Here's what catches most traders off guard: you open a EUR/USD position on Monday morning, hold it through Tuesday night, and discover a $6.50 charge labeled "swap" in your account history. No one closed your trade. The price barely moved overnight. Yet your broker extracted a fee you didn't see coming.

That's a swap rate—the daily interest adjustment applied to positions kept open beyond the market's 5 PM Eastern rollover cutoff. Central banks assign interest rates to their currencies. Trading a pair means you're simultaneously going long one currency (earning its rate) and short another (paying its rate). The gap between these rates creates your swap charge or credit.

A single night's fee looks insignificant. Three dollars here, five dollars there—pocket change on a standard lot position. But swing traders holding for two weeks? That pocket change becomes $70 in accumulated costs, sometimes more than the spread you paid entering the trade. On the flip side, choose the right currency pair and direction, and those daily credits stack up as passive income while you sleep.

Brokers pull these rates from the interbank tom-next market, layer on their markup (usually 1-2% annually), and apply the result automatically at rollover. Since you're trading on leverage, the calculation uses your full position size. Control $100,000 in EUR/USD with just $5,000 margin, and swap gets computed on that entire $100,000—not your margin deposit. This amplifies both costs and credits depending on which side of the interest rate differential you've positioned yourself.

How Currency Swap Rates Work

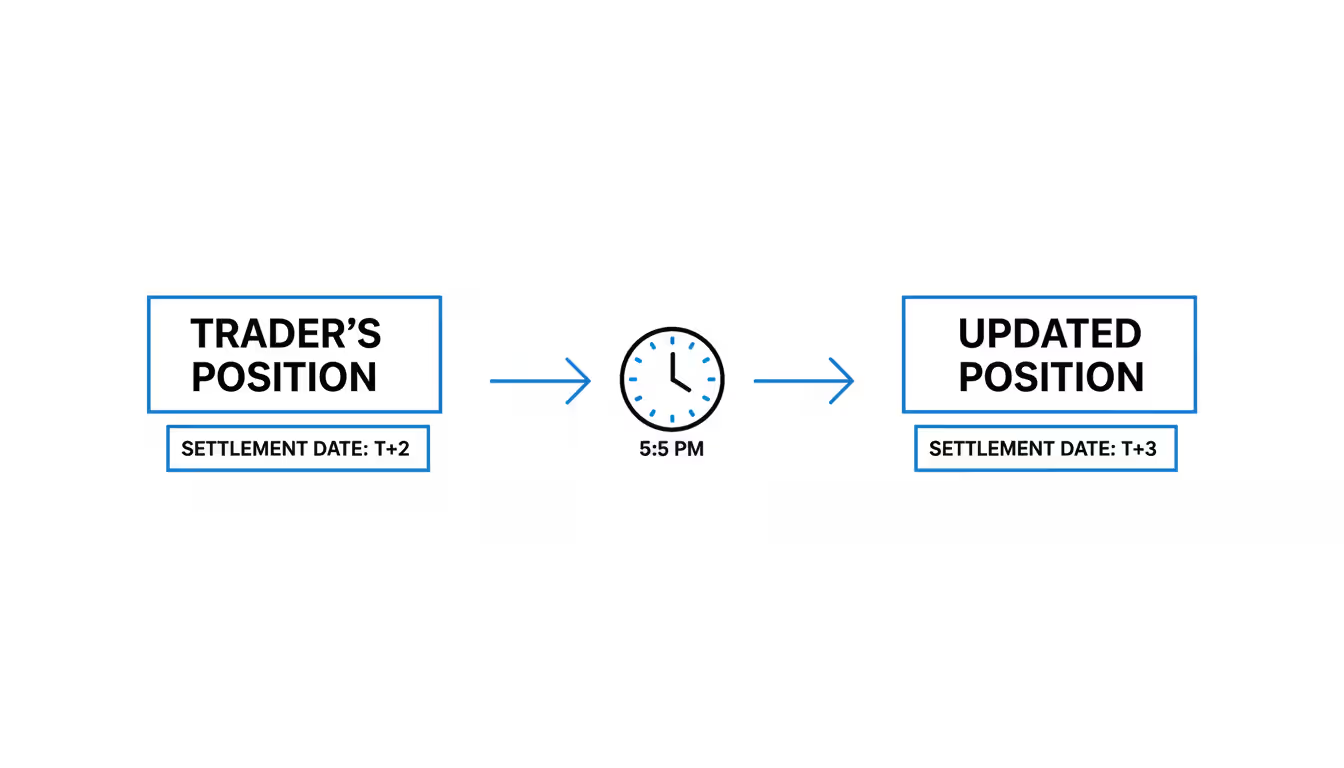

Opening a forex position creates a spot contract that settles two business days forward. Your broker needs to "roll" this contract ahead by one day when you keep the position overnight—closing the original settlement date and opening a new one. This happens invisibly at the 5 PM ET cutoff. Your actual trade stays open. Your entry price doesn't change. But behind the curtain, the broker has swapped out tomorrow's value date for the day after.

The mechanics stay hidden from most retail traders. You won't see two transactions (one close, one open) in your platform. Instead, a single "swap" line appears in your account history, showing either a debit or credit in your account currency. The broker calculates this in the quote currency of your pair first, then converts it using the current exchange rate if you're trading a USD account with EUR/JPY, for instance.

Author: Vanessa Cole;

Source: martinskikulis.com

Rollover rate forex markets operate on interbank lending rates—specifically, the cost for banks to borrow currency overnight from each other. Say you're long GBP/USD. You've borrowed dollars (paying the Fed's rate) to purchase pounds (earning the Bank of England's rate). If the BoE sits at 4.25% while the Fed charges 4.75%, you're bleeding a 0.50% annual rate in the wrong direction. That's a negative swap.

