Spot forex traders know the feeling—one surprise central-bank announcement, and suddenly your position is underwater with no buffer. Currency markets can swing 200 pips in an hour during major news events, leaving directional bets vulnerable. That's where forex options change the game. Instead of buying or selling a pair outright and hoping the market cooperates, you're purchasing the right to transact at a specific rate, with your maximum loss capped at the contract cost from day one.

For businesses paying overseas suppliers or active traders managing multiple positions, options create asymmetric risk profiles you can't replicate with spot trades alone. You might pay 60 pips for a EUR/USD put, but that premium buys protection against a 400-pip plunge—or lets the option lapse unused if the euro strengthens instead. This flexibility explains why institutional desks hold billions in notional option exposure and why more US retail traders are exploring currency derivatives beyond plain vanilla spot accounts.

We'll break down contract structures, option categories, what drives premium costs, real-world hedging scenarios, and how to execute your first trade through a CFTC-registered platform.

What Are Forex Options and How Do They Work

Think of a forex option as an insurance policy on an exchange rate. You pay a one-time fee (the premium) for protection against unfavorable currency moves, but if the market swings your way, you're free to ignore the contract and trade at the better spot price. That one-sided obligation is the core difference from futures or forwards, which lock you into settlement regardless of where rates go.

Call and put options forex split into two camps. Buy a call when you expect the base currency to appreciate; you're securing the right to purchase it at your chosen strike. EUR/USD calls at a 1.1200 strike let you acquire euros at that level even if the pair rockets to 1.1500. Puts work in reverse—they grant the right to sell the base currency at the strike, hedging against depreciation. A GBP/USD put at 1.2600 caps your downside if sterling tumbles to 1.2200.

Profit mechanics depend on where spot settles relative to your strike. Long a call? You're in the money when spot exceeds strike plus premium. Long a put? You profit when spot falls below strike minus premium. The seller (writer) pockets that upfront premium but faces potentially unlimited risk if the market moves sharply against them, which is why brokers impose strict margin requirements on short option positions.

How currency options work in settlement can follow two paths. Physical delivery means you actually exchange the underlying currencies at the strike rate—common in institutional OTC contracts where corporations need real euros or yen for payables. Cash settlement simply pays the intrinsic value difference in a single currency, which most retail traders prefer to avoid dealing with actual foreign-exchange logistics. CME currency futures options, for instance, settle to the underlying futures contract, which can then be closed or delivered.

Contract sizes vary widely. Standard OTC options might reference one million units of base currency, while CME micro options on EUR/USD cover just 12,500 euros, lowering the barrier for smaller accounts. Expiration tenors range from overnight binary options (pure directional bets on a single session) to multi-year LEAPS-style structures for long-term hedgers, though most liquidity clusters around one-week, one-month, and three-month maturities.

Options provide asymmetric risk profiles that spot positions cannot replicate. A corporate treasurer can cap downside exposure to adverse rate moves while retaining the ability to benefit if the currency swings favorably—something a forward contract simply doesn't allow

— Michael Hartley

Types of Currency Options You Should Know

Option contracts come in multiple flavors beyond the basic call/put split. Structural tweaks—exercise windows, barrier triggers, payout formulas—determine which scenarios pay off and which leave you empty-handed.

Vanilla Options in Forex

Vanilla options forex strip away all exotic features. One strike. One expiration. Straightforward in-the-money payout based on spot at maturity or exercise. No knock-outs, no digitals, no averaging formulas. EUR/USD vanilla puts simply give you the right to sell euros at the strike; if spot is below that level at expiry, you exercise and pocket the difference (minus premium paid upfront).

Why trade vanilla when cheaper structures exist? Liquidity. Vanilla contracts on major pairs like EUR/USD, USD/JPY, and GBP/USD maintain tight bid-ask spreads because dealers can easily hedge their exposure in the spot and futures markets. You can enter and exit positions mid-life without paying a massive spread penalty, which matters if you're actively managing a portfolio rather than holding to expiration.

Most US retail brokers listing currency options stick to vanilla contracts on futures—thinkorswim, Interactive Brokers, Tastytrade all fit this mold. The standardized terms and transparent pricing make them ideal for anyone building foundational option skills before graduating to exotics.

