Most currency traders stick with the over-the-counter spot forex market. I get it—platforms like MetaTrader make it easy. But there's another way to get currency exposure that sidesteps many OTC headaches: exchange-traded futures. These contracts lock in future exchange rates through centralized marketplaces, not bilateral dealer relationships. You'll deal with quarterly expirations, standardized sizes, and margin rules that work completely differently from retail forex accounts. Whether that trade-off makes sense depends on what you're trying to accomplish and how much you value things like regulatory oversight and transparent pricing.

What Are FX Futures Contracts?

An FX futures contract obligates you to exchange one currency for another at a predetermined rate when the contract expires. Nothing is negotiable. The Chicago Mercantile Exchange already baked in every specification—the notional amount, the minimum price fluctuation, the settlement procedure, the expiration calendar.

Let's look at EUR/USD, the busiest currency future. Each contract represents €125,000. Period. The quoted price tells you how many U.S. dollars each euro costs. The minimum price movement (a "tick") equals 0.0001, worth $12.50 per contract. So if the March contract moves from 1.0850 to 1.0851, you just made or lost $12.50 depending on which side you took.

Going long one EUR/USD contract means you profit when the euro appreciates against the dollar. You've effectively agreed to accept euros while paying dollars at the contract price. Euro climbs from 1.0850 to 1.0900? That's a 50-tick gain—$625 in your pocket. Euro drops 50 ticks? You're down $625. The bilateral currency relationship works exactly like spot forex in this regard.

What the CME defines upfront:

Notional value: How much base currency the contract covers (€125,000 for euros, £62,500 for sterling, ¥12,500,000 for yen)

Minimum fluctuation: The tick size and its dollar value per contract

Expiration schedule: Standard quarterly cycle (March/June/September/December) with serial months added for heavily traded pairs

Settlement process: Most contracts now cash-settle against a reference rate; physical currency delivery still exists but rarely happens

Trading window: Electronic trading runs nearly 24/5, matching the global foreign exchange market's schedule

Author: Marcus Ellington;

Source: martinskikulis.com

The clearinghouse becomes the counterparty to every single transaction. Sold a contract? The clearinghouse is your buyer. Bought one? The clearinghouse is your seller. This legal structure eliminates the credit risk inherent in OTC forward agreements where you're relying on a specific bank or corporation to honor its obligation months down the road.

How FX Futures Are Traded on US Exchanges

CME's Globex platform opens Sunday evening around 6 PM Eastern and runs straight through until Friday afternoon with just a brief maintenance window each day. This schedule mirrors the 24-hour nature of currency markets—Tokyo participants can trade during their business hours, London traders don't wait for New York, and California-based hedge funds can put on positions before sunrise.

You'll need an account with a futures commission merchant. That's industry jargon for a brokerage licensed to handle futures transactions. Plenty of retail-friendly platforms now offer futures access alongside equities and options. Interactive Brokers, TD Ameritrade's thinkorswim, TradeStation—they all provide CME currency futures. Institutional traders often maintain relationships with prime brokers or trade directly through proprietary infrastructure.

Your initial margin deposit gets posted immediately. This isn't payment—you're not buying anything yet. It's a performance bond guaranteeing you can cover potential losses. Post $3,000 for a single EUR/USD contract and suddenly you're controlling €125,000 of currency exposure (roughly $135,000 at current rates). That degree of leverage amplifies everything.

The standard order types all work:

Market orders execute instantly at the best available price this second

Limit orders specify your maximum buying price or minimum selling price, then wait for someone to meet your terms

Stop orders trigger at a designated price level and immediately become market orders

Stop-limit combinations add another layer of price control at the cost of execution certainty

CME also lists E-micro contracts at one-tenth the standard size. E-micro EUR/USD covers €12,500 instead of €125,000. Smaller accounts can participate without massive leverage, and hedgers gain precision when their exposure doesn't fit neatly into full-size contract increments.

