Panoramic view of a modern financial district skyline at sunrise with stylized transparent arrows representing international capital flows between bank buildings

Interest rate arbitrage represents a trading strategy that exploits differences in interest rates between two countries to generate profit. When central banks set different borrowing costs—say, the Federal Reserve maintains rates at 4.5% while the European Central Bank holds at 2.0%—sophisticated investors can borrow in the cheaper currency and invest in the higher-yielding one.

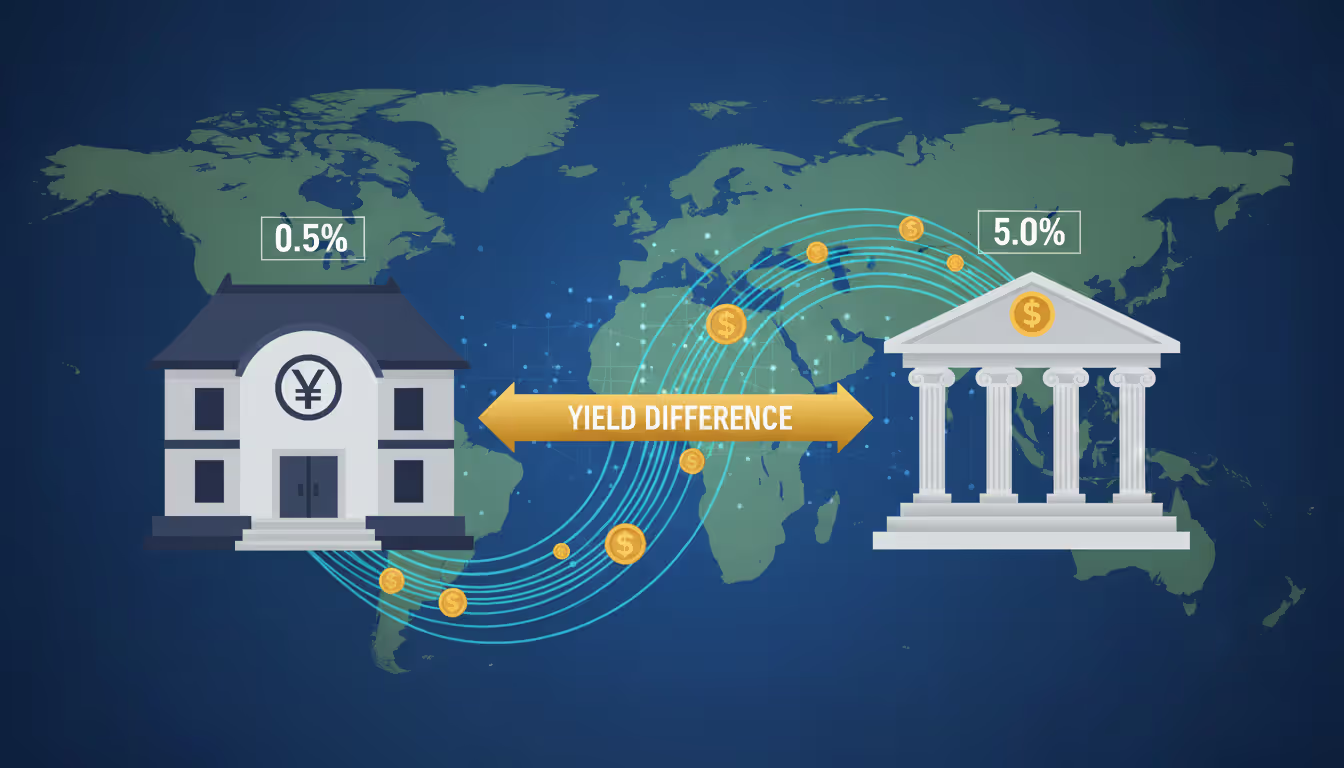

The basic mechanism works like this: A trader borrows funds in Japanese yen at 0.5% annual interest, converts those yen to U.S. dollars, and invests the proceeds in Treasury securities yielding 4.0%. The 3.5 percentage point differential creates the profit opportunity, assuming exchange rates remain stable or move favorably.

What is interest rate arbitrage in practical terms? It's a form of financial engineering that seeks to capture these interest differentials while managing—or in some cases accepting—currency risk. Banks, hedge funds, and institutional investors actively monitor global rate spreads, looking for dislocations large enough to justify the transaction costs and operational complexity.