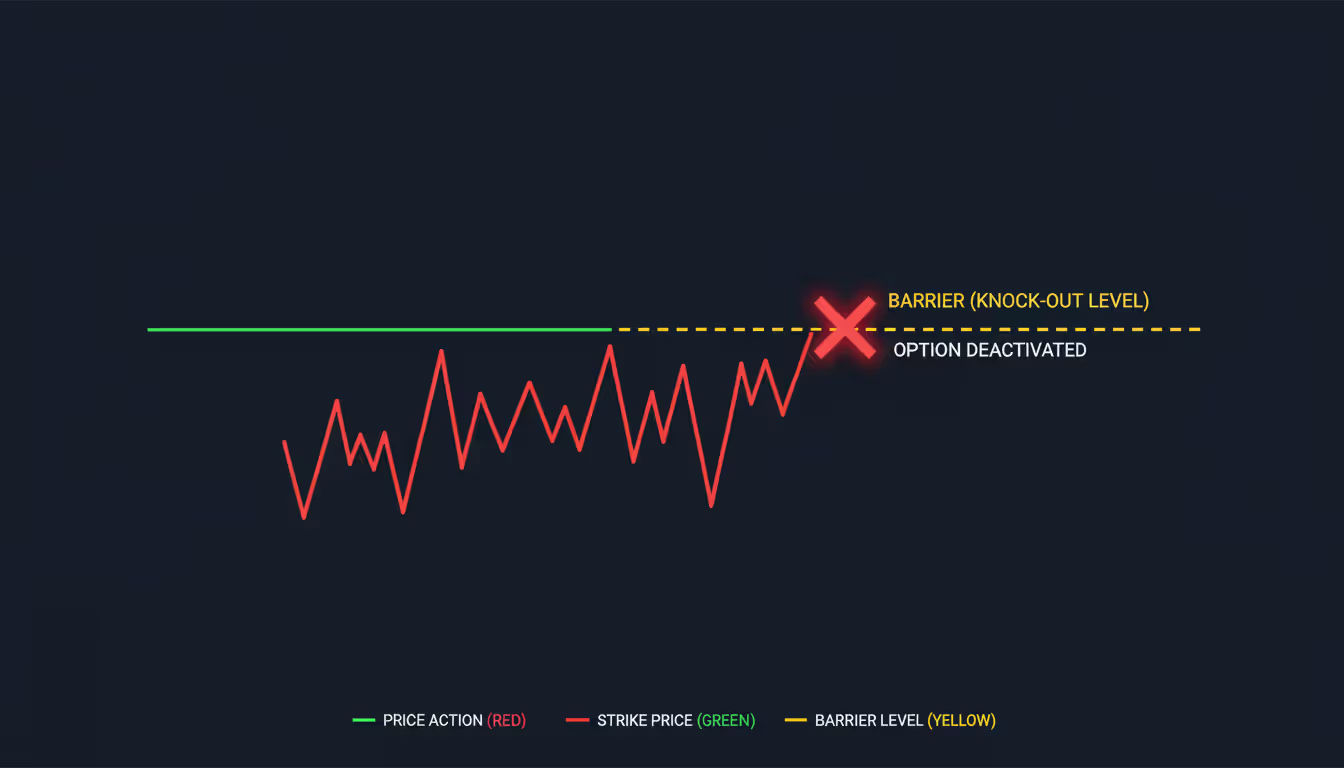

Barrier Options and Exotic Variants

Barrier options currency contracts add conditional triggers. A "knock-in" call only activates if spot touches a specified barrier before expiration; until then, it's dormant. A "knock-out" put disappears forever if the barrier is breached, refunding a small rebate or nothing at all depending on terms. Imagine you're long a USD/JPY call struck at 148.00 with a knock-out at 152.00. If dollar/yen climbs to 152.01, your option vanishes instantly, even if weeks remain until expiry.

The trade-off? Barriers slash premium costs—sometimes by 30% to 50% versus equivalent vanilla options—because the seller's risk is capped. A corporate treasurers expecting moderate dollar weakness might buy a EUR/USD knock-in put at 1.0800 that only activates if spot falls to 1.0750 first. If the euro stays above 1.0750 the entire time, no protection kicks in, but they paid half the premium of a vanilla put.