Volume clusters heavily in the front-month contract—whichever expiration comes next. Bid-ask spreads tighten down to one tick there, order flow is deepest, and execution quality peaks. Several days before the last trading day (which varies by contract but typically precedes the official expiration), most traders shift their positions forward to the next quarterly month. This "roll" maintains their market exposure without dealing with settlement procedures. The exchange publishes settlement prices, volume statistics, and open interest figures every day—transparency you simply don't get in bilateral OTC markets.

One formatting quirk confuses newcomers: Japanese yen futures quote as dollars per yen (0.008500 for example), while spot forex platforms show USD/JPY the opposite way (117.65). Same exchange rate, inverted presentation. Always double-check you understand the contract's quotation convention before placing your first order.

Author: Marcus Ellington;

Source: martinskikulis.com

FX Futures vs Forward Contracts and OTC Markets

Both instruments lock in future exchange rates. The structural architecture determines which tool serves your needs better.

Exchange-Traded vs OTC FX Products

Currency futures trade on regulated exchanges where every contract is identical. All EUR/USD futures share the same size, expiration dates, and tick value. This uniformity concentrates liquidity in the most popular contracts. Pricing happens in full public view—everyone sees identical quotes simultaneously. The clearinghouse stands behind every transaction, so you never research counterparty balance sheets or credit ratings.

Forward contracts are private bilateral agreements, typically arranged through your bank's foreign exchange desk. Everything gets negotiated. Need to hedge €3.7 million exactly 73 days from now? A forward contract matches that precise amount and timeline. Futures force you to round—maybe 29 or 30 standard contracts (€3,625,000 or €3,750,000)—and since standardized expirations don't offer a 73-day option, you're accepting basis risk or planning to roll positions at quarterly intervals.

That customization comes at a price: counterparty credit exposure. Your OTC forward only performs if the other party can and will honor the contract when settlement arrives. Major international banks are solid, but smaller regional institutions or thinly capitalized corporations introduce risk that simply doesn't exist with exchange-traded futures. Banks typically don't require upfront margin for forwards, though they impose credit lines and may demand collateral based on your financial standing.

Characteristic

Exchange-Traded Futures

OTC Forward Agreements

Where they trade

Centralized exchanges (primarily CME)

Private negotiations with banks and dealers

Terms

Exchange sets all specifications in advance

Parties negotiate every detail to fit their needs

Credit exposure

Clearinghouse guarantee removes counterparty risk

Direct reliance on the other party's creditworthiness

Collateral

Mark-to-market system with daily variation margin

Generally none upfront; depends on bilateral credit agreement

Market depth

Concentrated liquidity in major pairs with visible order books

Depends on dealer relationships; pricing opacity

Oversight

CFTC regulation plus exchange rules

Less stringent framework; contract terms govern

How they settle

Cash settlement against reference rate is standard

Typically involves actual currency exchange or negotiated cash settlement

Futures Delivery vs Cash Settlement

The vast majority of futures traders close out their positions well before expiration arrives. But the settlement mechanism still matters if you forget to exit or deliberately hold through the delivery period.

Cash settlement means the clearinghouse calculates the difference between your contract price and a final reference rate taken from the spot market, then transfers the profit or loss in dollars. No actual foreign currency changes hands. EUR/USD futures use CME's proprietary spot rate fix for this calculation. It's straightforward and final.

Physical delivery means actually swapping currencies. Hold a long position into delivery? You pay the contracted dollar amount and receive the foreign currency through coordinated bank transfers. Banks charge fees for this service. Most retail brokers prohibit it entirely and will forcibly liquidate your position days before expiration to avoid the operational headache.

Traditional OTC forwards in the interbank market typically involve actual currency exchange—the U.S. exporter converting euro receipts to dollars, the importer paying yen to Japanese suppliers. Non-deliverable forwards (NDFs) settle in cash and get used primarily for currencies subject to capital controls or limited convertibility.

