Most traders have heard whispers about forex arbitrage—the supposed holy grail of risk-free profits. Buy a currency pair cheap here, sell it expensive there, pocket the difference. Simple, right?

Not quite. Those price gaps between brokers? They vanish faster than you can blink. We're talking milliseconds here, not minutes.

The forex market moves $7.5 trillion every single day as of 2026. That's more money than the GDP of most countries. Inside this enormous marketplace, tiny pricing mismatches pop up constantly. But here's the catch: institutional traders with supercomputers sitting next to exchange servers grab these opportunities before your trading platform even refreshes.

Let's dig into how currency arbitrage actually functions, who's making money from it, and whether you stand a snowball's chance in hell of profiting from these strategies.

Understanding Forex Arbitrage Basics

What is forex arbitrage? The basic concept goes like this: you spot a currency trading at different prices in different places, then execute offsetting positions to capture the spread. No directional risk, just pure mathematics.

Sounds bulletproof. EUR/USD quotes at 1.0850 with Broker A but 1.0855 with Broker B? Buy low, sell high, collect five pips. Except reality throws wrenches into this beautiful theory faster than you can open your trading platform.

These price gaps exist because information doesn't teleport instantly. When London updates a quote, that price change takes microseconds to reach servers in Tokyo or New York. During that blink-and-you'll-miss-it window, exchange rates diverge. Banks refresh their pricing at slightly different moments. Liquidity providers update their quote engines on varying schedules.

Market efficiency tells us these opportunities shouldn't last. The forex market proves this brutally. Trading firms with quantum computers report arbitrage windows in major pairs now average just 0.3 seconds in 2026. Ten years ago? Those same opportunities lasted over two seconds—an eternity in algorithmic trading terms.

Here's the beautiful paradox: arbitrage and market efficiency feed each other. When traders exploit a price gap, they automatically close it. Buying the cheap version pushes that price up. Selling the expensive version drags that price down. The gap shrinks until nothing remains worth trading.

JPMorgan employs entire teams of math PhDs who design systems to catch these microsecond windows. Their servers sit physically inside exchange data centers—a setup called co-location that shaves nanoseconds off execution time. That's the competition you're up against.

How Currency Arbitrage Works in Practice

How currency arbitrage works comes down to three things: spotting the gap, calculating if it's worth trading, and executing before it disappears. All within timeframes your brain can barely process.

Let's walk through the mechanics. You're monitoring EUR/USD across multiple banks. Provider A shows 1.0850. Provider B displays 1.0852. Provider C quotes 1.0848. You buy 100,000 units from Provider C at 1.0848, simultaneously selling to Provider A at 1.0850.

Your calculator says: 0.0002 × 100,000 = $20 gross. But wait. Factor in the bid-ask spread (usually 0.1 to 0.5 pips on majors), execution slippage where your order fills at a worse price than expected, and commission fees. Total costs hit 1.5 pips? You just lost money.

Speed determines everything. A human trader spots the discrepancy, clicks buy, confirms the order—meanwhile prices already converged. Automated systems complete this entire sequence in under 10 milliseconds. You can't compete with your mouse and keyboard.

Arbitrage opportunities in forex cluster around specific events. Major economic announcements when quote engines lag momentarily. Exotic currency pairs with thinner liquidity where prices move slower. The rollover period when spot and futures markets briefly diverge. Each scenario brings unique headaches.

The technical setup alone scares most people away. You need direct market access that bypasses retail brokers. Dedicated servers with fiber-optic connections. Redundant internet lines in case one fails. Software capable of parsing fifteen different price feeds simultaneously and executing trades across all of them.

Author: Ethan Blackwell;

Source: martinskikulis.com

Real-World Example of a Currency Arbitrage Trade

A Chicago-based quant shop monitors AUD/USD across five major banks every microsecond. March 15th, 9:15 AM Eastern, the Reserve Bank of Australia drops unexpected guidance on rates. Quote engines across different banks update at different speeds. The gap lasts 0.4 seconds.

