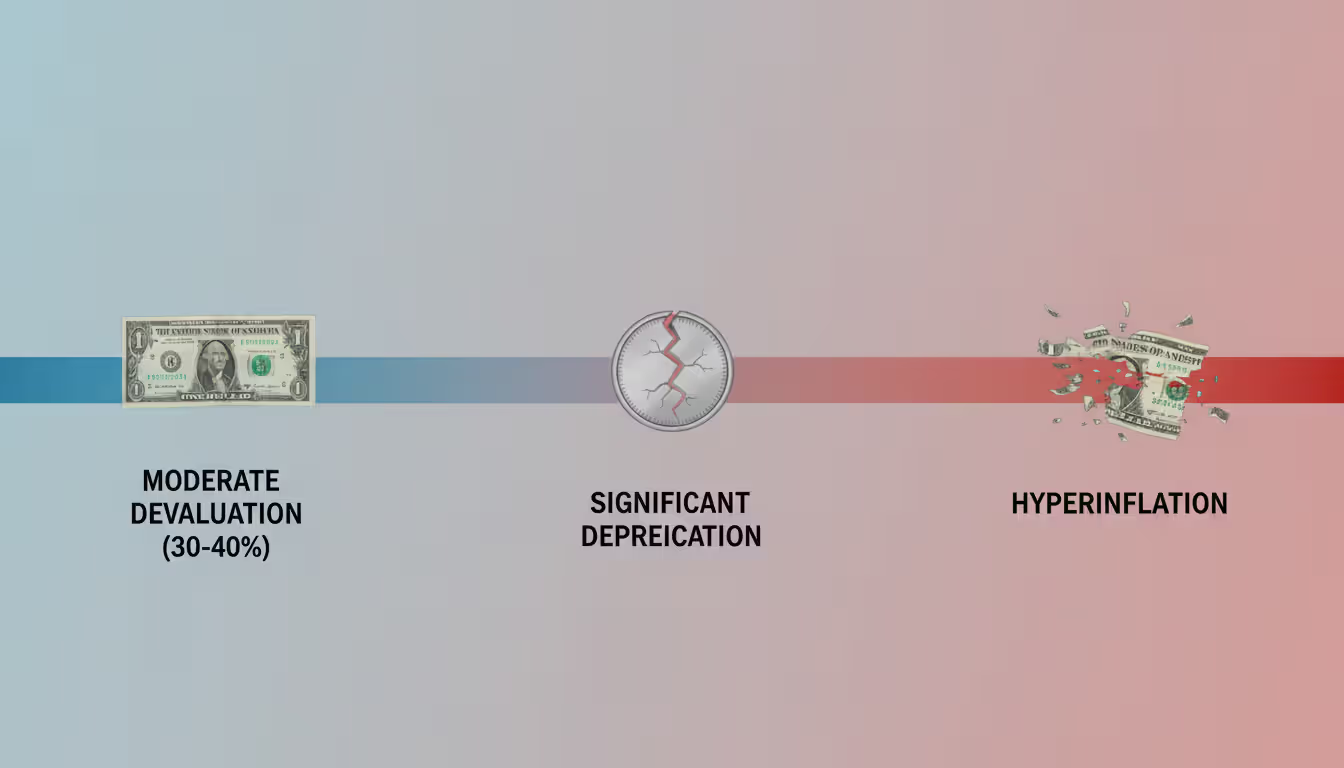

A dollar collapse doesn't necessarily mean the currency becomes worthless overnight. The term encompasses several distinct scenarios, each with different implications for your financial security.

Dollar collapse scenarios range from gradual devaluation to catastrophic loss of confidence. At the mild end, you might see the dollar lose 30-40% of its value against other major currencies over a few years—similar to what happened between 2001 and 2008. At the extreme end, hyperinflation could make the currency nearly worthless for transactions, though this remains unlikely for a major economy with diverse production capacity.

Reserve currency loss represents a middle-ground scenario that worries economists more than sudden hyperinflation. The dollar currently accounts for roughly 58% of global foreign exchange reserves as of 2026, down from nearly 72% in 2001. If that share drops below 40%, the US would lose significant economic leverage. Foreign governments and corporations would hold fewer dollars, reducing demand and driving down value. This wouldn't happen overnight—the British pound's decline from reserve status took decades—but the transition period creates substantial uncertainty.

