Back in 1972, the Chicago Mercantile Exchange launched something that would reshape how businesses and traders handle foreign currency risk. Currency futures arrived on the scene, and they've been gaining ground ever since—particularly among companies that need predictable exchange rates and traders who want the structure of exchange-traded products.

If you're sizing up hedging options for cross-border business dealings or considering leveraged bets on currency moves, you'll want to understand how these contracts actually work—and where they diverge from the spot forex market most retail traders know.

What Are Currency Futures and How Do They Work

Think of currency futures as binding agreements where you commit to exchanging a fixed amount of one currency for another on a specific future date, at a price you lock in today. Everything about these contracts—their size, when they expire, how prices move—stays identical across all market participants because the exchange mandates it.

CME Group runs the show for US currency futures. They list contracts on major pairs (EUR/USD, GBP/USD, JPY/USD) plus emerging-market currencies like the Mexican peso and Brazilian real. Contract sizes stay fixed: one euro contract controls €125,000, while a British pound contract covers £62,500. You can't customize these amounts. The uniformity creates deep liquidity pools since everyone trades the same thing.

Price movements happen in standardized increments called ticks. On the euro futures, one tick represents $0.00005 per euro—that's $6.25 of actual money per contract. Buy ten contracts, watch the price climb 20 ticks, and you just made $1,250. These uniform increments make P&L calculations straightforward and let algorithmic systems execute strategies that depend on precise price steps.

Here's where futures diverge sharply from holding spot currency: mark-to-market settlement happens every single trading day. The clearinghouse calculates each position's value at 4:00 PM Central and immediately moves cash between accounts. Your position climbs? Money hits your account that night. It drops? Cash leaves your account. This daily reckoning prevents credit risk from accumulating the way it might in a bilateral agreement where settlement waits until the end.

Contracts expire quarterly—March, June, September, December—though you'll also find nearby months like April or May for short-term hedging. The March euro contract trades alongside these serial months. Most traders close out before expiration, but if you hold through the final trading day, you'll either deliver currency or receive a cash settlement, depending on which contract you're trading.

Currency futures provide price transparency and centralized clearing that many institutional hedgers require.The standardization and exchange infrastructure reduce counterparty risk, which remains a priority for corporate treasurers and fund managers

— Agha Mirza

How Currency Futures Pricing Works

Currency futures don't exist in a vacuum—their prices anchor to the spot exchange rate, then adjust for the interest rate gap between the two currencies. This relationship, known as the cost-of-carry model, captures the opportunity cost of holding one currency instead of another until the contract expires.

When US rates run higher than eurozone rates, euro futures trade below the spot rate—a situation called contango. Flip it around, and futures trade above spot (backwardation). In early 2026, the Fed holds rates near 4.75% while the ECB sits at 3.25%. Euro futures typically trade at a discount to spot because holding dollars earns you more interest than holding euros.

The gap between futures and spot is called forward points. Traders watch this spread obsessively. When it strays too far from what the interest rate math says it should be, arbitrageurs pounce—buying the undervalued instrument, selling the overvalued one, pocketing the difference. That activity snaps prices back toward fair value.

Several forces push futures prices around:

Central bank policy shifts: Markets price in rate changes months before they happen, moving forward points ahead of official announcements

Credit stress: During financial turbulence, spreads between futures and spot widen as traders demand compensation for uncertainty

Hedging waves: Heavy corporate hedging flows or speculative positioning can temporarily overwhelm the interest rate math

Volatility enters the equation too. When implied volatility spikes, options embedded in some hedging strategies get pricier, which can shift futures demand. The VIX and currency-specific volatility indices help traders gauge whether current pricing reflects realistic expectations or panic.

Currency Futures vs Spot Forex Trading

The futures-versus-forex decision comes down to trading style, how much you care about regulation, and what operational features matter most to you. Each market has structural quirks that favor different users.