The strategy relies on several market realities. First, central banks rarely coordinate their monetary policies perfectly. Economic conditions vary across regions, pushing some countries to raise rates while others cut. Second, capital can move across borders relatively freely in developed markets, allowing large-scale fund transfers. Third, forward currency markets exist to hedge exchange rate risk, making certain arbitrage strategies nearly risk-free in theory.

How interest differentials create arbitrage comes down to simple math. If you can lock in borrowing at 1% and lending at 4%, the 3% spread becomes your gross profit margin. The challenge lies in execution: converting currencies, managing counterparty risk, monitoring positions, and timing your entry and exit to maximize returns while minimizing exposure.

Market efficiency theory suggests these opportunities should vanish quickly as arbitrageurs pile in, driving up demand for high-yield currencies and pushing down yields. In practice, frictions keep small arbitrage windows open longer than pure theory predicts, though the margins have compressed significantly since the 1990s.

Covered vs Uncovered Interest Rate Arbitrage

The distinction between covered and uncovered approaches defines the risk profile of your arbitrage strategy. Both methods exploit interest rate differentials, but they handle currency risk in fundamentally different ways.

Covered Interest Parity Explained

Covered interest parity represents the theoretical condition where interest rate differentials equal the forward premium or discount between two currencies. When this relationship holds, no arbitrage profit exists because the forward contract exactly offsets the interest advantage.

Here's how covered interest arbitrage works in practice: You borrow $1 million at 2% annual interest in euros (after converting from dollars). Simultaneously, you invest that $1 million in U.S. Treasury bills yielding 4.5%. To eliminate currency risk, you enter a forward contract to sell dollars and buy euros at a predetermined rate in one year.

The forward rate typically reflects the interest differential. If the euro trades at $1.10 spot and U.S. rates exceed euro rates by 2.5%, the one-year forward rate should be approximately $1.1275. This forward premium compensates for the interest advantage, theoretically eliminating arbitrage profits.

Author: Vanessa Cole;

Source: martinskikulis.com

Yet deviations from covered interest parity do occur. During the 2020-2022 period, researchers documented persistent violations, particularly in cross-currency basis spreads. Banks faced higher balance sheet costs under Basel III regulations, making them less willing to facilitate arbitrage trades even when pricing dislocations appeared. By 2026, these deviations have narrowed but haven't disappeared entirely, especially during periods of market stress.

Currency arbitrage and interest rates connect through the forward points—the difference between spot and forward exchange rates. When forward points don't perfectly reflect interest differentials, arbitrage opportunities emerge. A trader might find that borrowing in Swiss francs at 0.75%, converting to dollars, investing at 4.25%, and hedging with a forward contract yields a net 0.30% annual return after all costs. Small, yes, but meaningful when scaled to $500 million.

Uncovered Interest Parity and Exchange Rate Risk

Uncovered interest parity assumes that expected exchange rate changes will offset interest differentials. Unlike covered arbitrage, this approach skips the forward contract hedge, leaving the trader exposed to currency fluctuations.

The uncovered strategy appeals to investors who believe the high-yield currency will appreciate—or at least not depreciate enough to erase the interest advantage. If Brazilian real deposits pay 10% while U.S. dollar deposits pay 4%, the 6% differential looks attractive. However, if the real depreciates 8% against the dollar over the holding period, you've suffered a net 2% loss despite the higher interest income.

Empirical evidence consistently shows uncovered interest parity fails in the real world. High-interest-rate currencies often appreciate rather than depreciate, a phenomenon known as the forward premium puzzle. This violation of theoretical expectations has generated substantial academic debate and represents one of the most robust anomalies in international finance.

Risk-tolerant investors sometimes favor uncovered strategies because forward contracts carry their own costs—bid-ask spreads, margin requirements, and counterparty risk. Skipping the hedge preserves more of the interest differential as potential profit. The trade-off: you're making a leveraged currency bet alongside your interest rate play.

How Carry Trade Arbitrage Works

The carry trade represents the most popular form of interest rate arbitrage among retail and institutional investors alike. This strategy involves borrowing in a low-interest-rate currency (the funding currency) and investing in a high-interest-rate currency (the target currency), capturing the interest differential as profit.

Carry trade arbitrage flourished during the 2003-2007 period when Japanese yen rates hovered near zero while Australian dollar and New Zealand dollar rates exceeded 6%. Traders borrowed yen cheaply, converted to Aussie or Kiwi dollars, and invested in government bonds or even high-yield savings accounts. As long as the exchange rate remained stable or moved in their favor, they pocketed the spread.