Flip to short GBP/USD, and you'd expect a positive swap from that same differential, right? Not quite. Brokers add markup to both sides—often making both directions negative for the same pair. You might see -$4.80 on longs and -$2.50 on shorts for GBP/USD. That markup (typically 0.5-2% annually) represents part of how brokers monetize your trading activity beyond spreads. A 1.5% differential between currencies might translate to -$7 one direction and -$2 the other after the broker's cut, rather than a clean +$5/-$5 split.

Understanding Overnight Swap Rate Meaning and Tom-Next

Overnight swap doesn't mean holding a position for 24 hours. It means crossing that 5 PM Eastern threshold. Open a trade at 4:58 PM and close at 5:02 PM? You're paying or earning swap for those four minutes. Open at 5:01 PM and close at 4:59 PM the next afternoon? Zero swap, despite nearly 24 hours of exposure.

Tom-next—short for "tomorrow-next"—describes the actual transaction banks use to manage this rollover. They're borrowing money for tomorrow's value date and repaying it the next business day. Institutional traders and banks conduct thousands of these transactions daily to maintain currency positions without taking physical delivery. Your retail broker aggregates these institutional rates, applies adjustments for their costs and profit margins, then passes the final number to your account.

Wednesday night creates a strange quirk. Positions held through that rollover get charged or credited three times the normal amount. Why? The spot forex market operates on a T+2 settlement cycle. Wednesday's value date lands on Friday. Rolling it forward needs to account for Saturday and Sunday when banks are closed, jumping straight to Monday. That's three days of interest in one rollover event. Some brokers apply this "triple swap" on Friday instead, depending on their liquidity providers' conventions, though Wednesday dominates industry practice.

This timing knowledge prevents nasty surprises. Plan to hold a position for five calendar days including a Wednesday? You're actually paying seven days of swap. Conversely, if you're targeting positive swap income, deliberately holding through Wednesday triples that night's credit. A position earning $7 normally collects $21 on Wednesday night—meaningful money for carry traders operating multiple standard lots.

Interest Rate Differential and How Swap Rates Are Calculated

The formula for calculating swap starts with the rate gap between your two currencies:

Let's run real numbers using 2026 rates. You're long one standard lot (100,000 units) of AUD/USD at 0.6500. The Reserve Bank of Australia maintains 4.35% while the Federal Reserve sits at 4.75%. That's a -0.40% differential working against you—you're borrowing at the higher rate. Your broker tacks on a 1.5% markup.

Swap = (100,000 × (-0.0040 - 0.015) × 0.6500) / 365 = -$3.38 per night

Short that same position, and the math reverses—but the broker still takes their cut. Instead of earning from the differential, you'll pay roughly -$1.15 nightly. The broker's 1.5% slice eats into what would otherwise be a positive swap for shorts.