Other exotic formats include digital options (pay a fixed $1,000 if EUR/USD closes above 1.1000, zero otherwise) and Asian options that settle based on the average spot rate over the contract life, smoothing out single-day manipulation risk. These suit sophisticated users who want precise payoff profiles or need to reduce hedging costs in tight-margin businesses. The downside: exotics are illiquid, hard to unwind early, and require deep understanding of trigger mechanics to avoid surprises.

Author: Ethan Blackwell;

Source: martinskikulis.com

European vs American Exercise Styles

European vs American currency options dictate when you can pull the trigger. European-style contracts allow exercise only at expiration—think of them as "take it or leave it" on the final day. American-style contracts permit exercise any business day before expiry, giving you flexibility to lock in gains early if the market moves sharply in your favor.

Most OTC forex options follow European convention, simplifying dealer hedging and pricing models. Exchange-traded options on CME currency futures lean American, which marginally increases premiums because that early-exercise optionality has value. When might you exercise an American option early? If the interest-rate differential between currencies is wide and you hold an in-the-money call, you might exercise early to start earning carry on the high-yielding currency. With European options, you wait until expiration and miss out on days or weeks of interest.

Here's how vanilla and barrier options stack up in practice:

Your choice hinges on three factors: how confident you are in your exchange-rate forecast, how much premium you're willing to spend, and whether you need the flexibility to exit mid-contract. Beginners gravitate toward vanilla options for transparency and liquidity, while institutional desks layer in barriers to optimize cost versus coverage.

Understanding Forex Option Pricing and Premium

Forex option premium isn't plucked from thin air—six measurable inputs feed pricing models, and understanding them helps you spot expensive versus cheap contracts.

Spot rate versus strike distance – An option already in-the-money carries intrinsic value (the immediate profit if you exercised now). Out-of-the-money options have zero intrinsic value; their premium reflects pure time value and volatility expectations.

Time remaining until expiration – More days on the clock mean more opportunities for favorable moves. A 90-day option costs significantly more than a 30-day option at the same strike, all else equal. That extra time value erodes steadily as expiration approaches—a phenomenon called theta decay.

Implied volatility – The market's forecast of how much the currency pair will swing. When the VIX equivalent for FX spikes before a Federal Reserve meeting or Brexit vote, premiums jump across all strikes because larger expected moves increase the chance of landing in-the-money.

Interest-rate differential – Currencies don't pay dividends, but they do carry interest. If US rates sit at 5% and eurozone rates at 3%, holding dollars earns you 2% more per year. That differential skews EUR/USD option prices: calls become pricier (you're buying the lower-yielding euro) and puts cheaper (selling the euro is less costly). Forward points bake this into strike pricing.

Supply-demand imbalances – During crisis periods, everyone rushes to buy downside protection. USD/JPY puts might trade at implied volatilities 3–5 points above calls purely from hedging demand, creating skew that deviates from theoretical fair value.

Bid-ask spread – Liquid pairs like EUR/USD might show a 2-pip spread on at-the-money options, while exotic pairs like USD/ZAR can have 20-pip spreads, effectively raising your entry cost.