Feature

Currency Futures

Spot Forex

Contract standardization

Fixed sizes, set expirations, uniform ticks

Flexible lot sizing, positions never expire

Trading venue

Centralized exchange (CME)

Decentralized over-the-counter network

Margin requirements

Exchange-mandated; usually 3–5% of notional

Broker-determined; often 1–2% or less

Regulation

CFTC oversight with strict position caps

Lighter regulation; varies by broker location

Settlement method

Daily mark-to-market; delivery or cash

Rolling positions with no delivery events

Trading hours

Nearly 24 hours with short maintenance gaps

True round-the-clock Monday through Friday

Typical spreads

Wider (0.5–1.5 pips on majors)

Tighter (0.1–0.5 pips on majors)

Counterparty risk

Clearinghouse backs every trade

Depends entirely on broker creditworthiness

Institutions gravitate toward futures because they need regulatory transparency and bulletproof clearing. A multinational hedging €50 million in receivables can execute a block trade on CME knowing the clearinghouse guarantees settlement. With spot forex, you're trusting your broker's balance sheet—a risk some treasury departments won't touch.

Retail traders often pick spot forex for lower barriers to entry and razor-thin spreads. Got $5,000? You can control serious notional value through high leverage. Spot brokers offer micro-lots (1,000 units), letting you dial in position sizes that futures' standardized contracts can't match.

Taxes diverge too. IRS Section 1256 gives futures traders a 60/40 capital gains split—60% taxed at long-term rates (max 20%), 40% at short-term rates (up to 37%)—no matter how long you hold. Spot forex gains usually get ordinary income treatment unless you make specific elections with your accountant, which complicates year-end planning.