Central bank policy shifts drive swap changes in real time. The Federal Reserve's 2022-2023 rate hike campaign dramatically increased costs for traders long non-USD pairs. Today's environment (2026) shows more stability, with major central banks clustering between 3.5% and 5%, yet the differentials still matter plenty for multi-week positions. The Bank of Japan's persistent 0.25% rate creates enormous gaps with virtually every other major currency, making yen pairs swap-intensive in both directions.

Brokers recalibrate these rates continuously—some daily, others weekly—tracking interbank rate movements and their own funding costs. When the Bank of England announces a surprise rate decision, your GBP/USD swap might shift overnight. Always check current rates before committing to a swing trade. Last month's +$3 credit could have flipped to a -$2 charge after a central bank meeting you didn't follow.

Author: Vanessa Cole;

Source: martinskikulis.com

Positive vs Negative Swap in Forex Positions

Whether you see credits or debits each night comes down to two factors: which currency pays more interest, and which direction you're trading. Positive swap grows your account balance—you're collecting interest on the trade. Negative swap shrinks it—you're paying rent to keep the position open.

Take USD/JPY with the Fed at 4.75% and the Bank of Japan at 0.25%. Go long USD/JPY (buying dollars, selling yen), and you're holding the high-rate currency against the low-rate one. After broker markup, you might collect $6-8 nightly on a standard lot. Short USD/JPY reverses this dynamic: you're borrowing expensive dollars to hold cheap yen, creating a negative swap around -$10 to -$12 per night.

Different pairs produce wildly different swap magnitudes. EUR/GBP shows tiny swaps because the European Central Bank (3.75%) and Bank of England (4.25%) run similar policies—only a 0.50% gap. Daily swaps might be just $1-2 per standard lot either direction. Compare that to USD/TRY, where the Fed's 4.75% meets Turkey's 45% central bank rate. The differential is massive, creating swaps that can hit $50-100 daily on a standard lot. Of course, the Turkish lira's volatility and chronic depreciation often overwhelm any interest collected.

High-yielding currencies—Aussie dollar, Kiwi, Mexican peso—generate positive swaps when purchased against low-yielding ones like the yen or Swiss franc. This attracts carry traders, though higher yields typically signal higher economic risk. The Turkish lira offers eye-watering positive swap for longs against the dollar, yet the currency has lost 80%+ of its value over the past decade. Swap income means nothing if the exchange rate collapses underneath you.

Broker markup ensures both directions for the same pair rarely show positive swaps on retail platforms. You'll commonly see asymmetric negative swaps: -$5 for longs, -$2 for shorts. Or +$3 for longs, -$8 for shorts. Don't assume that a negative long swap automatically means a positive short swap. Check your broker's contract specifications for both directions before structuring your trade.

Swap Costs for Holding Positions Over Time

Daily swap charges compound faster than new traders realize. A $5 nightly fee on a standard lot becomes $150 monthly—enough to convert a breakeven technical trade into a net loss. Swing traders holding for three weeks on that same position pay $105 in financing, which might exceed the spread cost you paid entering the trade. That's pure overhead that never shows up in your initial risk calculation unless you plan for it.

Wednesday's triple swap accelerates this accumulation. Hold a position for two weeks, and you'll cross two Wednesday rollovers—incurring 16 days of swap charges (10 single-day rollovers plus two triple-charge events). At $7 per night in negative swap, that's $112 in financing over 14 calendar days. On a $5,000 margin deposit controlling $100,000 notional value, you've just paid 2.24% of your margin—comparable to the bid-ask spread on many pairs.

Author: Vanessa Cole;

Source: martinskikulis.com

Finding current swap rates requires digging into your platform's contract specifications. Most trading software displays this under "symbols," "instruments," or "contract details," showing separate values for long and short positions. These appear either as points (pips) or in your account currency per lot. Seeing "-0.65 points" on EUR/USD with a standard lot? That's -$6.50 nightly, since each point on EUR/USD equals $10 per standard lot (or $1 per mini lot, $0.10 per micro lot).

Managing these costs as a swing trader demands several tactics. First, compare swap rates across brokers before depositing funds. One broker might charge $7 nightly on long EUR/USD while another charges $4—that $3 difference costs $90 per month on a continuously held position. Second, factor swap direction into your pair selection. If your strategy works equally well on AUD/JPY (positive swap long) or EUR/USD (negative swap long), choosing the former adds income while the latter drains your account. Third, incorporate swap into position sizing. Targeting 200 pips over ten days? If swap will cost you 15 pips, your effective target drops to 185 pips—adjust your risk/reward calculations accordingly.