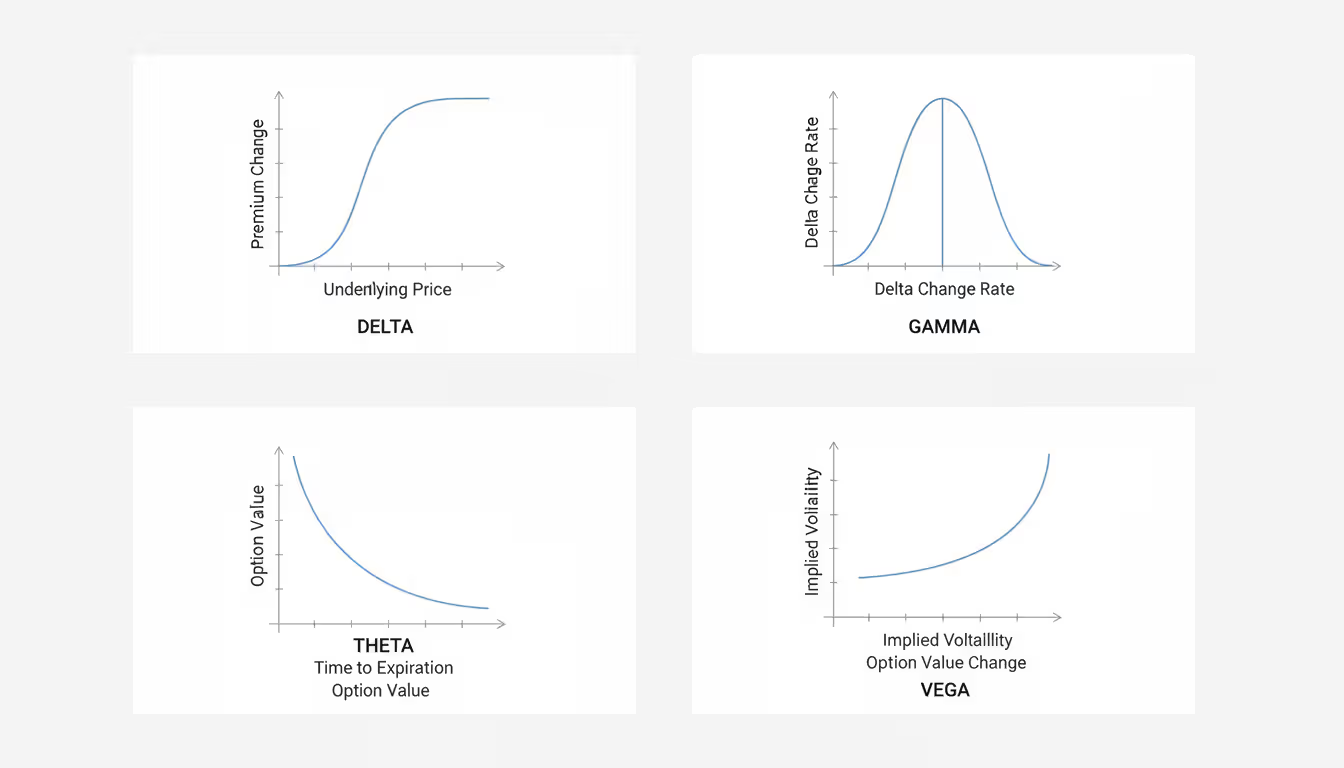

Option delta in currency markets quantifies sensitivity to spot moves. A delta of 0.40 means the option premium rises roughly 0.40 pips for every 1-pip increase in the underlying pair (for calls; puts carry negative delta). Delta also approximates probability: a 0.25-delta call has about a 25% chance of expiring in-the-money under risk-neutral assumptions.

Traders use delta to hedge dynamically. Suppose you've sold ten EUR/USD calls with 0.50 delta at a 100,000-unit contract size. You're effectively short 500,000 euros (10 contracts × 100,000 × 0.50). To neutralize directional risk, you'd buy 500,000 euros in the spot market, creating a delta-neutral position. As spot moves, delta shifts—that's where gamma comes in, measuring the rate of delta change.

Vega tracks how a 1% shift in implied volatility affects premium. Before major announcements, vega exposure explodes; owning options ahead of a European Central Bank decision can be profitable even if spot barely moves, as long as implied vol spikes. Thetaquantifies daily time decay. An at-the-money option with two weeks to expiry might lose 3 pips per day; in the final three days, theta accelerates to 10+ pips daily, eroding value fast if spot stays flat.

Author: Ethan Blackwell;

Source: martinskikulis.com

Retail platforms display premiums in pips or percentages of notional. A 70-pip premium on a EUR/USD standard lot (100,000 euros) equals $700. Comparing premiums across strikes reveals the volatility smile: out-of-the-money puts on risk-off pairs like USD/JPY often cost more than equivalent calls, reflecting crash-hedging demand. Scanning implied volatilities helps you identify relatively cheap or expensive options before committing capital.

Common Option Strategies for Forex Markets

Option strategies for forex let you tailor risk-reward profiles beyond simple long calls or puts. Below are five go-to approaches that work across different market conditions.