Contract Specifications and Margin Requirements

Knowing the exact contract terms prevents expensive surprises. CME publishes complete specifications for each currency pair; here are the most actively traded:

Pair

Notional Size

Minimum Price Move

Traded On

Approximate Margin (2026)

EUR/USD

€125,000

$12.50 per tick

CME Globex

$2,500–$3,200

GBP/USD

£62,500

$6.25 per tick

CME Globex

$2,800–$3,500

JPY/USD

¥12,500,000

$12.50 per tick

CME Globex

$2,200–$2,900

AUD/USD

A$100,000

$10.00 per tick

CME Globex

$1,800–$2,400

CAD/USD

C$100,000

$10.00 per tick

CME Globex

$1,600–$2,100

Margin levels fluctuate with market volatility. Both the exchange and your specific broker determine these amounts. The ranges shown reflect typical levels for standard-size contracts.

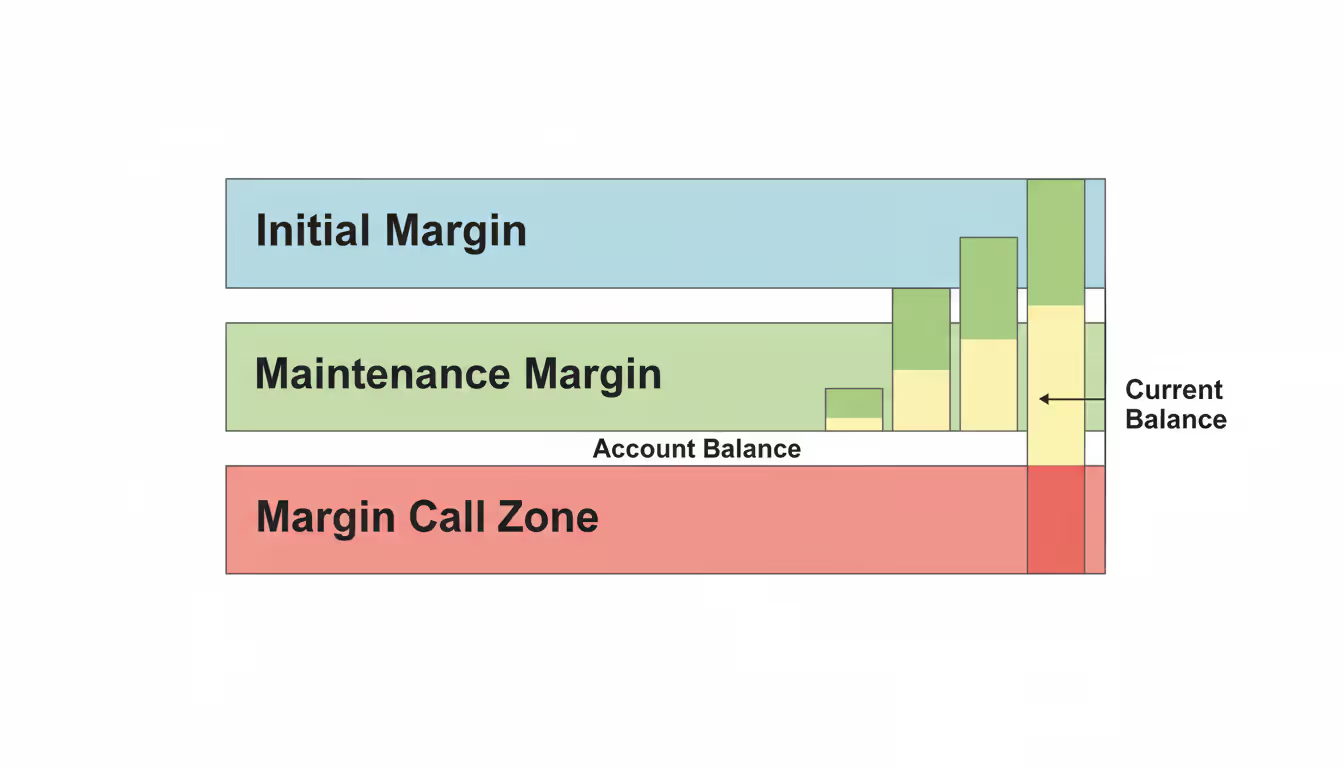

Initial margin represents the deposit you must post to establish a position. It's not a purchase price—think of it as a good-faith bond guaranteeing you can handle adverse moves. Deposit $3,000 to open one EUR/USD contract and you're suddenly controlling €125,000 of notional exposure—approximately $135,000 worth at a 1.0800 exchange rate. Leverage this extreme cuts both ways in a hurry.

