A single quarter can tell the whole story. Your European supplier sends an invoice for €100,000. Three months ago, that meant $110,000. Today? Try $105,000. Sounds great—except you're the one selling to Europe and watching your dollar revenue shrink with every exchange rate tick. Currency swings don't care about your profit targets.

Here's what actually works when protecting your business from exchange rate chaos.

What Is Currency Risk and Why It Matters

Foreign exchange risk shows up whenever your money crosses borders. You've got exposure the moment you sign a contract in euros, report earnings from your Mexican subsidiary, or compete with imports priced in yen.

Three different flavors will hit you:

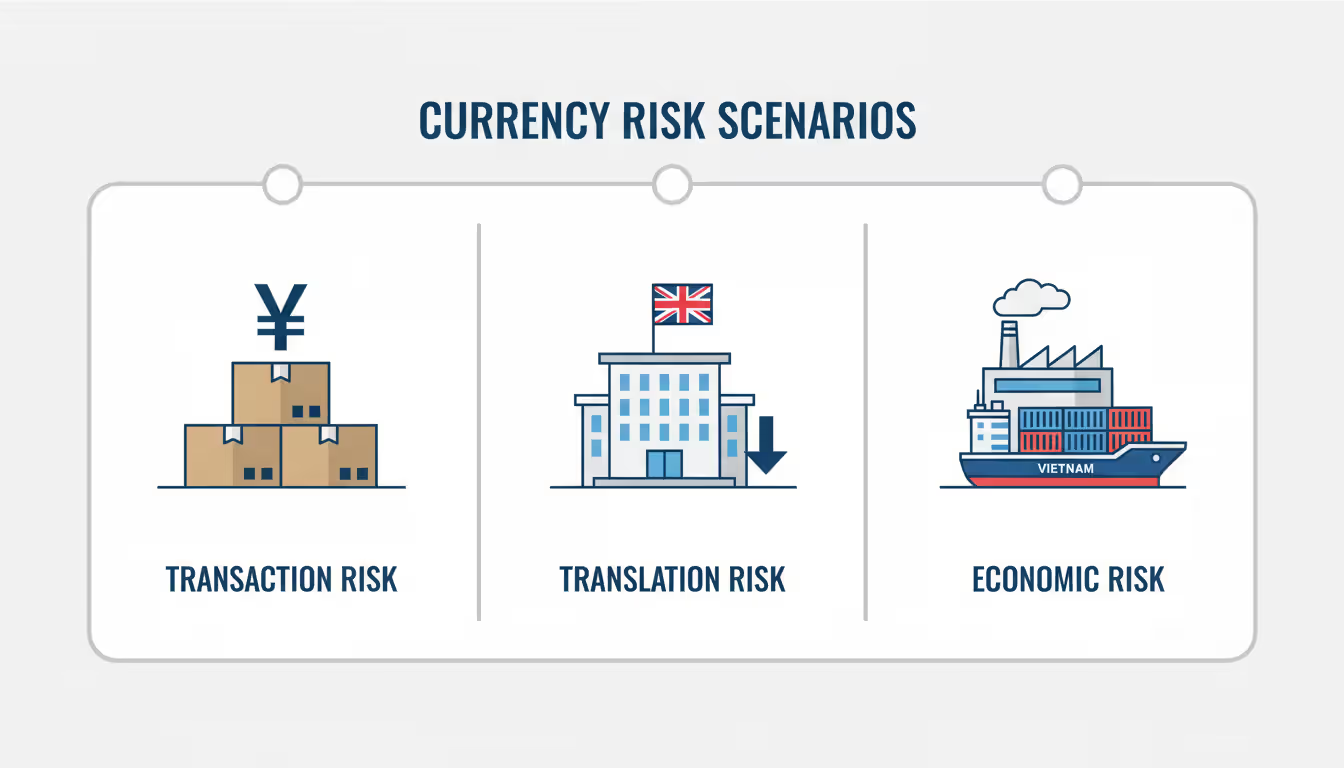

Transaction exposure — the immediate, concrete risk. You've agreed to pay ¥10 million in 60 days for manufacturing equipment. Right now, at 148 yen per dollar, you're looking at $67,568. But what if the yen strengthens to 138 by payment day? Same equipment now costs $72,464. That's five grand evaporating because you waited.