Author: Olivia Kensington;

Source: martinskikulis.com

The usd safe haven status depends on global confidence that the US government will honor its debts and maintain political stability. That confidence has wobbled before—during the 1979 energy crisis, the 2008 financial meltdown, and the 2023 debt ceiling standoff. Each time, the dollar eventually recovered because investors had nowhere better to go. But "eventually" can mean years of poor performance, and past recovery doesn't guarantee future results.

A realistic collapse scenario involves sustained high inflation (8-15% annually) combined with loss of reserve currency dominance. Your grocery bill doubles every five years. Imported goods become luxury items. Savings accounts lose half their purchasing power in a decade. This isn't Mad Max territory, but it fundamentally reshapes middle-class financial security.

How Dollar Weakness Affects Your Purchasing Power

When the dollar weakens, you notice it first at the gas pump and grocery store. Import prices rise immediately because foreign suppliers want more dollars to equal the same amount of their currency. That iPhone assembled in China? The car parts from Mexico? The coffee from Colombia? All become more expensive before domestic inflation even kicks in.

Dollar devaluation effects ripple through the economy in stages. Initially, import-dependent sectors see price spikes. Then domestic producers raise prices because they can—their goods look relatively cheaper than imports, even with a markup. Wages eventually follow, but they lag behind prices by months or years. During that lag, your real purchasing power drops.

The strong dollar vs weak dollar dynamic creates winners and losers. A strong dollar benefits consumers through cheap imports and affordable foreign travel. It hurts exporters who struggle to sell American-made goods abroad. A weak dollar does the opposite: exporters thrive, but consumers pay more for everything from electronics to prescription drugs.

Consider a practical example: In 2014, one dollar bought 110 Japanese yen. By 2022, it bought 150 yen—a strong dollar. Your Tokyo vacation cost less. But in 2008, one dollar bought only 95 yen. That weakness helped Boeing sell more planes to Japanese airlines because the price in yen looked attractive.

Savings erosion accelerates during dollar weakness. A savings account paying 2% interest loses purchasing power when inflation runs at 6%. You're earning nominal returns but suffering real losses. Retirees on fixed incomes get squeezed hardest—their Social Security checks buy less each month, and bond portfolios yield returns that don't keep pace with rising costs.

The psychological impact matters too. When people lose confidence in their currency, they change behavior. They spend rather than save, creating a self-fulfilling cycle of inflation. They hoard goods, creating artificial shortages. They seek alternative stores of value, from gold to foreign bank accounts to cryptocurrency. These individual rational decisions can collectively accelerate currency decline.

Physical Assets That Hold Value During Currency Crises

Tangible assets you can touch, use, or occupy provide the most intuitive protection against currency collapse. They have intrinsic utility independent of any government's promise.

Precious Metals: Gold and Silver

Gold has preserved wealth through every major currency crisis of the past 5,000 years. When the Roman denarius collapsed, gold retained value. When Weimar Germany printed marks into worthlessness, gold protected those who held it. When the dollar decoupled from gold in 1971, gold prices soared from $35 to over $800 per ounce by 1980.

The assets that protect against dollar weakness consistently include gold because it has no counterparty risk. A dollar bill represents a promise from the US government. A gold coin is simply gold—its value doesn't depend on anyone's creditworthiness.

Silver offers similar benefits with more industrial utility. Electronics, solar panels, and medical equipment require silver. This dual role as monetary metal and industrial commodity creates different price dynamics than gold. Silver tends to be more volatile—bigger gains during dollar weakness, but sharper drops during economic contractions when industrial demand falls.

Practical considerations matter when holding metals. Physical possession means storage and security costs. A home safe works for modest amounts; larger holdings might require bank safe deposit boxes or private vault services. Allocated storage—where you own specific bars or coins—costs more than unallocated, but you avoid counterparty risk if the storage company fails.

Gold ETFs and mining stocks provide easier liquidity but reintroduce counterparty risk. The ETF is only as good as its management and the actual gold backing it. Mining stocks give you leverage to gold prices but add company-specific risks like operational problems, political instability in mining regions, and management quality.

A rule of thumb: hold 5-15% of your portfolio in precious metals for currency crisis insurance. That's enough to matter if the dollar weakens substantially, but not so much that you miss out on growth if stocks and real estate continue performing well.

Author: Olivia Kensington;

Source: martinskikulis.com

Real Estate and Land

Property represents the oldest form of wealth preservation. You can live on it, farm it, rent it, or sell it. Even during severe currency crises, people need housing.