Bank A quotes: AUD/USD 0.6523 Bank B shows: AUD/USD 0.6521 Bank C displays: AUD/USD 0.6525

The firm's algorithm catches this within 3 milliseconds. Two trades fire simultaneously: - Purchase 5 million AUD/USD from Bank B at 0.6521 - Sell 5 million AUD/USD to Bank C at 0.6525

Before costs: 0.0004 × 5,000,000 = $2,000 After spread, commission, and slippage: roughly $800 net

This required $3.26 million in trading capital (5 million × 0.6521). The return? About 0.025% in under one second. Scale that across a year and you'd be printing money. Except opportunities like this might happen 15-30 times daily across all pairs, not thousands of times.

Four other firms detected this exact opportunity. Three executed successfully. Two arrived 0.6 seconds late—an eternity in algorithm time—and ate losses from the spread when prices had already aligned.

Types of Forex Arbitrage Strategies

Different arbitrage tactics exploit various market quirks. Each demands specific technology, capital, and nerves of steel.

Triangular Arbitrage Explained

Triangular arbitrage hunts for misalignments between three interconnected currency pairs. You move money through three conversions, and if the math doesn't work perfectly, profits appear.

Here's the game: Take dollars, swap for euros, flip those euros into pounds, convert pounds back to dollars. When cross-rates drift out of sync with direct rates, you've found your edge.

Walk through the numbers: - Beginning balance: $100,000 - Dollars to euros at 1.0850: gives you €92,166 - Euros to pounds at 0.8500: nets £78,341 - Pounds back to dollars at 1.2800: returns $100,276

That's $276 before anyone takes their cut.

The detection formula: multiply (EUR/USD) × (GBP/EUR) × (USD/GBP). Perfect markets equal exactly 1.0000. Any deviation signals opportunity.

That discrepancy screams "trade me!" except transaction costs usually devour any theoretical edge. Professional systems track dozens of three-way combinations continuously, only firing when the spread exceeds costs by comfortable margins.

These opportunities shrank dramatically after 2023 when major banks upgraded pricing engines to cross-check all pairs in real-time. Current windows last 0.1 to 0.2 seconds for liquid currencies.

Statistical Arbitrage in Forex

Statistical arbitrage forex strategies play a completely different game than pure arbitrage. Instead of guaranteed price differences, you're betting on historical patterns repeating. Currency pairs that normally move together temporarily diverge, and you trade expecting them to reconnect.

Take AUD/USD and NZD/USD. These pairs typically track each other because Australia and New Zealand share geographic proximity and similar economic drivers. When the spread between them widens beyond normal levels, you short whichever performed better and buy the laggard. Then you wait for mean reversion.

This approach leans heavily on: - Correlation analysis over 90-180 day windows - Z-score calculations flagging extreme deviations - Position sizing based on volatility measurements - Holding trades anywhere from hours to weeks

Unlike pure arbitrage, statistical methods carry actual risk. Correlations break permanently. Maybe Australia hits a mining boom while New Zealand's agricultural sector struggles. Suddenly your "temporary" divergence becomes the new normal.

Hedge funds deploy machine learning models analyzing hundreds of currency relationships simultaneously. These systems spot patterns invisible to humans, though they still blow up spectacularly when market conditions shift.

Latency Arbitrage and High-Frequency Trading

Latency arbitrage forex feeds on the time delay between price updates across different platforms. One broker's price changes, and traders with faster connections execute on slower brokers before those quotes refresh.

Requirements include: - Servers physically located inside exchange data centers - Direct market access cutting execution to sub-millisecond speeds - Sophisticated algorithms monitoring multiple price feeds - Infrastructure investment starting around $500,000 annually

A serious latency arbitrage operation burns through $500,000 to $2 million yearly on infrastructure, data feeds, and co-location fees. Firms compete to shave nanoseconds—not milliseconds, nanoseconds—off execution times.