Short-term traders sometimes dismiss swap as irrelevant for "just a few days." Three nights at $5 each is $15—enough to turn a 10-pip winner into a 5-pip winner on a standard lot after you account for the spread. Track your monthly swap costs across all positions, and you'll probably discover you're paying hundreds of dollars in financing charges you never consciously budgeted for.

Swap Rates and Carry Trade Strategies

Carry trades explicitly target positive swap as a profit center, not just a byproduct of position holding. The classic setup: buy a high-rate currency against a low-rate currency, then hold the position to collect daily credits. Earning $8 nightly on a standard lot generates $240 monthly or $2,880 annually—that's a 2.88% return on $100,000 notional value.

Leverage transforms these modest percentages into dramatic returns on margin. A $5,000 margin deposit controlling $100,000 (20:1 leverage) collects that same $2,880 annually in swap income. Express it as a percentage of margin used, and you're looking at a 57.6% annual return before any price appreciation. This explains the carry trade mania of the 2000s, when Japanese rates sat near zero while Australian and New Zealand rates exceeded 6-7%. Traders pocketed substantial interest income, often supplemented by currency appreciation as capital flowed into the high-yielders.

The 2026 market offers smaller but still attractive carry opportunities. USD/JPY remains the primary vehicle with the Fed at 4.75% versus the Bank of Japan's 0.25%. AUD/JPY and NZD/JPY push differentials even higher—the Reserve Bank of New Zealand maintains 5.50%, creating a 5.25% gap with Japanese rates. These pairs can generate $10-15 nightly per standard lot after broker markup, adding up to meaningful income for patient traders with stable positions.

But here's the catch nobody mentions until after it explodes: carry trades work beautifully in calm markets and implode during panic. When global risk appetite collapses, investors dump high-yielding currencies and stampede into safe havens—yen, Swiss franc, and US dollar. The Japanese yen can appreciate 5-10% in a week during severe risk-off events, obliterating months of accumulated swap income. The 2008 financial crisis saw carry trades unwind violently. August 2024's yen carry trade meltdown repeated the pattern. Traders who focused solely on collecting swap while ignoring price risk suffered catastrophic losses.

Popular carry pairs in 2026 include USD/JPY, AUD/JPY, NZD/JPY, USD/CHF, and (for aggressive risk-takers) EUR/TRY. Mexican peso pairs attract carry interest too, though political uncertainty and cartel violence create periodic volatility spikes. Successful carry traders combine positive swap with directional or range-trading analysis—using swap income as a bonus, not the entire justification for the position. They size conservatively, recognizing that leverage amplifies both swap credits and price losses when the market reverses.

How to Minimize or Avoid Rollover Rate Fees

Swap rates silently destroy profitability for swing traders who don't track them.I've audited thousands of retail trading accounts, and here's the pattern: traders obsess over entry prices and exit prices while completely ignoring the financing costs piling up between those two points. Someone celebrates catching a 150-pip EUR/USD move over three weeks without realizing they surrendered 40 pips to swap—money that never registered in their mental accounting of the trade. Professional traders treat swap as a standard business expense line item, exactly like spreads and commissions. Carry traders flip it and treat swap as a revenue line. Either way, it belongs in your pre-trade analysis spreadsheet, not as a shock when you review your monthly account statement

— Michael Chen

Islamic or swap-free accounts eliminate overnight charges entirely, complying with Sharia prohibitions on interest. Brokers offering these accounts strip out swap but typically compensate elsewhere—wider spreads, higher commissions, or administrative fees on positions held beyond a threshold (often 3-7 days). These accounts target Muslim traders but are frequently available to anyone, though some brokers verify religious observance or restrict access to certain account types.

The cost-benefit equation varies dramatically by broker. Some charge zero additional fees for the first three days, making swap-free accounts objectively superior for short-term swing traders regardless of religious considerations. Others impose a fixed daily fee (say, $5 per lot) starting from day one or after a grace period—potentially costing more than standard swap rates. Always compare the broker's swap-free fee structure against their normal swap rates for your typical holding periods and pairs before switching account types.

Day trading completely sidesteps the swap question. Close everything before 5 PM Eastern, and you'll never pay or earn a cent in rollover fees. This works perfectly for traders whose systems generate signals on 5-minute to 4-hour charts without requiring overnight exposure. The downside? You're forced to exit potentially profitable positions to avoid swap costs, and you miss any overnight moves that might work in your favor.