Real estate performs well during dollar devaluation for several reasons. Property values often rise with inflation—replacement costs increase, so existing buildings become more valuable. If you have a fixed-rate mortgage, inflation works in your favor. You repay the loan with devalued dollars while the property appreciates in nominal terms.

Location determines everything. Productive farmland retains value better than suburban office parks during economic turmoil. Housing in growing metros with diverse economies outperforms properties in declining industrial towns. Coastal areas face climate risks that might offset other advantages.

Foreign real estate adds geographic diversification. Property in Switzerland, Singapore, or New Zealand provides a hedge if US-specific problems drive dollar weakness. But cross-border ownership brings complications: unfamiliar legal systems, tax treaties, property management from afar, and potential capital controls during crises.

Raw land offers inflation protection without tenant headaches, but it generates no income and costs money for property taxes. Rental properties produce cash flow that typically rises with inflation, but they require active management or property manager fees that eat into returns.

Debt matters enormously. Fixed-rate mortgages become advantageous during inflation—you lock in low payments while rents rise. But variable-rate debt can destroy you if interest rates spike to combat currency weakness. The 1980s saw mortgage rates exceed 18% as the Federal Reserve fought inflation.

Essential Commodities and Supplies

Stockpiling basics makes sense up to a point. Six months of non-perishable food, basic medicines, household supplies, and tools provide security during supply chain disruptions that often accompany currency crises.

Energy deserves special attention. Gasoline storage requires proper containers and safety measures, but heating fuel, propane, or firewood for cold climates can be critical. Solar panels with battery backup provide energy independence, though the upfront cost takes years to recoup under normal conditions.

The mistake people make is over-accumulating. Fifty years of canned beans won't help if you need to relocate quickly. Supplies have carrying costs—storage space, spoilage risk, opportunity cost of capital tied up in goods rather than investments. Balance practical preparedness with financial flexibility.

Financial Instruments That Protect Against Dollar Devaluation

Paper assets and digital instruments offer advantages that physical goods can't match: liquidity, divisibility, and ease of rebalancing.

Foreign Currencies and Reserve Currency Alternatives

Holding currencies from countries with stronger fiscal positions provides direct protection against dollar-specific weakness. The Swiss franc, Norwegian krone, and Singapore dollar historically maintain value better than the dollar during global uncertainty.

Reserve currency alternatives increasingly include the Chinese yuan, though capital controls limit its usefulness for individual investors. The euro represents a large, liquid alternative, but the eurozone's own structural problems—aging demographics, southern European debt issues—create risks that sometimes mirror dollar concerns.

Currency diversification works best through foreign bond funds or money market accounts rather than cash under your mattress. You earn interest while holding the currency exposure. But exchange rate volatility cuts both ways. If the dollar strengthens unexpectedly, your foreign holdings lose value in dollar terms even if they're stable in their home currency.

Special Drawing Rights (SDRs) from the International Monetary Fund represent a basket of currencies—dollar, euro, yuan, yen, and pound. Individuals can't hold SDRs directly, but some funds provide exposure to similar currency baskets, reducing single-currency risk.

Inflation-Protected Securities

Treasury Inflation-Protected Securities (TIPS) adjust their principal value based on the Consumer Price Index. If inflation runs 5%, your TIPS principal grows 5%, and interest payments increase accordingly. When TIPS mature, you receive the inflation-adjusted principal or the original amount, whichever is higher.

TIPS provide government-guaranteed protection against measured inflation. The catch is "measured." If you believe official inflation statistics understate real price increases—and many economists argue they do—TIPS offer incomplete protection. The CPI calculation methodology has changed repeatedly, generally in ways that reduce reported inflation.

I Bonds offer similar inflation protection with different mechanics. They pay a fixed rate plus an inflation adjustment that resets every six months. Purchase limits ($10,000 per person annually through TreasuryDirect, plus $5,000 in paper bonds via tax refunds) make them suitable for modest savings but inadequate for large portfolios.

Corporate bonds with inflation-linked coupons exist but trade less frequently than TIPS. The credit risk of the issuing company adds another variable—you might get inflation protection but lose principal if the company defaults.

Cryptocurrency Considerations

Bitcoin advocates argue it represents "digital gold"—a fixed supply asset immune to government money printing. The 21 million bitcoin limit contrasts sharply with unlimited fiat currency creation. During 2020-2022, as governments worldwide printed money to combat pandemic economic damage, bitcoin prices surged from $7,000 to over $65,000.