The ethics here get murky. Some brokers explicitly ban this practice in their fine print. The strategy exploits technology advantages rather than genuine market inefficiencies, leading critics to call it parasitic.

Retail traders occasionally try latency arbitrage by opening accounts at multiple brokers and comparing price feeds. This almost never works because: - Your execution speed can't touch institutional infrastructure - Brokers spot arbitrage patterns and restrict accounts - Transaction costs exceed the microscopic price gaps available - Slippage during order execution kills theoretical profits

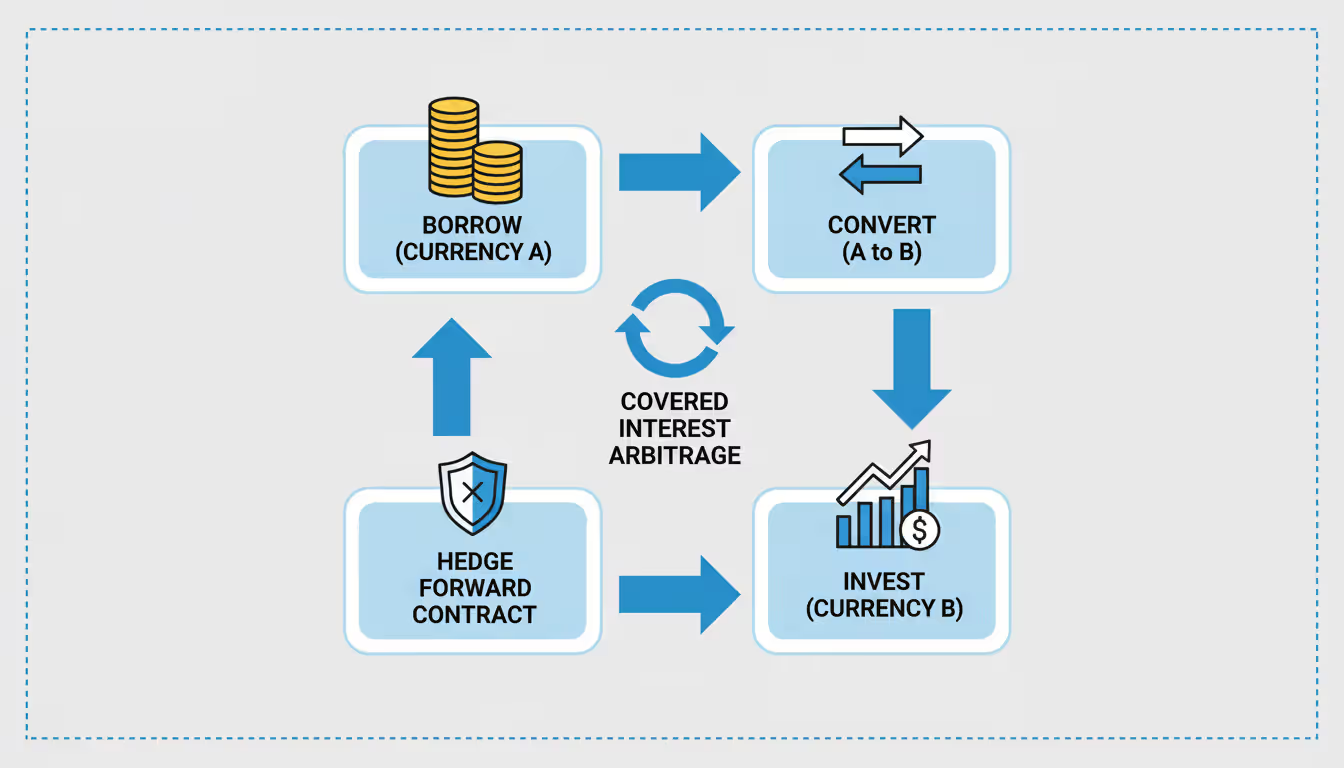

Covered Interest Arbitrage

Covered interest arbitrage exploits gaps between spot rates, forward rates, and interest rate differences between countries. You borrow in a low-rate currency, convert to a high-rate currency, invest at the better rate, then lock in a forward contract eliminating exchange rate risk.