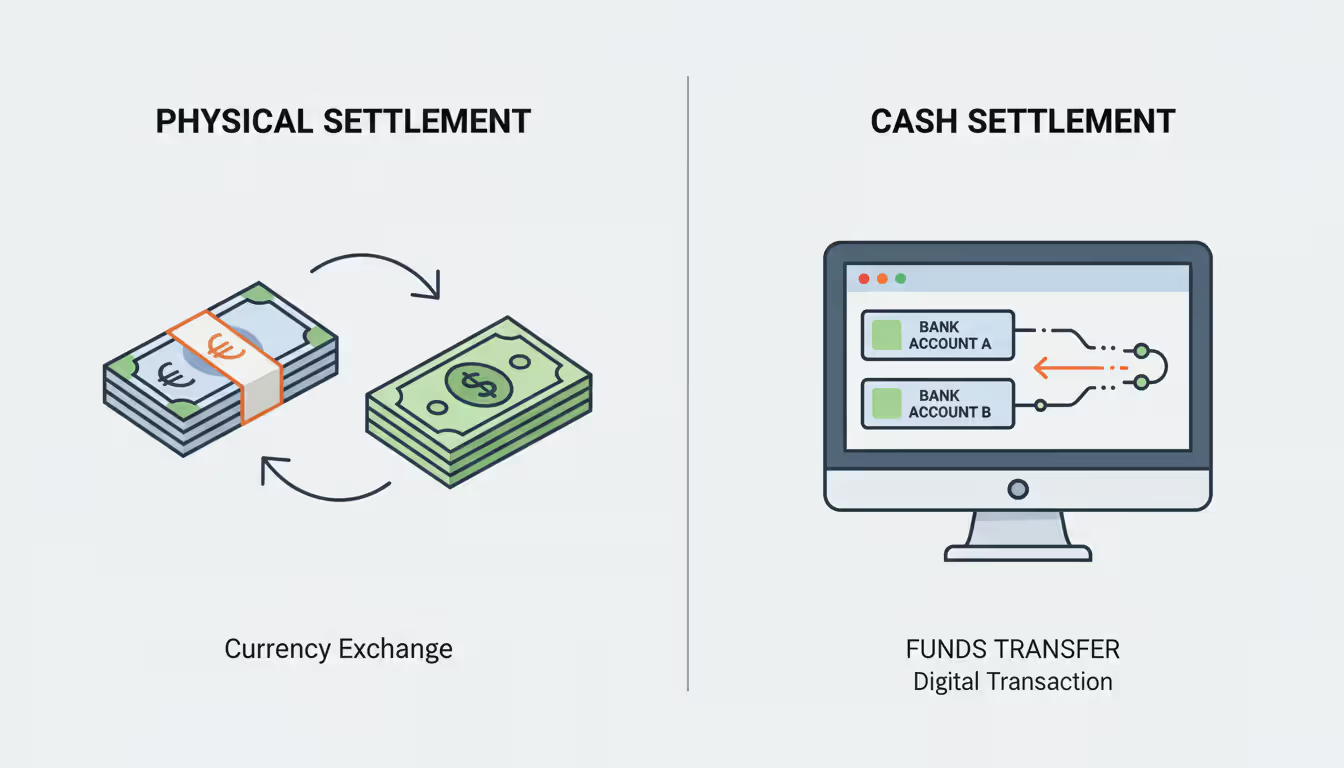

Key Differences in Settlement and Expiration

Currency futures offer two settlement paths: physical delivery or cash. Physical delivery means you actually receive the currency. Hold a euro contract through expiration? You get €125,000 and pay the USD equivalent at the final settlement price. Delivery happens two business days after the last trading day, matching standard FX market conventions.

Cash settlement skips the currency transfer entirely. The clearinghouse calculates the difference between the final price and your entry price, then moves cash accordingly. Japanese yen futures use cash settlement exclusively—simpler for speculators who never wanted actual yen anyway.

Author: Vanessa Cole;

Source: martinskikulis.com

Quarterly expirations create predictable roll dates. The March contract stops trading on the second Friday of March. You either close the position or roll it into June. Contrast this with spot forex, where positions sit open indefinitely through automatic rollovers that charge you swap fees each night.

Forget to roll and you'll get an unpleasant surprise. A speculator long ten euro contracts who blanks on the March expiration might find their broker force-closing the position at a terrible price—or, worse, initiating delivery procedures that rack up unexpected fees. Smart traders set calendar alerts two weeks out.

Margin Requirements and Contract Settlement

Exchanges calibrate margin levels by looking at volatility and contract value, trying to balance risk control against capital efficiency. You need to post two types of margin: the initial deposit to open a position, and the maintenance threshold your account must stay above to keep it open.

Euro futures in early 2026 carry initial margin around $3,300 per contract—roughly 2.6% of the $125,000 notional. Maintenance margin sits near $3,000. Open five contracts and you deposit $16,500. Daily losses push your account below $15,000? Your broker calls demanding more cash to bring you back to initial margin.

Mark-to-market happens every trading day at 4:00 PM Central. The clearinghouse compares your position's settlement price to yesterday's, then moves money between accounts. This daily cash flow catches new traders off guard: a $2,000 paper loss Monday becomes a real $2,000 withdrawal from your account Monday night. You need liquid cash to cover it or face forced liquidation.

Author: Vanessa Cole;

Source: martinskikulis.com

Variation margin—the daily settlement amount—transfers immediately. You're long three euro contracts and settlement drops 50 ticks? Your account loses $937.50 overnight ($6.25 per tick × 50 ticks × 3 contracts). The clearinghouse doesn't wait for you to exit; cash moves that evening. Keep a buffer above maintenance margin so normal volatility doesn't trigger margin calls.

Portfolio margining can slash your capital requirements. The clearinghouse offsets correlated positions—say you're long euro futures and short British pound futures. EUR/USD and GBP/USD usually move together, reducing your net risk. CME's SPAN (Standard Portfolio Analysis of Risk) system calculates these offsets, sometimes cutting total margin by 20–40% versus treating each position separately.

Rolling Currency Futures Contracts

Futures expire, but your exposure might need to continue. Rolling means closing your near-expiration position while simultaneously opening an equivalent one in a later expiration month. You maintain your directional bet without dealing with delivery.

The rolling window typically opens two to three weeks before expiration, when trading volume shifts from the expiring contract to the next one. For March euro futures expiring mid-March, most traders roll during the first week of March as open interest migrates to June. Roll too early and you pay wider spreads in the less-liquid June contract. Wait too late and you're stuck in the expiring contract's final-day chaos.

Mechanically, it's simple: sell (or buy back) your March contract while buying (or selling) the June contract in one transaction—a calendar spread. Many brokers offer one-click roll tools that execute both sides simultaneously, minimizing the gap between your exit and re-entry. The price difference between contracts captures the interest rate differential over those three months.