Maintenance margin defines the lowest account equity allowed before action becomes necessary. Your account balance drops below this threshold due to losing trades? Your broker issues a demand for additional funds. Fail to meet that demand? Your position gets closed whether you like it or not.

These requirements shift constantly based on volatility. During turbulent periods—surprise central bank announcements, geopolitical crises, sudden government interventions in currency markets—the exchange raises margin levels to protect the clearinghouse system. You might open a trade requiring $2,500, then see that requirement jump to $4,000 the following week. Now you need to deposit more money even though your position hasn't moved against you yet.

Author: Marcus Ellington;

Source: martinskikulis.com

Intraday margin typically runs lower than overnight requirements, favoring day traders. Close all positions before the session ends and you trade with reduced margin—effectively higher leverage. This approach demands strict discipline and solid risk controls since a sharp move against you can wipe out an account before protective stops trigger.

Managing FX Futures Positions

Position management extends well beyond timing your entry and exit. The quarterly expiration cycle creates operational considerations that don't exist when trading spot forex or stocks.

Rolling FX Futures Positions

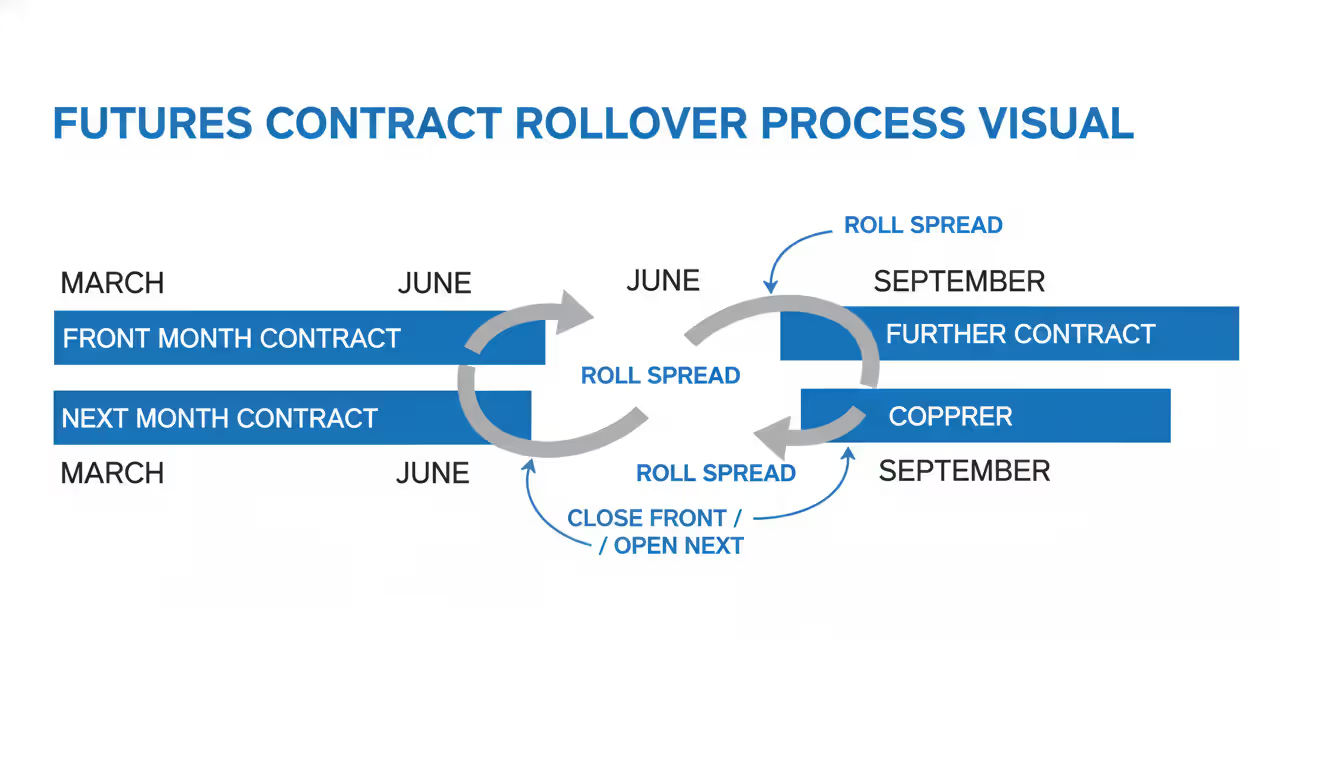

Currency futures expire every three months, but plenty of traders and hedgers need exposure stretching beyond a single contract cycle. Rolling involves simultaneously closing your expiring position and opening an identical position in a later expiration month.

The price gap between the nearby and deferred contracts—called the "calendar spread" or "roll differential"—reflects interest rate differences between the two currencies. U.S. rates running higher than eurozone rates? The June EUR/USD contract will trade at a discount to the March contract, costing you a bit when you roll forward. Eurozone rates higher instead? Rolling produces a small credit.

Most market participants execute the roll several days before the last trading day to dodge the settlement process and stay in whichever contract offers the best liquidity. Large institutions sometimes spread the roll over multiple sessions to minimize market impact from big position adjustments. Retail traders holding just a few contracts generally roll everything in a single transaction.

E-mini and E-micro contracts sometimes improve roll flexibility. A corporate hedger with 15 standard EUR/USD contracts might roll 10 to the next quarterly expiration and deploy E-minis for the remaining exposure, achieving finer precision than standard contracts alone allow.

Author: Marcus Ellington;

Source: martinskikulis.com