But cryptocurrency volatility exceeds any traditional asset. Bitcoin dropped from $65,000 to $16,000 in 2022, then recovered to fluctuate between $40,000 and $90,000 through 2026. That instability makes it questionable as a stable store of value, even if long-term appreciation potential exists.

Regulatory uncertainty adds risk. Governments could restrict cryptocurrency exchanges, impose transaction taxes, or mandate reporting that eliminates privacy advantages. China banned cryptocurrency transactions entirely. The US has taken a more permissive approach through 2026, but that could change if authorities view crypto as enabling tax evasion or threatening monetary policy control.

Custody presents challenges. Self-custody through hardware wallets provides security but requires technical knowledge. Exchange custody is convenient but introduces counterparty risk—multiple exchanges have failed, taking customer funds with them. The FTX collapse in 2022 cost investors billions.

A balanced view: cryptocurrency might play a role in a diversified collapse-hedge portfolio, but treat it as a speculative position, not a core holding. Allocate only what you can afford to lose completely. The 1-3% portfolio allocation some advisors suggest for bitcoin captures upside if it succeeds without devastating your finances if it fails.

Author: Olivia Kensington;

Source: martinskikulis.com

Historical Examples of Dollar Devaluation and What Worked

Historical dollar devaluation episodes provide the best guide to asset performance during currency weakness. Three periods stand out for their lessons.

1971-1980: Nixon Shock and Stagflation

President Nixon ended dollar convertibility to gold in August 1971, effectively devaluing the currency. Through the 1970s, oil shocks and loose monetary policy created stagflation—simultaneous inflation and economic stagnation. The dollar lost roughly 50% of its purchasing power during the decade.

Gold exploded from $35 per ounce (the old fixed rate) to $850 by January 1980. Silver rose from $1.50 to $50. Commodities broadly outperformed. Real estate appreciated significantly in nominal terms, though high interest rates by decade's end created affordability problems.

Stocks struggled. The S&P 500 was essentially flat in nominal terms from 1970 to 1980, meaning substantial real losses after inflation. Bonds performed terribly—who wants to hold 5% bonds when inflation runs 10%? Cash lost purchasing power steadily.

2001-2008: Weak Dollar Period

Following the dot-com crash and 9/11 attacks, the Federal Reserve cut rates aggressively. The dollar declined about 40% against major currencies from 2001 to 2008. This period showed what drives dollar strength—or in this case, weakness. Low interest rates, growing trade deficits, and foreign central banks diversifying reserves all pressured the currency.

Gold tripled from around $250 to $1,000 per ounce. Foreign stocks in local currency terms outperformed US stocks significantly—emerging markets particularly benefited. Real estate boomed until 2006, though the subsequent crash had more to do with credit excess than currency issues. Commodities soared as China's growth drove demand while dollar weakness made them cheaper in other currencies.

US stocks provided positive returns but lagged foreign equities. Bonds offered modest protection through price appreciation as rates fell, but real returns after inflation were minimal.

2020-2022: Pandemic Money Printing

The COVID-19 pandemic triggered unprecedented fiscal and monetary stimulus. The Federal Reserve's balance sheet expanded from $4 trillion to $9 trillion in two years. Federal deficits exceeded $3 trillion annually. Many predicted dollar collapse.

Instead, the dollar initially strengthened as global investors fled to safety. By late 2020 through 2021, dollar weakness emerged. Gold rose but less dramatically than many expected, peaking around $2,070 in August 2020. Cryptocurrency surged—bitcoin's rise to $65,000 suggested some viewed it as a dollar alternative.

Real estate appreciated rapidly, driven partly by inflation expectations but also by low rates and pandemic-driven housing demand. Stocks soared despite currency concerns, with tech stocks leading. Commodities rallied strongly in 2021-2022.

This period illustrated that dollar weakness doesn't occur in isolation. Multiple factors—growth expectations, relative interest rates, geopolitical stability—interact in complex ways.

Asset Class

1971-1980 Performance

2001-2008 Performance

2020-2022 Performance

Gold

+2,330%

+280%

+45%

Real Estate

+150% (nominal)

+90% (peak)

+40%

S&P 500 Stocks

+17% (nominal)

+35%

+55%

10-Year Bonds

-20% (real)

+45%

-15%

Cash

-50% (real)

-30% (real)

-20% (real)

Note: Performance figures are approximate and represent total returns for the periods indicated. Real returns account for inflation; nominal returns do not.