Translation exposure — the accounting headache. Your UK subsidiary posts strong numbers: £2 million profit. Great news, until you consolidate financials. Sterling dropped 7% this quarter, so that £2 million converts to fewer dollars on your income statement. Wall Street sees declining earnings even though your British team crushed their targets.

Economic exposure — the sneaky one that compounds over time. You manufacture furniture in North Carolina. Vietnamese factories make comparable products. The dong weakens 12% over eighteen months. Suddenly Vietnamese imports flood the market at lower prices. You haven't touched a foreign currency, yet your pricing power just took a hit.

Remember March 2023? The banking crisis sent the dollar on a wild ride—up 3% one week, down 2% the next. Companies without hedges watched their Q1 forecasts become fiction. Treasury teams with systematic programs? They updated their board slides and moved on.

Author: Olivia Kensington;

Source: martinskikulis.com

Core Methods for Hedging Currency Exposure

Forward Contracts

Think of forwards as locking your rate today for tomorrow's transaction. You call your bank, specify the amount and date, done. No guessing what exchange rates will do.

Real example: You're importing Italian leather goods—€250,000 due in four months. Today's rate sits at 1.09. Lock it in with a forward. Four months pass, and the euro jumps to 1.14. You still pay at 1.09, saving yourself $11,013.

The catch? That works both ways. Euro drops to 1.04? You're stuck paying 1.09 while your competitor who didn't hedge gets the better rate.

Banks don't charge you upfront for forwards. But you'll need a credit facility, and walking away early means paying whatever the contract's worth at current market rates—could be a gain, could be a loss.

Currency Options

Options work like insurance policies. Pay your premium, get protection against bad moves, keep the good ones.

Say you're expecting £800,000 from UK customers over the next five months. Buy a put option at 1.27 (costs maybe $18,000). Sterling crashes to 1.21? Exercise your option, convert at 1.27, collect $1,016,000 instead of $968,000. That $48,000 gain minus the $18,000 premium nets you $30,000 in savings.

Sterling rises to 1.31 instead? Let the option expire worthless, convert at the better market rate, lose only your premium.

You're paying for flexibility. Sometimes that's worth it—especially when you're not 100% certain the transaction will happen or the timing might shift. Invoice gets delayed two months? Your option adjusts easier than a forward.

Currency Swaps

Swaps mean trading payment streams with another party. You've got dollar debt but earn euros; they've got euro debt but earn dollars. Trade positions.

This gets complex fast and typically makes sense only for multi-year commitments or ongoing financing arrangements. A US manufacturer with a three-year euro loan might swap into dollars with a European company needing dollar financing. Both get their preferred currency exposure and potentially better interest rates.

Most businesses don't touch swaps until they're managing substantial, long-term multi-currency operations.