When this relationship breaks, arbitrage windows open.

Scenario using 2026 rates: - Borrow $1,000,000 at 4.5% annually (USD rate) - Convert to euros at spot rate 1.0850: €921,659 - Invest euros at 3.2% annually - Sell euros forward at 1.0900 for one-year settlement

One year later: - Euro investment becomes: €921,659 × 1.032 = €951,152 - Forward conversion at 1.0900: $1,036,756 - USD loan repayment: $1,000,000 × 1.045 = $1,045,000 - Final result: Loss of $8,244

This shows no arbitrage exists when parity holds. But during market stress or regulatory shifts affecting capital flows, deviations emerge.

The 2022-2023 banking sector chaos created significant parity violations for emerging market currencies. Turkish lira and Argentine peso forward markets showed persistent gaps as capital controls and credit risk warped normal relationships.

Banks and multinationals use covered interest arbitrage optimizing global cash management. A corporation receiving euros but paying dollars can structure forward contracts capturing favorable rate differentials while hedging currency exposure.

Author: Ethan Blackwell;

Source: martinskikulis.com

How Banks and Institutions Use Forex Arbitrage

How banks use forex arbitrage differs from anything retail traders can imagine. Major institutions possess structural advantages making arbitrage a genuine (if modest) profit center.

Banks function as market makers, quoting both bid and ask prices to clients continuously. This provides information advantages—they watch order flow across thousands of daily transactions. A large corporate order temporarily moves prices, and the bank's trading desk hedges that position across multiple venues, capturing small spreads.

Major bank technology includes: - Trading platforms connecting directly to every significant liquidity provider - Quant research teams developing predictive algorithms - Risk systems monitoring exposure across all currency pairs simultaneously - Co-located servers at primary forex trading venues

JPMorgan, Citibank, and Deutsche Bank together handle roughly 35% of global forex volume. This scale lets them profit from bid-ask spreads while simultaneously running arbitrage algorithms exploiting temporary inefficiencies.

A typical bank arbitrage desk might generate 0.5 to 2 basis points per trade. With billions in daily volume, these razor-thin margins produce meaningful profits. A bank executing $50 billion daily at an average 1 basis point profit earns $5 million daily.

Banks even arbitrage between their own regional offices. A price mismatch between London and Tokyo desks creates internal arbitrage opportunities. Sophisticated banks use these instances testing and refining pricing algorithms rather than simply profiting from internal inefficiencies.

Regulatory capital requirements limit how aggressively banks chase arbitrage. Basel III regulations require holding capital against trading positions, making low-margin strategies less attractive. Many banks scaled back proprietary trading after 2024 regulatory updates increased capital charges on high-frequency activities.

The push-pull between arbitrage and market efficiency ultimately benefits everyone. When banks aggressively eliminate price discrepancies, they improve price consistency across global forex markets. This efficiency reduces transaction costs for corporations, investors, and eventually consumers.

Forex Arbitrage Risks and Limitations

Forex arbitrage risks extend way beyond simple execution challenges. Even sophisticated institutions face substantial obstacles limiting profitability.

Execution risk dominates the worry list. Prices shift between spotting an opportunity and when your orders actually fill. In volatile markets, the currency you're buying might jump higher while the one you're selling drops further, flipping theoretical profit into real loss. Partial fills create nightmares—your buy order completes but your sell order only fills 60%, leaving unwanted directional exposure.

Transaction costs murder most apparent opportunities. Run the numbers on typical retail trading: - EUR/USD spread: 0.8 pips - Commission: $7 per 100,000 units - Average slippage: 0.3 pips - Combined cost: approximately 1.1 pips

Any arbitrage opportunity must exceed 1.1 pips just reaching break-even. In 2026, such discrepancies rarely survive long enough for manual execution.