Common Mistakes When Preparing for Dollar Weakness

Panic drives poor decisions. The fear of currency collapse tempts people into extreme positions that often backfire.

Over-concentration in one asset represents the most common error. Going all-in on gold feels safe when you're convinced the dollar will crash. But if the collapse doesn't materialize—or takes decades rather than years—you've sacrificed growth and income. Gold produced negative real returns from 1980 to 2000 as the dollar strengthened. Anyone who converted their entire portfolio to gold in 1980 spent twenty years watching stocks and real estate outperform.

Ignoring liquidity creates problems during actual crises. Farmland might preserve wealth beautifully, but you can't pay your mortgage with an acre of soybeans. You need some liquid assets—cash, money market funds, or easily sold securities—to handle unexpected expenses without forced sales at bad prices. The rule of thumb: maintain 6-12 months of living expenses in liquid form even while hedging against dollar weakness.

Timing the market proves nearly impossible. Currency moves unfold over years or decades with plenty of false starts and reversals. Trying to jump in and out of dollar hedges based on news headlines costs you in transaction fees and taxes while likely getting the timing wrong. The 2010s saw repeated predictions of imminent dollar collapse that never materialized. Those who sold stocks to buy gold in 2011 missed a decade-long bull market.

Author: Olivia Kensington;

Source: martinskikulis.com

Neglecting tax consequences turns paper gains into real losses. Precious metals held for under a year face ordinary income tax rates. Held longer, they're taxed as collectibles at up to 28%—higher than the long-term capital gains rate on stocks. Foreign currency gains are taxable. Cryptocurrency creates complex reporting requirements. Structure your collapse hedges in tax-advantaged accounts where possible, and consult a tax professional before making major moves.

Forgetting about income leaves you cash-poor even if asset values rise. Gold pays no dividends. Land without tenants generates no rent. During extended periods of dollar weakness, you still need to eat and pay bills. Balance appreciation-focused assets with income-producing ones—dividend stocks, rental properties, bonds—so you're not forced to sell holdings to fund living expenses.

Overlooking personal circumstances leads to inappropriate strategies. A 30-year-old with decades until retirement can tolerate more volatility and illiquidity than a 65-year-old living on savings. Someone with stable employment needs less emergency cash than a freelancer with irregular income. Geographic location matters—coastal property faces climate risks, while rural land offers fewer amenities. Customize your approach rather than following generic advice.

The dollar's role as the global reserve currency is not permanent. History shows that reserve currencies change over time—the Dutch guilder, British pound, and others all had their day. The question isn't if the dollar will lose its dominance, but when and how quickly. Diversification across asset classes and currencies isn't pessimism; it's prudent risk management based on historical precedent

— Jim Rickards

FAQ

Can the US dollar actually collapse completely?

Complete collapse—where the dollar becomes worthless for transactions—is extremely unlikely barring catastrophic political breakdown. The US has the world's largest economy, most powerful military, and deepest financial markets. Even significant devaluation differs from collapse. More realistic scenarios involve the dollar losing 30-50% of its value over several years or gradually losing reserve currency status while remaining functional for domestic transactions. Historical examples like the British pound show that former reserve currencies can decline substantially yet remain viable.

What triggers a loss of reserve currency status?

Reserve status depends on global confidence, liquidity, and lack of alternatives. Triggers include: sustained high inflation that erodes value; loss of political stability that raises default concerns; emergence of credible alternatives like a digital yuan or multi-currency system; excessive use of financial sanctions that motivate other countries to avoid dollar dependence; or massive debt accumulation that questions long-term solvency. The process typically unfolds over decades rather than months, giving attentive investors time to adjust.

Should I convert all my savings to gold?

No. Gold provides insurance against currency collapse but sacrifices growth and income. A 100% gold portfolio would have underperformed stocks and real estate over most multi-decade periods. Gold doesn't pay dividends, fund your retirement through regular distributions, or grow with economic productivity. Financial advisors typically recommend 5-15% precious metals allocation—enough to provide meaningful protection during dollar weakness without abandoning growth potential. Your specific allocation should reflect your age, risk tolerance, income stability, and other personal factors.

How much of my portfolio should protect against dollar weakness?