Natural Hedging Strategies

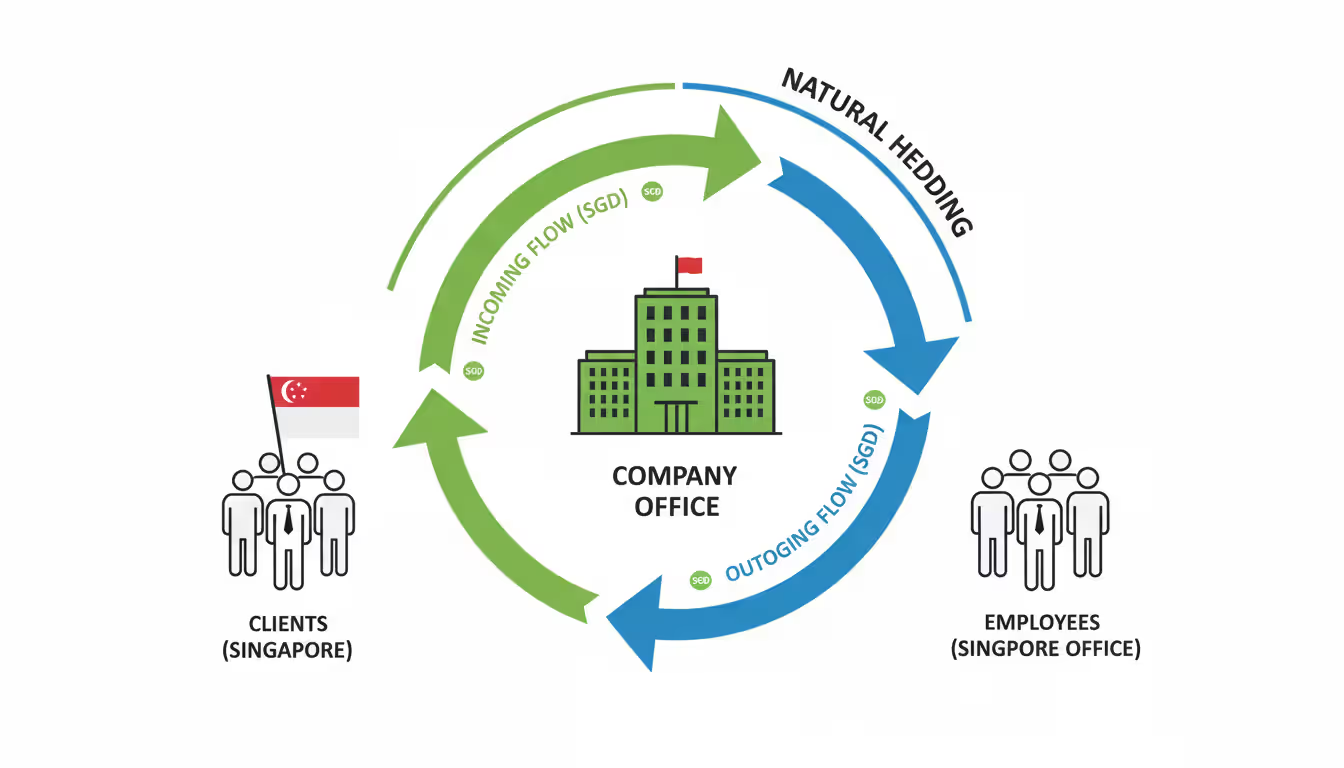

Match your inflows and outflows. Earn yen, spend yen. Problem solved—no derivatives needed.

A SaaS company sells software across Asia and invoices in Singapore dollars. They open a Singapore office and pay local salaries in Singapore dollars. Revenue and expenses move together. Exchange rates shift? Both sides adjust proportionally.

Or consider the importer bringing in Brazilian coffee. Instead of converting everything to dollars, they open US locations serving Brazilian communities and accept payment in reais from customers who prefer it. Creates a natural offset.

Zero derivative costs, no bank fees, nothing to renew or roll over. The downside: you need operational flexibility. Can't always choose where to locate facilities or which suppliers to use based purely on currency matching. A California tech company can't suddenly move engineering to Japan just to hedge yen exposure.

Author: Olivia Kensington;

Source: martinskikulis.com

Natural Hedge in Business vs Financial Hedging Instruments

Operational moves versus financial contracts—different tools for different jobs.

Natural hedges rebuild your business structure to eliminate currency mismatches inherently:

Bill your French customers in euros, pay your French suppliers in euros

Manufacture products in the regions where you sell them

Take loans in the same currency generating your revenue

Source components from suppliers in your sales markets

You're fundamentally changing how money flows through your business. A clothing retailer imports from Vietnam (paying dong), then opens stores in Ho Chi Minh City (collecting dong). The business model creates the hedge automatically.

What you gain: permanent protection that costs nothing in premiums, zero counterparty risk, no expiration dates. What you lose: agility. Relocating production takes years. Switching suppliers disrupts operations. You're committing to structural changes that can't pivot quickly.

Financial instruments—your forwards, options, swaps—transfer risk through contracts. Fast to execute (one phone call), precisely sized to exact exposures, no business restructuring required. Need to hedge a €500,000 payment next quarter? Done in ten minutes.

The economic versus financial hedge distinction matters strategically. Economic hedges tackle your fundamental competitive position and long-term structural exposure through business decisions. Financial hedges address specific transactions and short-term risks through banking products.