1. Protective put (insurance hedge) You already own a long position—maybe you're long GBP/USD spot at 1.2700 from last week—and you're worried about a Bank of England surprise. Buy a 1.2650 put for, say, 40 pips. If sterling crashes to 1.2400, your spot position loses 300 pips, but the put gains roughly 210 pips (250 intrinsic minus 40 premium), capping total damage at 130 pips. If sterling climbs, you participate fully, just out the 40-pip premium. It's portfolio insurance with a deductible.

2. Covered call (income generation) Hold long EUR/USD spot and sell an out-of-the-money call at 1.1100 when spot is 1.0950. You collect, say, 30 pips upfront. If the euro stays below 1.1100, the call expires worthless and you keep the premium as extra yield. If EUR/USD rallies to 1.1200, you deliver euros at 1.1100, capping your gain at 150 pips (spot rise) plus 30 pips (premium) = 180 pips. This suits sideways markets where you don't expect explosive moves but want to monetize time decay.

3. Straddle (volatility play) Purchase both a call and a put at the same strike—let's say 1.1000 on EUR/USD—with matching expirations. Total cost might be 80 pips. You're betting on a big move in either direction: if the pair jumps to 1.1150 or plunges to 1.0850, one leg pays off enough to cover both premiums. Straddles shine around FOMC meetings, NFP releases, or geopolitical shocks where you expect fireworks but don't know which way the market will break.

4. Strangle (cheaper volatility bet) Similar setup, but strikes are out-of-the-money: buy a 1.0900 put and a 1.1100 call when spot is 1.1000. Combined premium drops to, say, 50 pips because neither option has intrinsic value. You need a larger move (past 1.0850 or 1.1150) to break even, but lower upfront cost means less capital at risk if the market stays calm.

5. Vertical spread (bull call or bear put) Construct a bull call spread by buying a 1.1000 call and selling a 1.1100 call, both expiring in 30 days. Net premium might be 30 pips (you paid 50, collected 20). Maximum profit is 100 pips (strike difference) minus 30 = 70 pips if EUR/USD closes above 1.1100. Maximum loss is the 30-pip net premium if EUR/USD stays below 1.1000. Spreads reduce cost and risk, ideal when you have a modest directional view but don't want to pay full freight for a naked long option.

Each setup has a breakeven calculation and a payoff diagram you should sketch before entering. Many platforms offer strategy builders that auto-populate legs and display Greeks, but understanding the mechanics yourself prevents costly mistakes like selling naked options without realizing your risk is theoretically unlimited.

How to Hedge Currency Risk with Forex Options

How to hedge with forex options revolves around protecting cash flows or portfolio value from adverse FX moves without locking yourself into a fixed rate that eliminates upside.

Scenario: US importer buying European goods Your company owes €250,000 in 60 days for a container shipment. Spot EUR/USD sits at 1.0900, and you're budgeting $272,500 (1.0900 × €250,000). But if the euro strengthens to 1.1200, your cost jumps to $280,000—an extra $7,500 you didn't plan for. You could buy a forward contract at 1.0920, locking the rate but forfeiting any benefit if the euro weakens. Instead, purchase a EUR/USD call struck at 1.0950 for 40 pips (€1,000 premium). If EUR/USD rallies to 1.1200, you exercise at 1.0950, paying $273,750 plus the $1,000 premium = $274,750—well below the $280,000 worst case. If the euro drops to 1.0700, you let the call expire and buy spot, paying $267,500 + $1,000 = $268,500, still cheaper than the original budget.

Scenario: Active forex trader protecting open positions You're long AUD/USD at 0.6600 with a 100-pip profit target at 0.6700 but nervous about a Reserve Bank of Australia surprise tonight. Buy a 0.6550 put for 25 pips. If the Aussie collapses to 0.6400 overnight, your spot position loses 200 pips, but the put gains 150 intrinsic (0.6550 – 0.6400) minus 25 premium = 125 pips, cutting total loss to 75 pips. If AUD/USD soars to 0.6750, you bank your 150-pip spot gain minus the 25-pip put cost = 125 net. The put acts as a trailing stop with upside flexibility.