Shopping for low-swap brokers means comparing contract specifications across multiple platforms. The same EUR/USD position might cost $7 nightly at Broker A and $4 at Broker B. Over a month of continuous holding, that $3 daily difference accumulates to $90—real money that impacts your bottom line. Pull up contract specs for your most-traded pairs at three or four brokers, calculate monthly swap costs based on your typical position sizes and hold times, then factor this into your broker selection alongside spreads, execution quality, and regulation.

Total cost comparison matters more than any single fee component. A scalper executing 50 trades daily cares intensely about spreads and commissions—swap is utterly irrelevant since nothing's held overnight. A swing trader placing five trades monthly, each held two weeks, pays substantial cumulative swap that might exceed spread costs. For that trader, a broker with 0.2 pips wider spreads but 30% lower swap rates could prove cheaper overall.

Some traders attempt to offset negative swap positions with positive swap hedges—for example, holding long EUR/USD (negative swap) for a technical setup while adding a small long AUD/JPY (positive swap) position. This only makes sense if the second position aligns with your broader strategy and risk management. Forcing trades purely to offset swap costs usually creates more problems (correlation risk, doubled margin usage, management complexity) than it solves.

Author: Vanessa Cole;

Source: martinskikulis.com

Currency Pair Swap Rate Comparison

This table shows typical overnight swap rates for major pairs in 2026. Values represent one standard lot (100,000 units) and are approximate—actual rates fluctuate with central bank policy changes and vary by broker.

Currency Pair

Long Swap (USD)

Short Swap (USD)

Interest Rate Gap

EUR/USD

-$5.50

-$2.00

-0.75% (ECB 3.75%, Fed 4.75%)

GBP/USD

-$4.80

-$2.50

-0.50% (BoE 4.25%, Fed 4.75%)

USD/JPY

+$6.20

-$10.50

+4.50% (Fed 4.75%, BoJ 0.25%)

AUD/USD

-$3.00

-$1.50

-0.40% (RBA 4.35%, Fed 4.75%)

USD/CHF

+$4.50

-$8.00

+3.75% (Fed 4.75%, SNB 1.00%)

NZD/USD

+$1.00

-$5.50

+0.75% (RBNZ 5.50%, Fed 4.75%)

USD/CAD

+$2.80

-$6.20

+1.25% (Fed 4.75%, BoC 3.50%)

EUR/GBP

-$1.20

-$0.80

-0.50% (ECB 3.75%, BoE 4.25%)

Notice how yen and Swiss franc pairs offer the strongest positive swap potential when you're long the higher-yielding currency. Meanwhile, buying euros, pounds, or Aussie dollars against the US dollar costs you money nightly due to the Fed's relatively higher rate in this 2026 environment.

Frequently Asked Questions

What is a swap rate in simple terms?

Swap rates are the nightly interest adjustments your broker applies when you keep a forex position open past the 5 PM Eastern rollover cutoff. Since currency trading involves simultaneously borrowing one currency to purchase another, and since central banks assign different interest rates to each currency, there's a cost or benefit to holding that position overnight. Your broker calculates this gap between the two currencies' rates, adds their markup, then either charges your account or credits it depending on which direction you're trading.

Do all forex brokers charge swap rates?

Almost every standard forex broker applies swap rates derived from the interest rate gaps between currency pairs. The exception is Islamic accounts (also called swap-free accounts), which eliminate these charges to comply with Sharia financial principles. Brokers offering Islamic accounts usually compensate for lost swap revenue through alternative means—wider bid-ask spreads, elevated commission rates, or administrative fees kicking in after you hold a position for a certain number of days. The exact compensation method varies widely across brokers.

Can you earn money from swap rates?

Absolutely—through carry trade strategies. Buy a currency with a higher interest rate against one with a lower rate, and you'll receive a daily credit. For instance, long USD/JPY with the Fed at 4.75% and the Bank of Japan at 0.25% generates positive swap, potentially $5-10 nightly per standard lot depending on your broker. Over months, this compounds into substantial income. The critical caveat: currency price swings can easily overwhelm swap income if the exchange rate moves against your position, so carry traders need solid risk management and trend analysis to avoid catastrophic losses during market reversals.

How often are swap rates charged?