Smart treasury operations layer both approaches: natural hedges set a baseline for ongoing structural exposure, financial instruments handle residual risks and one-off transactions.

Hedging Method

What It Costs You

How Hard To Manage

Can You Change It?

When It Works Best

Protection Level

Forward Contracts

Nothing upfront; miss out if rates improve

Simple—set and forget

Locked in tight

Definite payment dates and fixed amounts

Complete coverage for that specific transaction

Currency Options

Premium payment (usually 1-3% of amount)

Moderate learning curve

Highly adaptable

Unsure timing or want upside participation

Shields downside, captures upside

Currency Swaps

Spread costs plus ongoing payments

Complicated setup and tracking

Difficult once committed

Multi-year financing needs

Extended structural coverage

Natural Hedge

Higher operating expenses sometimes

Complex to implement initially

Nearly impossible short-term

Continuous business operations

Automatic offset for matching flows

Hedging Strategies for Importers and Exporters

Trade creates directional exposure. You're either worried about foreign currency getting stronger (importers) or weaker (exporters).

Currency Hedging for Importers

Importing means you're buying foreign currency to pay suppliers. Your nightmare scenario: that currency strengthens, making your costs spike.

A Texas electronics distributor imports €150,000 in components monthly from Germany. Set up rolling forwards—each month, book a new 12-month forward contract. Creates a layered hedge where you're constantly protected for the year ahead, spreading your locked-in rates over time instead of betting everything on one day's exchange rate.

What about seasonal businesses? A retailer with variable import volumes might hedge 100% of baseline orders with forwards, then add call options for the variable seasonal portion. Guarantees protection on committed purchases, maintains flexibility for the uncertain piece.

Timing your payments strategically makes a difference too. Negotiate 90-day terms with suppliers when you expect the foreign currency to weaken (you'll pay less later). Push for 30-day terms when you expect strengthening (lock in current lower rates). Some importers simply demand dollar pricing—shifts all currency risk to the supplier, though they'll typically price that risk into your cost.

Currency Hedging for Exporters

Exporters collect foreign currency. Your problem: currency depreciation cuts your dollar revenue even when you sell the same volume.

An Oregon manufacturer exports agricultural equipment to Australia, invoicing A$500,000 quarterly. Sell those Aussie dollars forward at today's rate. When payments arrive in three months, you convert at your locked rate—doesn't matter if the AUD tanked in the meantime.

Put options offer a different play. Costs more than forwards but protects your downside while keeping upside potential. If you're in competitive markets where currency moves might create pricing opportunities, that flexibility helps. Australian dollar strengthens? You can cut local prices, gain market share, and still convert at favorable rates.