Options versus forwards for corporate hedging Forwards eliminate uncertainty—finance teams love that for budgeting. Lock a 1.1000 EUR/USD forward and your payable costs exactly that, no surprises. But if the euro drops to 1.0700, you're stuck paying 300 pips above market. Options cost premium upfront (cash outflow today) but preserve favorable outcomes. CFOs often blend both: cover baseline exposure with forwards, use options for contingent exposures (bids on overseas contracts you might win) or incremental layers where budget flexibility exists.

A frequent misstep: buying far out-of-the-money strikes to save premium. A 1.1200 call costs 15 pips versus 50 pips for a 1.0950 strike, tempting when budgets are tight. But that 1.1200 strike offers no real protection unless the euro skyrockets. Balancing premium cost against realistic volatility scenarios ensures your hedge actually activates when you need it.

Author: Ethan Blackwell;

Source: martinskikulis.com

Getting Started with Currency Options Trading

Forex options trading through a US retail account centers on exchange-traded options on currency futures. The CFTC and NFA regulate these markets tightly, so your first step is opening an account with a registered futures commission merchant—Interactive Brokers, TD Ameritrade's thinkorswim, or Tastytrade all fit the bill.

Account setup and approval levels Brokers walk you through a suitability questionnaire covering trading experience, net worth, income, and risk tolerance. Options approval tiers range from Level 1 (covered calls, protective puts) to Level 4 or 5 (naked shorts, complex multi-leg spreads). Expect to start at Level 2 or 3, which covers most strategies retail traders need. Minimum account sizes vary—some brokers accept $2,000 for micro contracts, others want $5,000+ for standard futures options.

Platform features that matter Real-time Greeks (delta, gamma, vega, theta) should display automatically on option chains. Integrated probability analysis—cones showing likely price ranges—helps you choose strikes. Strategy builders let you click "bull call spread" and the platform populates both legs, calculates max profit/loss, and displays breakeven prices. Paper-trading modes (simulated accounts) let you practice without risking real money; run a few dozen paper trades before going live to internalize how options behave as expiration nears.

Risk management essentials Cap single-position risk at 2% to 5% of account equity. A $10,000 account shouldn't risk more than $200–$500 on any one option trade. Monitor Greeks daily—delta shifts as spot moves, and a delta-neutral portfolio at 9 a.m. can be directional by noon if volatility spikes. Set alerts for significant spot moves or implied-vol changes that might warrant adjusting or closing positions early. Keep a trade log noting entry rationale, initial Greeks, market conditions, and post-mortem analysis of what worked or failed. Reviewing past trades sharpens pattern recognition faster than any textbook.

Tax and regulatory nuances Exchange-traded options on currency futures fall under Section 1256 contracts for US tax purposes: 60% long-term / 40% short-term capital gains split regardless of holding period, and mark-to-market accounting at year-end. OTC forex options (if you access them through an institutional broker) may be taxed as ordinary income. Consult a CPA familiar with derivatives—missteps here can turn a profitable year into a tax headache.

Starting small with micro contracts (1/10 the size of standard) lets you learn Greeks behavior and payoff dynamics without betting the farm. Most beginners blow up their first few trades from overleverage or ignoring theta decay; keeping position sizes modest gives you room to learn from mistakes.

Frequently Asked Questions About Forex Options

Can I trade forex options in the US?

Absolutely—US retail traders access currency options primarily through CME-listed contracts on futures, traded via CFTC-regulated brokers like Interactive Brokers, thinkorswim, or Tastytrade. OTC forex options exist but typically require institutional accounts, prime-brokerage relationships, or accredited-investor status, along with higher minimums (often $100,000+). If you're starting out, exchange-traded options on EUR/USD, GBP/USD, or JPY/USD futures are the accessible route.

What's the difference between forex options and spot forex trading?

Spot forex means you buy or sell a currency pair outright—long EUR/USD at 1.1000, and you profit or lose tick by tick as the market moves. Your risk is theoretically unlimited (though stop-losses help). Options give you a contract that expires—you pay premium upfront, and your maximum loss is that premium, full stop. If you're wrong, the option expires worthless, but you never face margin calls or slippage beyond your initial cost. Spot is simpler for directional bets; options add complexity but also asymmetric risk profiles.