A balanced approach might allocate 20-40% of your portfolio to dollar-collapse hedges: 5-15% in precious metals, 5-10% in foreign currency exposure through international bonds or stocks, 5-10% in real assets like commodities or real estate beyond your primary residence, and potentially 1-3% in cryptocurrency as a speculative position. The remaining 60-80% stays in traditional investments—domestic stocks, bonds, and cash—which still perform adequately in moderate devaluation scenarios and provide liquidity. Adjust based on your personal situation and conviction level about dollar risks.

Are cryptocurrencies a safe hedge against dollar collapse?

Cryptocurrency remains too volatile and unproven to serve as a primary hedge. Bitcoin's 80%+ drawdowns and regulatory uncertainty make it unsuitable for wealth preservation, even if long-term potential exists. Unlike gold's 5,000-year track record, cryptocurrency has only 15 years of history, mostly during a period of dollar strength and declining interest rates. If you include crypto in your collapse-hedge strategy, limit it to a small speculative allocation you can afford to lose. Treat it as a high-risk/high-reward position rather than safe harbor.

What happened to people's wealth during past currency crises?

Outcomes varied dramatically based on asset allocation. During Weimar Germany's hyperinflation (1921-1923), those holding physical assets—real estate, businesses, commodities—preserved wealth, while cash and bond holders were wiped out. In Argentina's repeated currency crises, dollar-denominated assets and foreign property protected wealth. During the 1970s US stagflation, gold and real estate owners prospered while stock and bond investors struggled. The consistent pattern: diversified holders of real assets fared better than those concentrated in currency-denominated paper assets. But even in severe crises, some currency remained functional for transactions—complete societal breakdown is rare.

Preparing for potential dollar weakness doesn't require extreme measures or abandoning conventional investments. The goal is balance—enough protection to preserve purchasing power if currency problems emerge, but not so much that you sacrifice growth during normal times.

Physical assets like precious metals and real estate provide tangible value independent of government promises. Financial instruments like foreign currency exposure and inflation-protected securities offer liquidity and ease of management. Cryptocurrency might play a speculative role for those comfortable with volatility and risk.

Historical episodes show that diversified portfolios with real asset exposure navigate currency devaluation far better than cash-heavy approaches. But they also reveal that timing currency moves is nearly impossible and that extreme positions often backfire.

Start with modest allocations to dollar-hedging assets—perhaps 5% gold, 5% foreign bonds, and 10% in real assets beyond your home. Monitor economic indicators like inflation trends, federal debt levels, and foreign reserve currency holdings. Adjust gradually rather than making dramatic shifts based on headlines.

The dollar has survived numerous predictions of its demise. It might continue dominating for decades, or it might decline substantially within years. Your financial security shouldn't depend on predicting which scenario unfolds. Instead, build a portfolio resilient enough to preserve wealth across multiple outcomes. That's not pessimism—it's prudent risk management based on historical precedent and the recognition that no currency, no matter how dominant today, maintains its position forever.

Volatility determines profit potential and risk in forex trading. Some currency pairs swing hundreds of pips daily while others barely move. This guide examines which pairs exhibit the highest price fluctuations, why certain currencies are more volatile, and how to trade them effectively with proper risk management

The forex market processes $7.5+ trillion daily, yet a handful of pairs dominate volume. Learn which currency pairs traders prefer, why EUR/USD captures 24% of global transactions, and how liquidity, spreads, and volatility shape pair selection for different trading strategies

Major currencies represent the backbone of global foreign exchange markets. These monetary units from economically stable nations account for over 90% of daily forex turnover. Understanding which currencies dominate trading, how they're classified, and why they matter helps traders and investors navigate international markets

Discover the full scope of world currencies in 2026—from the 180+ recognized legal tenders to the major players in forex markets. Learn currency names by country, understand fiat vs. digital money, and get actionable advice for travel and international business

The content on this website is provided for general informational and educational purposes only. It is intended to explain concepts related to Forex (FX) trading, currency markets, leverage, hedging, and risk management.

All information on this website, including articles, guides, and examples, is presented for general educational purposes. Forex trading carries significant risk, and outcomes may vary depending on market conditions, leverage, and individual decisions.

This website does not provide financial, investment, or trading advice, and the information presented should not be used as a substitute for consultation with qualified financial professionals.

The website and its authors are not responsible for any errors or omissions, or for any outcomes resulting from decisions made based on the information provided on this website.