FX Futures Liquidity by Currency Pair

Trading experience varies dramatically across different currency pairs. EUR/USD futures absolutely dominate—spreads frequently just one tick wide, order books showing significant size on both the bid and offer. GBP/USD, JPY/USD, and CHF/USD also trade actively, though spreads widen slightly compared to the euro.

Less common pairs like the Mexican peso or Brazilian real see lower participation and wider spreads. Entering or exiting large positions moves prices noticeably, and stop orders might fill at levels far from your designated trigger during volatile moments. Traders working these contracts rely more heavily on limit orders and accept slower fills to avoid paying excessive transaction costs.

Time of day significantly impacts execution quality. EUR/USD and GBP/USD liquidity peaks during the European-American overlap window (roughly 8 AM to noon Eastern). JPY/USD activity increases when Tokyo markets are open. Trade during off-peak hours and you risk poor execution even in major pairs.

Open interest—the total number of outstanding contracts—provides another useful liquidity indicator. High open interest signals many participants holding positions, which typically correlates with better execution. A sudden drop in open interest as expiration nears tells you traders are rolling to the next contract month, and spreads might temporarily widen during that transition.

Using FX Futures for Hedging Currency Risk

Companies and investors use currency futures to lock in exchange rates, protecting budgets and returns against adverse currency movements. The standardized format makes futures accessible to more participants than custom OTC forwards, though you sacrifice the ability to match hedge ratios perfectly.

Picture a U.S. electronics retailer importing components from Germany. The company commits to a €2.5 million payment in three months. What happens if the euro strengthens against the dollar? Their cost in dollar terms increases. To eliminate this uncertainty, the retailer purchases 20 EUR/USD futures contracts (20 × €125,000 = €2.5 million). If the euro appreciates, the futures contracts gain value, offsetting higher import costs. If the euro weakens instead, the futures lose money—but the retailer pays less for goods anyway, so the overall result is still favorable despite the hedge loss.

The hedge won't be perfect. The futures expiration date probably won't align exactly with the actual payment date. The retailer might need to roll the contracts forward or accept some basis risk (the spread between the futures price and the spot rate when payment actually occurs). Daily mark-to-market creates cash flow volatility too. Euro initially weakens? The retailer must post variation margin even though the ultimate outcome (lower import costs) is positive.