Once per day, specifically when you hold a position past the daily rollover threshold (5 PM Eastern Time for most brokers). The charge doesn't depend on how many hours you've held the position during the day—only whether you crossed that cutoff. Wednesday night is special: positions held through Wednesday's rollover incur triple the normal swap amount to account for the weekend when banks are closed but interest continues accruing. This means three days of interest hit your account in a single rollover event, making Wednesday either the most expensive or most profitable night of the week depending on your swap direction.

Are swap rates the same for all currency pairs?

Not even close. Swap rates vary dramatically based on each currency pair's interest rate differential. Pairs involving the Japanese yen (0.25% rate) or Swiss franc (1.00% rate) show large swaps because these currencies pay minimal interest compared to others. Pairs like EUR/GBP have tiny swaps since the ECB (3.75%) and BoE (4.25%) maintain similar policies—only a 0.50% gap. Exotic pairs with emerging market currencies like the Turkish lira (45% rate) or Mexican peso show the largest swaps, though these pairs also carry dramatically higher volatility and different risk profiles than major pairs.

What is a swap-free account and who can use it?

Swap-free accounts are trading accounts that don't apply overnight interest charges or credits, originally designed for Muslim traders following Sharia law's prohibition on interest-based transactions. While marketed primarily to Islamic traders, many brokers now allow anyone to request these accounts. Brokers don't provide this for free—they recover the foregone swap revenue through higher spreads, increased commissions, or administrative fees applied to positions held beyond a set number of days (commonly 3-7 days). Whether this arrangement saves you money depends entirely on your trading style, typical holding periods, and the specific broker's fee structure for swap-free accounts.

Swap rates directly impact your bottom line if you hold forex positions overnight—period. These daily adjustments flow from interest rate gaps between currencies, automatically applied when brokers roll your position to the next value date. A single night's charge might look trivial, but weeks of accumulated swaps can seriously damage profitability through negative financing costs or boost returns through positive carry income.

Knowing how swaps function lets you make smarter decisions about trade management and strategy design. Day traders can ignore the entire topic by flattening positions before the 5 PM ET cutoff. Swing traders must build these costs into profit targets and risk calculations from day one. Carry traders can construct strategies specifically around capturing positive swap, though they'd better respect the price risk that comes with chasing interest rate differentials.

The practical approach: treat swap as a routine business expense or income stream, not an afterthought. Check rates before entering multi-day positions. Compare swap structures across brokers when selecting your trading platform. Remember Wednesday's triple charge when planning how long to hold a position. For traders regularly keeping positions overnight, choosing a broker with competitive swap rates can save several thousand dollars annually compared to one charging above-average financing fees.

Whether you're bleeding money on long EUR/USD positions or collecting credits on long USD/JPY trades, these daily adjustments affect your results just as much as spreads, commissions, and price movements do. Build them into your planning, track them in your performance analysis, and adjust your approach when swap costs threaten to undermine otherwise solid trading decisions.

Spread betting lets you speculate on market moves without owning the asset. This guide walks through real examples—long and short positions, forex pairs, margin calculations—showing exactly how profits and losses accumulate, how to size stakes responsibly, and what happens when trades go wrong

An overnight index swap is a derivative where parties exchange fixed and floating interest payments based on compounded overnight rates. These instruments have become the standard for derivatives discounting and provide key insights into central bank policy expectations and market stress levels

Interest rate movements can transform profitable loans into financial burdens overnight. Companies with floating-rate debt and bond investors face the same challenge: protecting against adverse rate shifts without sacrificing upside. This guide explains hedging instruments, duration strategies, and how to match protection to your specific exposure

Interest rate arbitrage exploits interest differentials between countries to generate profit. This comprehensive guide explains covered and uncovered strategies, carry trades, why covered arbitrage is considered risk-free, and the real-world constraints that limit arbitrage opportunities in modern currency markets

The content on this website is provided for general informational and educational purposes only. It is intended to explain concepts related to Forex (FX) trading, currency markets, leverage, hedging, and risk management.

All information on this website, including articles, guides, and examples, is presented for general educational purposes. Forex trading carries significant risk, and outcomes may vary depending on market conditions, leverage, and individual decisions.

This website does not provide financial, investment, or trading advice, and the information presented should not be used as a substitute for consultation with qualified financial professionals.

The website and its authors are not responsible for any errors or omissions, or for any outcomes resulting from decisions made based on the information provided on this website.