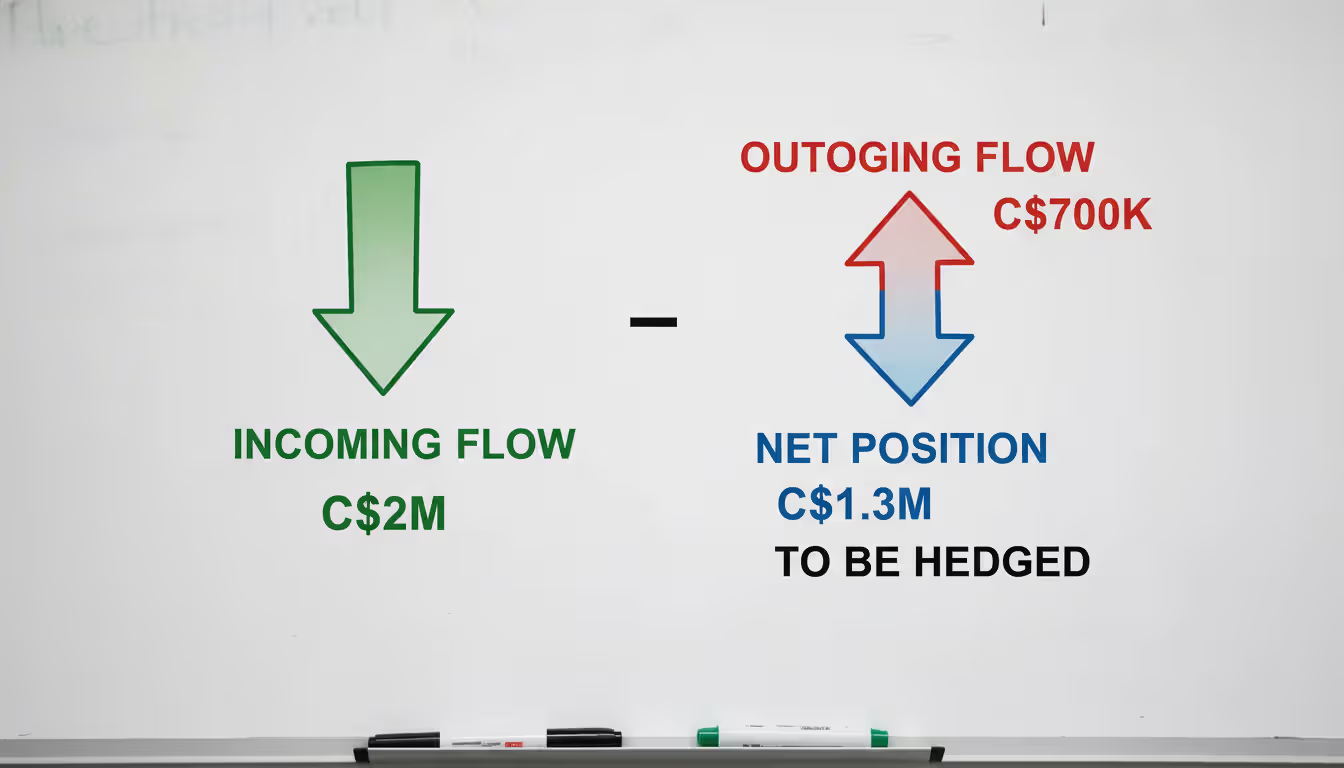

Netting across transactions cuts costs substantially. Your company receives C$2 million from Canadian sales but pays C$700,000 to Canadian suppliers. Don't hedge both gross amounts—hedge your net C$1.3 million exposure. Fewer transactions, lower fees, simpler tracking.

Author: Olivia Kensington;

Source: martinskikulis.com

Most sophisticated exporters hedge 60-75% of forecasted near-term revenue. Protects the core business, leaves some exposure for potential beneficial moves, acknowledges that forecasts aren't perfect. Better than the extremes: hedging nothing (wild volatility) or hedging 100% (expensive and creates new risks if volumes miss forecast).

Advanced Hedging Techniques and Considerations

Beyond basic forwards and options, you can fine-tune your approach.

Currency overlay programs separate FX management from core business decisions completely. Investment firms with international portfolios often hire specialized overlay managers who handle all currency exposure independently. Portfolio managers pick stocks; overlay managers handle the currency angles. Centralizes expertise, allows opportunistic positioning based on currency views—but adds management fees and another vendor relationship.

Your hedge ratio determines how much exposure you actually protect. Not everything needs hedging.

Calculate what's at stake: You've got £3 million in quarterly exposure. EUR/GBP historically moves about 4% per quarter (one standard deviation). At 95% confidence, you're looking at potential swings around $235,000. Can your business absorb that? If not, what loss threshold actually keeps you up at night?

Here's a practical formula: Decide your maximum acceptable loss, divide by your calculated exposure at risk, subtract from 100%. If you'll accept $100,000 in losses but calculated risk is $235,000, you need a 57% hedge ratio minimum.

Most companies settle somewhere between 70-85%. Balances protection with costs, maintains some natural market participation, avoids over-hedging traps.

Partial hedging acknowledges reality: forecasts are wrong. Always. Your sales projection says €1.8 million but actual results typically range €1.4-2.2 million. Hedge the €1.4 million floor with forwards (you're confident about that minimum). Leave the variable €400-800,000 portion either unhedged or protected with options. Avoids over-hedging scenarios where you've locked in more than you actually transact, accidentally creating speculative positions.