Broker restrictions specifically hunt arbitrage traders. Most retail brokers ban: - Latency arbitrage between their platform and external price sources - Exploiting system delays or errors - High-frequency strategies straining their infrastructure

Brokers identify arbitrage patterns through: - Monitoring hold times (arbitrage trades close within seconds) - Analyzing win rates (arbitrage shows unusually high success rates) - Tracking execution patterns (simultaneous opposite trades across correlated pairs)

Accounts flagged for arbitrage face requotes, widened spreads, withdrawal delays, or outright closure. One trader reported seven different broker accounts restricted within three months after attempting latency arbitrage in 2025.

Market efficiency barriers keep strengthening. Proliferation of algorithmic trading means more competitors chasing fewer opportunities. Each new algorithm reduces average arbitrage windows. What lasted seconds in 2020 now disappears in milliseconds.

Regulatory considerations vary by location. The U.S. Commodity Futures Trading Commission doesn't explicitly prohibit forex arbitrage, but related practices like spoofing (placing orders you intend to cancel manipulating prices) carry severe penalties. The 2025 case against a Chicago firm resulted in $4.2 million in fines for manipulative trading disguised as arbitrage.

Capital requirements create another massive barrier. Meaningful arbitrage profits demand substantial position sizes. A 0.5-pip gain on a 100,000-unit position yields $50. Generating $500 daily requires either ten such trades or million-unit positions. Most retail traders lack sufficient capital making the strategy worthwhile after costs.

Leverage presents a paradox. Higher leverage allows larger positions with less capital, but amplifies losses when execution fails. A 1-pip adverse move on a 1-million-unit position with 50:1 leverage can obliterate a $20,000 account.

Technology costs for legitimate arbitrage operations: - Virtual private servers: $100-500 monthly - Premium data feeds: $200-1,000 monthly - Trading software: $500-5,000 monthly - Development and maintenance: $2,000-10,000 monthly

You might drop $50,000 annually on infrastructure competing for opportunities that institutional players with million-dollar systems are simultaneously targeting.

Can Retail Traders Profit From Arbitrage Opportunities?

Author: Ethan Blackwell;

Source: martinskikulis.com

Let's be blunt: rarely, and definitely not through traditional arbitrage.

Retail traders face crushing disadvantages in speed, technology, and capital. By the time your platform displays a price discrepancy, institutional algorithms already exploited and eliminated it. The technological chasm between retail and institutional infrastructure widened further in 2026 as major banks deployed quantum computing for pattern recognition in forex.

Technology gaps manifest everywhere: - Your retail platform updates prices every 100-500 milliseconds while institutional systems operate in microseconds - Order routing through retail brokers adds 50-200 milliseconds compared to institutional direct market access that's nearly instantaneous - You access aggregated liquidity pools while institutions connect directly to primary providers

A 2025 MIT study tracked 10,000 attempted arbitrage trades by retail accounts. Success rate? 3.2%. Average loss per attempt after spreads and commissions: $47. The few profitable trades averaged $12 gains.

Viable alternatives exist for traders interested in the arbitrage concept: - Focus on statistical arbitrage with longer holding periods (hours to days) where speed advantages matter less - Trade emerging market currency pairs where inefficiencies persist longer - Exploit differences between spot forex and currency futures during rollover periods - Use correlation strategies between currencies and related assets like currency ETFs or commodity prices

One semi-viable approach involves arbitrage between retail forex brokers and cryptocurrency exchanges for pairs like EUR/USD versus EUR/USDT (Tether). Price discrepancies occasionally last several seconds during high volatility, though liquidity constraints and transfer delays limit profitability.