These roll costs add up. If euro futures consistently trade at a 20-tick discount to the next contract because US rates exceed eurozone rates, each quarterly roll costs you $6.25 × 20 = $125 per contract. Four rolls a year total $500 per contract—a meaningful drag if you're holding long-term positions. Compare that to spot forex swap fees that hit nightly but might total less over twelve months.

Some traders use "spread roll" orders, specifying the price gap between contracts instead of executing two separate trades. You might submit an order to "roll March to June at a 15-tick discount," and it fills when the market reaches that spread. This reduces execution risk but might take longer in thin markets.

Broker auto-roll features simplify the process but require oversight. A trader holding ten contracts who enables auto-roll might not notice their broker executing at a lousy spread during overnight hours when liquidity dries up. Always review roll confirmations and compare execution prices to the prevailing market spread.

Using Currency Futures for Hedging

Companies, fund managers, and exporters use currency futures to nail down exchange rates months ahead, eliminating the guesswork from international transactions. Take a Texas electronics importer expecting to pay €1 million to a German supplier four months out. If EUR/USD climbs from 1.1000 to 1.1500, the dollar cost jumps from $1.1 million to $1.15 million—a $50,000 hit.

The hedge? Buy eight euro futures contracts (€125,000 × 8 = €1 million). If the euro strengthens, gains on those futures offset the higher cost of buying euros for the supplier payment. Say EUR/USD rises to 1.1500 and the futures contract appreciates 500 ticks. The importer makes $6.25 × 500 × 8 = $25,000 on the futures. Yes, the supplier payment costs $50,000 more, but the futures profit cuts the net increase to $25,000.

Perfect hedges rarely exist. The futures contract expires mid-June, but the supplier payment lands late June. Basis risk—the mismatch between your hedge and your actual exposure—means the spot rate on payment day might differ from the June futures settlement price. The importer could roll to September or just accept the residual risk, weighing hedge precision against transaction costs.

Author: Vanessa Cole;

Source: martinskikulis.com

Portfolio managers holding European stocks face currency exposure when those assets appreciate in euros but the fund reports in dollars. European equities rise 8% in euro terms, but the euro drops 5% against the dollar? Your dollar return collapses to roughly 3%. Selling euro futures proportional to your equity exposure neutralizes currency swings, isolating the equity performance.

Calculate your hedge ratio by dividing total exposure by contract size. A $5 million European equity portfolio requires $5,000,000 ÷ $125,000 = 40 euro futures contracts (assuming EUR/USD near 1.0000; adjust for the actual spot rate). Rebalance as portfolio value changes to maintain effective coverage.

Exporters face the mirror problem. A California winemaker selling $2 million of wine to UK distributors over six months faces pound depreciation risk. Selling British pound futures locks in the GBP/USD rate. The pound tanks? Futures gains offset lower dollar revenues from wine sales. The winemaker sells $2,000,000 ÷ $78,125 (£62,500 contract at a 1.2500 rate) ≈ 26 pound futures contracts.

Dynamic hedging adjusts positions as exposure evolves. A company with rolling monthly receivables might hedge 100% of next month's exposure, 75% of the second month, and 50% of the third, layering contracts to match cash-flow timing. This balances protection with flexibility, avoiding over-hedging if business conditions shift.

Frequently Asked Questions About Currency Futures

What is the minimum investment needed to trade currency futures?

You'll need $2,000–$5,000 per contract for major pairs like EUR/USD or GBP/USD, though that's just the exchange minimum. Brokers often add their own buffer. Smart traders keep at least 50% above the initial requirement to absorb daily swings without triggering margin calls. Realistically, start with $10,000–$15,000 if you want to trade one or two contracts without sweating every tick.

Can individual retail traders access CME currency futures?

Absolutely. You access CME futures through a futures broker (called a Futures Commission Merchant). Retail-friendly brokers like Interactive Brokers, TD Ameritrade's futures arm, and TradeStation all connect individual traders to the exchange. Account minimums range from $500 to $10,000 depending on the broker, though you need more capital to actually trade given margin requirements and practical risk management.