Run the numbers on costs versus benefits. Track what hedging actually delivers. Your program costs $40,000 annually in option premiums, bank spreads, and staff time. Compare against unhedged volatility. Hedging reduced quarterly earnings swings by $180,000 last year? Clear value. Costs ran $40,000 but you only avoided $25,000 in volatility? Time to reconsider your approach.

Don't forget tax treatment—hedge gains might get taxed differently than your underlying transaction results. Hedge accounting under ASC 815 lets you match hedge outcomes with hedged items for cleaner reporting, but documentation requirements and effectiveness testing create overhead. Plenty of mid-sized companies skip formal hedge accounting, accepting some P&L noise from mark-to-market revaluation.

Author: Olivia Kensington;

Source: martinskikulis.com

Common Mistakes When Hedging Currency Risk

Smart companies still trip over these regularly.

Over-hedging transforms risk management into speculation. You forecast €2.5 million in revenue, hedge the full amount, then only realize €2 million. That €500,000 excess hedge? That's a naked short position in euros. Euro strengthens, you lose money on phantom exposure you don't actually have. Always hedge conservatively against forecasts. Build flexibility through options or partial hedges when amounts aren't certain.

Chasing the "free" hedge backfires. Forwards look free compared to options with their upfront premiums. But opportunity cost is real cost. When rates move favorably and you're stuck in a forward, you're paying—just differently than a premium. Evaluate total economic impact, not just cash outlays. Sometimes the "expensive" option is actually cheaper when you account for flexibility value.

Market timing turns treasury into a trading desk. Waiting to hedge because you think rates will improve? That's speculation. Your job is predictability, not predicting exchange rates. Establish systematic hedging programs that execute according to policy regardless of market views. Discipline beats market opinions consistently.

Set-it-and-forget-it hedge ratios fail as businesses evolve. That 75% ratio made sense three years ago when your exposure profile, risk tolerance, and balance sheet looked different. Quarterly exposure just doubled because you entered new markets? Your old ratio doesn't fit anymore. Review policies annually minimum, recalculate actual exposure quarterly.

Misreading what actually creates risk leads to hedging the wrong thing. A medical device manufacturer hedges raw material costs in euros. Sounds smart—except all their competitors buy the same European materials facing identical euro exposure. When the euro moves, industry-wide pricing adjusts. The transaction exposure is real, but economic exposure is minimal because competitive dynamics offset it. Understanding your specific risk profile prevents hedging theater that protects nothing meaningful.

The biggest mistake I see companies make is treating currency hedging as a profit center rather than risk management. Your job isn't to predict exchange rates—it's to make your business results predictable despite exchange rates. The moment you start deviating from policy based on market views, you've become a currency speculator with a manufacturing business attached

— Jennifer Martinez

FAQ

What is the simplest way to hedge currency risk?

Forward contracts offer the straightest path. Call your bank, tell them the currency amount and payment date, lock the rate. Nothing fancy, no premium due, no complex decisions. For regular foreign payments or receipts, set up rolling forwards—book a new forward each month for transactions 3-12 months out. Creates systematic protection without constant decisions. A monthly €50,000 import becomes twelve individual forwards at different rates, averaging out your hedge cost over time.

How much does it cost to hedge currency exposure?

Forwards carry no upfront premium but you sacrifice favorable moves—that's your opportunity cost. Options typically run 1-3% of the notional amount for 3-6 month coverage, varying by currency pair volatility and how far from current rates you set your strike price. Banks add 0.1-0.5% spreads to market rates. For $1 million exposure, budget $10,000-30,000 in option premiums or $1,000-5,000 in forward transaction costs, plus internal staff time to manage everything.

Should small businesses hedge currency risk?

Hedge when currency moves could genuinely threaten your financial stability—rule of thumb says when foreign currency transactions hit 10-15% of revenue or a single adverse move could wipe out a quarter's profit margin. Small importer operating on 8% margins with big European purchases? Absolutely hedge. Service business with occasional minor foreign invoices? Probably accept the risk and focus elsewhere. Start simple with forwards for your largest confirmed transactions, expand into systematic programs as exposure grows and you build expertise.

What is a currency hedge ratio and how do I calculate it?