Portfolio managers deploy currency futures to adjust foreign exchange exposure without liquidating underlying securities. A U.S.-based fund holding European equities faces euro exposure on those positions. Manager expects euro weakness? Selling EUR/USD futures provides a hedge without triggering capital gains taxes or incurring the transaction costs of selling the actual stocks. This technique proves especially useful for index funds or ETFs that can't easily adjust their holdings without tracking error.

FX futures offer a level of transparency and credit safety that's difficult to replicate in the OTC market. For institutional portfolios, the ability to hedge currency risk through a centrally cleared product with visible pricing is invaluable, especially in volatile markets where counterparty concerns resurface

— Michael Chen

Hedgers face a strategic choice between static hedging (fixed contract quantity) and dynamic hedging (adjusting positions as underlying exposure changes). Static hedges are operationally simpler but risk becoming over- or under-hedged if exposure shifts. Dynamic hedging requires constant monitoring and generates transaction costs from frequent adjustments.

Tax treatment influences hedging decisions too. U.S. tax law grants FX futures favorable 60/40 treatment under Section 1256—60% of gains receive long-term capital gains rates while 40% get taxed at short-term rates, regardless of your actual holding period. This can make futures more tax-efficient than spot forex for certain traders, though hedgers should consult tax professionals about how hedge accounting rules apply to their specific situations.

Frequently Asked Questions About FX Futures

How much money do I actually need to start trading FX futures?

Margin requirements for standard contracts typically run $2,000–$3,500 per contract, but most brokers impose higher account minimums—usually $5,000 to $10,000—as a volatility buffer. E-micro contracts lower the barrier considerably, with margins around $200–$350 per contract, making them accessible for traders with smaller accounts. But here's the reality: trading with just barely enough to meet minimum margin requirements leaves zero cushion for adverse price swings. You're one bad move from forced liquidation. Adequate capitalization beyond the bare minimum dramatically improves your survival odds.

Can regular retail traders actually access these markets?

Absolutely, yes. Retail traders open accounts with futures commission merchants (the regulatory term for futures brokers) that offer CME currency futures access. Most major online brokerage platforms now provide futures trading alongside stocks and options. The U.S. regulatory framework ensures retail participants receive the same pricing and execution quality as institutional traders—nobody gets special treatment on price. Commission structures vary considerably though. Some brokers specialize in active futures traders with low per-contract fees, while others bundle futures into broader brokerage services at higher costs.

What's the real difference between FX futures and the spot forex most people trade?

Spot forex operates over-the-counter through dealers and brokers—no centralized exchange, no uniform contracts. Positions don't expire, so you can theoretically hold them forever while paying or earning rollover interest each night. FX futures trade on regulated exchanges with standardized sizes and fixed quarterly expiration dates. Futures require margin posted through a clearinghouse with daily mark-to-market settlement, while spot forex margin practices vary wildly by broker. Tax treatment diverges significantly: futures automatically receive 60/40 capital gains treatment in the U.S., whereas spot forex profits typically count as ordinary income unless you make a Section 988 election. Futures also offer superior pricing transparency and eliminate counterparty credit risk entirely.

I forgot to close my position before expiration—what now?

Most currency futures settle in cash rather than requiring actual currency exchange. The clearinghouse calculates the difference between your contract price and the final settlement price (derived from a spot market reference rate), then credits or debits your account accordingly. No foreign currency actually changes hands. Long a EUR/USD contract you bought at 1.0850 and the final settlement comes in at 1.0900? You receive $625 (50 ticks × $12.50 per tick). Certain contracts still allow physical delivery, which means you'd actually exchange currencies through bank coordination—with extra fees attached. Most retail brokers prohibit physical delivery entirely and will force-close your positions several days before expiration to avoid the operational complexity.

Does the IRS treat FX futures differently than spot forex trading?