How are currency futures taxed in the US?

Futures get favorable treatment under IRS Section 1256. Gains split 60/40—60% taxed at long-term capital gains rates (maxing out at 20%), 40% at short-term rates (up to 37%)—no matter how long you held the position. That blended rate usually beats ordinary income treatment. You report everything on Form 6781 and Schedule D. Mark-to-market rules apply, so unrealized gains at year-end are taxable too.

What happens if I hold a currency futures contract until expiration?

Depends on the contract. Cash-settled ones like Japanese yen simply credit or debit your account based on the final settlement price, then close automatically. Deliverable contracts like the euro require you to either accept delivery (receiving €125,000 and paying the USD equivalent) or close before the last trading day. Most brokers force-liquidate retail positions a few days before expiration to avoid delivery headaches.

Are currency futures riskier than spot forex?

Risk comes from leverage and position sizing, not the instrument itself. Futures typically demand higher margin (3–5% of notional) than spot forex (1–2%), which naturally limits leverage. But futures' daily mark-to-market creates immediate cash demands that spot forex's floating P&L doesn't. Futures offer centralized clearing and stronger regulation, cutting counterparty risk versus OTC forex. Neither is inherently riskier—it's about how you use them.

Which currency pairs are most actively traded as futures?

The euro (EUR/USD) dominates, grabbing roughly 40% of CME currency futures volume. Japanese yen, British pound, Canadian dollar, and Australian dollar follow. Emerging-market contracts—Mexican peso, Brazilian real—are seeing growing interest from both hedgers and speculators. Euro contracts trade 300,000+ daily volume, ensuring tight spreads and reliable fills. That liquidity makes it the benchmark for currency futures.

Currency futures deliver exchange-traded FX exposure with standardized contracts, transparent pricing, regulatory safeguards, and clearinghouse backing. Whether you're hedging international cash flows or speculating on currency moves with leverage, these contracts provide a structured alternative to spot forex with distinct margin mechanics, settlement rules, and tax treatment.

Knowing contract specs, pricing dynamics, and rolling procedures separates traders who thrive from those blindsided by expiration dates or margin calls. The futures-versus-forex choice hinges on capital requirements, how much you value regulatory oversight, and whether standardized contracts or flexible position sizing better fits your approach.

Corporate treasurers locking in receivables, fund managers neutralizing currency risk, traders playing interest rate differentials—currency futures give all of them the infrastructure and liquidity to execute confidently. Match the instrument's structure to your specific needs, maintain disciplined risk controls, and stay aware of the interest rate dynamics driving futures prices.

Swap rates represent the interest cost or credit applied when forex traders hold positions past the daily rollover time. Understanding how these overnight fees work, when you pay or earn them, and their cumulative impact is essential for swing traders and anyone implementing carry trade strategies in 2026

Spread betting lets you speculate on market moves without owning the asset. This guide walks through real examples—long and short positions, forex pairs, margin calculations—showing exactly how profits and losses accumulate, how to size stakes responsibly, and what happens when trades go wrong

An overnight index swap is a derivative where parties exchange fixed and floating interest payments based on compounded overnight rates. These instruments have become the standard for derivatives discounting and provide key insights into central bank policy expectations and market stress levels

Interest rate movements can transform profitable loans into financial burdens overnight. Companies with floating-rate debt and bond investors face the same challenge: protecting against adverse rate shifts without sacrificing upside. This guide explains hedging instruments, duration strategies, and how to match protection to your specific exposure

The content on this website is provided for general informational and educational purposes only. It is intended to explain concepts related to Forex (FX) trading, currency markets, leverage, hedging, and risk management.

All information on this website, including articles, guides, and examples, is presented for general educational purposes. Forex trading carries significant risk, and outcomes may vary depending on market conditions, leverage, and individual decisions.

This website does not provide financial, investment, or trading advice, and the information presented should not be used as a substitute for consultation with qualified financial professionals.

The website and its authors are not responsible for any errors or omissions, or for any outcomes resulting from decisions made based on the information provided on this website.