Your hedge ratio shows what percentage of exposure you're actually protecting. Math is simple: hedged amount divided by total exposure. Hedging €600,000 of €1 million exposure gives you a 60% ratio. Determining the right ratio takes more thought: assess currency volatility (wilder swings suggest higher ratios), forecast confidence (hedge less when amounts are uncertain), hedging costs you're willing to pay, and earnings volatility you can stomach. Most companies land between 60-80%, balancing protection against flexibility and cost. Adjust quarterly as your business changes.

Can I hedge currency risk without derivatives?

Absolutely—through natural hedging. Match currency inflows and outflows operationally. Invoice customers in the same currency you pay suppliers. Locate operations in the markets where you sell. Borrow in currencies matching your revenue streams. A US company with European revenue might open European bank accounts, pay European suppliers from European customer receipts, only repatriate net amounts periodically—organically offsetting most exposure. Requires operational flexibility but sidesteps derivative costs, counterparty risk, and accounting complexity entirely.

What's the difference between a forward contract and an option for hedging?

Forwards obligate both parties to exchange currencies at your agreed rate on the specified date—you're committed regardless of where markets move. Options grant you the right to exchange at your strike price without the obligation—walk away if market rates are better. Forwards demand nothing upfront but eliminate both risk and opportunity. Options require premium payments but protect against bad moves while preserving good ones. Use forwards when you want cost-efficient certainty for definite transactions. Use options when you value flexibility, face uncertain timing, or want to capture potential upside.

Managing currency risk isn't about predicting where exchange rates will go. Nobody consistently gets that right anyway. It's about making your business results predictable regardless of what currencies do.

Start by mapping your actual exposure—transaction, translation, and economic. Many companies discover their real risk differs substantially from initial assumptions once they systematically track currency flows. Then match hedging tools to your specific situation: forwards handle predictable transactions, options address uncertain timing or variable amounts, natural hedges tackle structural exposure.

Build systematic programs instead of making ad-hoc judgment calls. Define your hedge ratio, establish rolling hedge schedules, execute according to policy regardless of currency market chatter. Review quarterly as volumes change, but resist constant tinkering based on exchange rate forecasts—that's speculation dressed up as risk management.

The best currency hedging programs are boring. They run automatically, generate consistent results, free management to focus on actual business operations instead of forex volatility. If your treasury team spends more time debating currency views than execution mechanics, you've drifted from managing risk into taking it.

Companies just starting out should hedge their largest near-term exposures using straightforward forwards. Build experience and confidence, then layer in options for variable amounts, implement netting across offsetting positions, consider natural hedges for long-term structural exposure. The learning curve flattens quickly when you start focused and expand deliberately based on what your specific business actually needs.

Swap rates represent the interest cost or credit applied when forex traders hold positions past the daily rollover time. Understanding how these overnight fees work, when you pay or earn them, and their cumulative impact is essential for swing traders and anyone implementing carry trade strategies in 2026

Spread betting lets you speculate on market moves without owning the asset. This guide walks through real examples—long and short positions, forex pairs, margin calculations—showing exactly how profits and losses accumulate, how to size stakes responsibly, and what happens when trades go wrong

An overnight index swap is a derivative where parties exchange fixed and floating interest payments based on compounded overnight rates. These instruments have become the standard for derivatives discounting and provide key insights into central bank policy expectations and market stress levels

Interest rate movements can transform profitable loans into financial burdens overnight. Companies with floating-rate debt and bond investors face the same challenge: protecting against adverse rate shifts without sacrificing upside. This guide explains hedging instruments, duration strategies, and how to match protection to your specific exposure

The content on this website is provided for general informational and educational purposes only. It is intended to explain concepts related to Forex (FX) trading, currency markets, leverage, hedging, and risk management.

All information on this website, including articles, guides, and examples, is presented for general educational purposes. Forex trading carries significant risk, and outcomes may vary depending on market conditions, leverage, and individual decisions.

This website does not provide financial, investment, or trading advice, and the information presented should not be used as a substitute for consultation with qualified financial professionals.

The website and its authors are not responsible for any errors or omissions, or for any outcomes resulting from decisions made based on the information provided on this website.