When opportunities might exist: - During extreme volatility events (central bank surprises, geopolitical shocks) when even sophisticated systems struggle keeping pace - In exotic currency pairs with limited liquidity where institutional players have less presence - Between different financial instruments (spot forex vs. currency options vs. futures) rather than between forex brokers - In jurisdictions with capital controls creating persistent pricing inefficiencies

A realistic example: A trader in 2026 identified recurring discrepancies between USD/TRY (Turkish lira) prices on retail forex platforms and Turkish domestic bank rates during Istanbul market open. The 2-3 second window allowed manual execution twice weekly, generating approximately $200 monthly before the pattern disappeared as others discovered it.

Bottom line: view arbitrage as education rather than practical strategy. Understanding how arbitrage functions improves overall market comprehension and risk management, even if direct application remains impractical for individuals.

The forex arbitrage landscape transformed fundamentally over the past decade. What once seemed accessible to well-capitalized retail traders now exists almost exclusively in institutional high-frequency trading territory. The combination of algorithmic sophistication and infrastructure investment required for consistent arbitrage profits has created an effective $10 million barrier to entry. The opportunities remaining for smaller players live either in statistical arbitrage with longer time horizons or exploiting temporary inefficiencies in less liquid emerging market currencies. Anyone selling retail traders profitable arbitrage systems is either misinformed or deliberately misleading. Market efficiency mathematics, combined with relentless trading technology improvements, has rendered traditional arbitrage largely theoretical for individual traders

— Dr. Michael Zhao

Dr. Zhao's research group analyzed over 2 billion forex transactions in 2025. They found 94% of arbitrage profits were captured by just 12 institutional players. The top three firms accounted for 67% of total arbitrage gains.

Frequently Asked Questions

Is forex arbitrage legal?

Yes, forex arbitrage operates legally in the United States and most jurisdictions. However, certain related practices might violate regulations or broker terms. Latency arbitrage exploiting system delays could breach broker agreements, while manipulative practices like spoofing are explicitly illegal under CFTC regulations. Always review broker terms carefully—many prohibit strategies exploiting price feed delays or system errors. International traders should consult local regulations, since some countries with capital controls restrict certain arbitrage activities.

How much capital do you need for forex arbitrage?

Meaningful arbitrage demands substantial capital because profit margins are paper-thin. Institutional players typically deploy $1-10 million per strategy. Retail traders attempting statistical arbitrage might start with $50,000, though profitability remains questionable below $100,000. Pure arbitrage opportunities yield 0.5-2 pips, meaning a 100,000-unit position generates $50-200 gross. Transaction costs eat most of that. You need position sizes of 500,000-1,000,000 units generating worthwhile returns. Using 50:1 leverage, this requires $10,000-20,000 in margin, but prudent risk management suggests maintaining at least five times that as buffer, pushing minimum capital toward $50,000-100,000.

Why do arbitrage opportunities disappear so quickly?

Several forces cause rapid convergence. First, algorithmic trading systems from hundreds of institutions simultaneously monitor prices and execute within milliseconds when discrepancies surface. Second, arbitrage itself—buying underpriced assets and selling overpriced ones—automatically pushes prices toward equilibrium. Third, modern market infrastructure dramatically reduced latency, allowing price updates propagating across venues in microseconds. Fourth, increased competition means more capital chasing fewer opportunities. The average arbitrage window in major currency pairs lasts 0.2-0.4 seconds in 2026, down from several seconds a decade ago.

What is the difference between triangular and statistical arbitrage?

Triangular arbitrage hunts for pricing inconsistencies between three related currency pairs, offering theoretically risk-free profits if executed simultaneously. You identify when cross-rates don't align with direct rates, then execute three trades within milliseconds. Statistical arbitrage takes positions based on historical price relationships expecting mean reversion. It carries directional risk since correlations can permanently break. Triangular arbitrage profits from guaranteed mathematical relationships while statistical arbitrage profits from probable (though not certain) pattern repetition. Holding times differ dramatically—triangular positions last under one second while statistical positions might remain open days or weeks.

Do forex brokers allow arbitrage trading?