Yes, the tax treatment differs substantially. FX futures fall under Section 1256 of the tax code, automatically treating all gains and losses as 60% long-term and 40% short-term capital gains no matter how long you actually held the position. This blended rate often produces lower taxes than ordinary income rates. Spot forex typically gets taxed under Section 988 as ordinary income—unless you file an election to opt into Section 1256 treatment before your first trade of the calendar year. The 60/40 treatment applies automatically to exchange-traded futures without any paperwork, simplifying record-keeping significantly. That said, tax rules get complicated quickly, and individual circumstances vary enormously, so consulting a tax professional who understands derivatives makes sense.

Which currency pairs should I focus on for the best liquidity?

EUR/USD futures dominate every liquidity metric by a wide margin—tightest spreads, highest daily volume, deepest order book on both sides of the market. GBP/USD, JPY/USD, and CHF/USD also see active trading. Australian dollar, Canadian dollar, and New Zealand dollar futures offer moderate liquidity that works fine for most hedging applications and trading strategies, though spreads widen slightly. Emerging market currency futures—Mexican peso, Brazilian real, Russian ruble—have considerably lower participation, wider bid-ask spreads, and less predictable execution quality. If you trade these contracts, use limit orders religiously and avoid off-peak trading hours to minimize transaction costs.

Currency futures deliver a regulated, transparent mechanism for gaining foreign exchange exposure or managing cross-border exchange rate risk. The standardized contract terms, centralized clearinghouse model, and daily mark-to-market settlement distinguish them from OTC forwards and spot forex—offering clear advantages in counterparty safety and pricing visibility while imposing constraints around contract sizes and the quarterly expiration cycle.

Your choice between FX futures and alternative instruments depends entirely on what you're trying to accomplish. Businesses needing to hedge exact amounts on custom settlement dates may find OTC forwards more practical despite the counterparty risk. Active speculators seeking leverage combined with tax efficiency often prefer futures. Portfolio managers value the ability to adjust currency exposure without disturbing underlying security holdings or triggering taxable events.

Success trading or hedging with currency futures requires understanding contract specifications inside and out, mastering margin mechanics, and planning ahead for the quarterly roll process. Liquidity varies dramatically across currency pairs—execution quality in thinly traded contracts suffers considerably compared to EUR/USD. Proper position sizing and rigorous risk management become absolutely essential given the substantial leverage built into futures trading.

The regulatory infrastructure and exchange mechanisms supporting FX futures have evolved considerably over several decades, making these instruments accessible to a much broader range of market participants than in earlier years. Whether you're hedging commercial foreign exchange risk or speculating on exchange rate movements, currency futures provide a well-established toolkit backed by extensive market development, mature infrastructure, and comprehensive regulatory oversight.

Swap rates represent the interest cost or credit applied when forex traders hold positions past the daily rollover time. Understanding how these overnight fees work, when you pay or earn them, and their cumulative impact is essential for swing traders and anyone implementing carry trade strategies in 2026

Spread betting lets you speculate on market moves without owning the asset. This guide walks through real examples—long and short positions, forex pairs, margin calculations—showing exactly how profits and losses accumulate, how to size stakes responsibly, and what happens when trades go wrong

An overnight index swap is a derivative where parties exchange fixed and floating interest payments based on compounded overnight rates. These instruments have become the standard for derivatives discounting and provide key insights into central bank policy expectations and market stress levels

Interest rate movements can transform profitable loans into financial burdens overnight. Companies with floating-rate debt and bond investors face the same challenge: protecting against adverse rate shifts without sacrificing upside. This guide explains hedging instruments, duration strategies, and how to match protection to your specific exposure

The content on this website is provided for general informational and educational purposes only. It is intended to explain concepts related to Forex (FX) trading, currency markets, leverage, hedging, and risk management.

All information on this website, including articles, guides, and examples, is presented for general educational purposes. Forex trading carries significant risk, and outcomes may vary depending on market conditions, leverage, and individual decisions.

This website does not provide financial, investment, or trading advice, and the information presented should not be used as a substitute for consultation with qualified financial professionals.

The website and its authors are not responsible for any errors or omissions, or for any outcomes resulting from decisions made based on the information provided on this website.