How much does a forex option contract cost?

Premiums vary wildly based on strike, expiration, volatility, and pair. An at-the-money one-month EUR/USD option might run 60 pips (roughly $600 per 100,000-euro contract). Out-of-the-money strikes cost less—maybe 20 pips—while in-the-money options carry intrinsic value that inflates the price. CME micro options on 12,500-euro notional bring costs down proportionally, making them beginner-friendly. Check real-time quotes; premiums shift minute by minute as spot and implied vol move.

Do forex options expire worthless?

Yes, and it happens constantly. Any option finishing out-of-the-money at expiration has zero value—the buyer loses the entire premium, and the seller keeps it as profit. Far out-of-the-money options frequently expire worthless, which is why they're cheap upfront. If you bought a EUR/USD 1.1500 call for 10 pips and the pair closes at 1.1200 at expiry, you're out 10 pips with nothing to show. Sellers count on this; around 60–70% of options expire worthless industry-wide, though exact stats vary by market conditions.

Are currency options better than futures for hedging?

Depends what you value. Futures and forwards lock in a rate with no upfront cash outlay (just margin), perfect for precise budgeting—you know your cost to the pip. But you're stuck with that rate even if the market moves favorably. Options cost premium today yet let you walk away and trade spot if conditions improve. Corporations often use futures for core exposure and options for contingent or incremental hedges. Neither is universally "better"; they serve different goals.

What brokers offer forex options to US traders?

Interactive Brokers, TD Ameritrade (thinkorswim platform), and Tastytrade all provide CME currency futures options with transparent pricing. Saxo Bank and IG Group offer OTC forex options in certain account tiers, typically aimed at higher-net-worth or institutional clients. Always verify CFTC and NFA registration, compare commission structures (per-contract fees plus exchange fees add up fast), and test the platform's options chain and analytics tools before committing serious capital.

Currency options aren't a magic bullet, but they're one of the few instruments that let you define risk precisely while keeping upside open-ended. Whether you're a business treasurer protecting next quarter's euro payable, a trader layering insurance onto an existing position, or a speculator betting on post-Fed volatility, options offer payoff structures spot and futures can't match.

Start by mastering vanilla calls and puts on liquid pairs. Understand how delta, theta, and vega interact. Paper-trade a handful of strategies—protective puts, straddles, spreads—so you see how time decay and spot moves affect P&L in real time. Once the mechanics click, options become a natural extension of your toolkit, balancing cost, flexibility, and that asymmetric edge that keeps institutional desks holding trillions in notional exposure worldwide.

Open a demo account, pull up a EUR/USD option chain, and place your first simulated trade this week. The learning curve is steeper than spot forex, but the strategic possibilities make it worth the climb.

Swap rates represent the interest cost or credit applied when forex traders hold positions past the daily rollover time. Understanding how these overnight fees work, when you pay or earn them, and their cumulative impact is essential for swing traders and anyone implementing carry trade strategies in 2026

Spread betting lets you speculate on market moves without owning the asset. This guide walks through real examples—long and short positions, forex pairs, margin calculations—showing exactly how profits and losses accumulate, how to size stakes responsibly, and what happens when trades go wrong

An overnight index swap is a derivative where parties exchange fixed and floating interest payments based on compounded overnight rates. These instruments have become the standard for derivatives discounting and provide key insights into central bank policy expectations and market stress levels

Interest rate movements can transform profitable loans into financial burdens overnight. Companies with floating-rate debt and bond investors face the same challenge: protecting against adverse rate shifts without sacrificing upside. This guide explains hedging instruments, duration strategies, and how to match protection to your specific exposure

The content on this website is provided for general informational and educational purposes only. It is intended to explain concepts related to Forex (FX) trading, currency markets, leverage, hedging, and risk management.

All information on this website, including articles, guides, and examples, is presented for general educational purposes. Forex trading carries significant risk, and outcomes may vary depending on market conditions, leverage, and individual decisions.

This website does not provide financial, investment, or trading advice, and the information presented should not be used as a substitute for consultation with qualified financial professionals.

The website and its authors are not responsible for any errors or omissions, or for any outcomes resulting from decisions made based on the information provided on this website.