Most retail forex brokers prohibit or restrict arbitrage trading in their terms. Specific restrictions typically target latency arbitrage (exploiting price feed delays), hedging between their platform and competitors, or strategies exploiting system errors. Brokers detect arbitrage by monitoring hold times, win rates, and execution patterns. Accounts identified using arbitrage may face requotes, increased spreads, withdrawal restrictions, or closure. Some brokers market themselves as "arbitrage-friendly" but still maintain restrictions on certain practices. Institutional brokers and prime brokers generally accommodate arbitrage since they earn from volume rather than client losses. Always read terms carefully and contact your broker directly if planning arbitrage strategies.

Can automated trading bots execute arbitrage strategies?

Automated systems prove essential for successful arbitrage—humans simply can't execute fast enough. Most retail trading bots claiming to perform arbitrage fail due to infrastructure limitations. Effective arbitrage bots demand direct market access, co-located servers, premium data feeds, and sophisticated algorithms. Retail bots running on standard VPS servers through broker APIs face latency eliminating profitability. That $99 "arbitrage expert advisor" sold online typically loses money after transaction costs. Institutional arbitrage systems represent millions in development and infrastructure investment. Retail traders can use automated systems for statistical arbitrage with longer timeframes, where speed advantages matter less, but pure arbitrage automation remains impractical without institutional-grade infrastructure.

Forex arbitrage sits at a fascinating intersection of mathematics, technology, and market dynamics. The theoretical concept promises risk-free profits from price discrepancies, yet practical implementation reveals a landscape dominated by institutional players with technological advantages beyond retail reach.

Forex market evolution toward greater efficiency systematically eliminated opportunities accessible to individual traders. Algorithmic trading, improved infrastructure, and intensified competition compressed arbitrage windows from seconds to milliseconds. The capital, technology, and expertise required for consistent profitability now exceed what most retail traders can realistically deploy.

This doesn't make arbitrage concepts useless for individual traders. Understanding how arbitrage functions improves market comprehension, reveals why prices move as they do, and explains institutional player roles. Statistical arbitrage approaches with longer timeframes offer more realistic opportunities for well-capitalized retail traders willing to accept directional risk.

The critical takeaway: approach forex arbitrage with realistic expectations. Those "risk-free profits" promised by various trading courses and software vendors rarely materialize in actual accounts. Successful trading requires identifying strategies aligned with your capital level, technological capabilities, and risk tolerance. For most retail traders, traditional directional trading, swing strategies, or longer-term position approaches offer more viable paths toward profitability than chasing arbitrage opportunities already exploited by algorithms operating at microsecond speeds.

The spread is the difference between bid and ask prices in forex trading—your cost to enter every position. Understanding how spreads work, when they widen, and how to minimize these costs can dramatically improve your trading profitability over time

A pip represents the smallest standardized price movement in forex trading. Understanding pip calculations is essential for position sizing, risk management, and profit calculation. This guide explains pip definitions, calculation methods for different currency pairs, and how to avoid common mistakes

Spread betting allows you to speculate on price movements without owning assets. This leveraged derivative offers access to thousands of markets but carries substantial risks. Learn how spread betting works, profit/loss mechanics, tax implications, and critical mistakes to avoid

The forex market moves $7.5 trillion daily, yet most retail traders lose money. Regulatory data shows only 15-25% maintain profitable accounts. This guide examines real statistics, common failure causes, and what actually makes traders profitable based on 2026 data

The content on this website is provided for general informational and educational purposes only. It is intended to explain concepts related to Forex (FX) trading, currency markets, leverage, hedging, and risk management.

All information on this website, including articles, guides, and examples, is presented for general educational purposes. Forex trading carries significant risk, and outcomes may vary depending on market conditions, leverage, and individual decisions.

This website does not provide financial, investment, or trading advice, and the information presented should not be used as a substitute for consultation with qualified financial professionals.

The website and its authors are not responsible for any errors or omissions, or for any outcomes resulting from decisions made based on the information provided on this website.