Author: Vanessa Cole;

Source: martinskikulis.com

The mechanics are straightforward but the execution requires discipline. Say you borrow ¥10 million at 0.25% annual interest when the exchange rate sits at ¥140 per dollar, giving you roughly $71,428. You invest this amount in U.S. Treasury notes yielding 4.0%. Your gross annual interest income is $2,857 while your interest expense is ¥25,000 (approximately $178 at current rates). The net carry is about $2,679 annually, or a 3.75% return on your dollar investment.

Carry trades work best in stable, low-volatility environments. When market turbulence strikes, funding currencies often appreciate sharply as traders unwind positions simultaneously. The yen famously surged during the 2008 financial crisis and again in early 2022 as risk appetite evaporated. Investors who borrowed yen at ¥120 per dollar suddenly faced repayment at ¥105, suffering devastating losses that overwhelmed years of accumulated interest income.

How interest differentials create arbitrage in carry trades depends on central bank policy divergence. When the Federal Reserve raises rates while the Bank of Japan maintains ultra-loose policy, the dollar-yen carry becomes more attractive. Conversely, policy convergence—both banks moving rates in the same direction—compresses carry opportunities. By 2026, with many developed market central banks clustered in the 3-5% range, classic carry trades offer slimmer pickings than a decade ago.

Successful carry traders monitor not just current interest differentials but expected policy paths. If the market anticipates the Reserve Bank of Australia will cut rates by 100 basis points over the next year while the Fed holds steady, the AUD carry becomes less attractive even if today's differential looks appealing. Forward-looking analysis matters more than backward-looking rate comparisons.

Why Covered Interest Arbitrage Is Considered Risk-Free

The "risk-free" label attached to covered interest arbitrage requires careful qualification. In theory, using forward contracts to hedge currency exposure eliminates exchange rate risk, leaving only the locked-in interest differential. In practice, several risks remain, though they're substantially lower than uncovered strategies.

The hedging mechanism works through precise coordination of spot and forward transactions. You execute four simultaneous steps: borrow in currency A, convert to currency B at the spot rate, invest in currency B assets, and enter a forward contract to convert back to currency A at maturity. When these four legs lock together, your profit is predetermined regardless of exchange rate movements.

Consider a concrete example: You borrow €1 million at 2.5% for one year. The spot rate is $1.08 per euro, giving you $1.08 million. You invest this in U.S. commercial paper yielding 4.2%. Simultaneously, you sell $1.08 million forward at a rate of $1.0975 per euro, locking in your ability to repay the euro loan. Your calculations show:

Interest income: $1.08 million × 4.2% = $45,360

Interest expense: €1 million × 2.5% = €25,000 (approximately $27,438 at forward rate)

Net profit: approximately $17,922, or 1.66% return

Author: Vanessa Cole;

Source: martinskikulis.com

This profit is "locked in" from day one. Exchange rate fluctuations don't matter because your forward contract fixes the conversion rate. Arbitrage equilibrium in fx markets means these opportunities should theoretically vanish as traders compete them away, but temporary dislocations do appear.

Why covered interest arbitrage is risk-free in theory but not quite in practice:

Counterparty risk: Your forward contract is only as good as the bank or dealer on the other side. During the 2008 crisis, counterparty concerns made even "risk-free" arbitrage feel risky.

Liquidity risk: If you need to exit early, unwinding four interconnected positions in volatile markets can be costly. The theoretical profit assumes you hold to maturity.

Operational risk: Mistakes in execution—wrong forward dates, mismatched amounts, incorrect rate quotations—can turn a profitable arbitrage into a loss.

Regulatory risk: Capital controls can trap your funds. Sudden rule changes might prevent repatriation or impose unexpected taxes.

Still, covered arbitrage remains the closest thing to a free lunch in finance when executed properly by well-capitalized institutions with sophisticated risk management systems. The profit margins are thin—often 10 to 50 basis points annually—but the risk-adjusted returns can be attractive when scaled appropriately.

Real World Limits to Interest Rate Arbitrage

Perfect arbitrage opportunities rarely exist outside textbooks. Multiple frictions constrain the ability to exploit interest differentials, keeping markets from achieving the theoretical equilibrium that finance models predict.

Transaction Costs and Market Frictions

Every arbitrage trade faces a gauntlet of costs that erode potential profits. Bid-ask spreads on currency conversions typically consume 2-5 basis points for major pairs, more for exotic currencies. If your arbitrage opportunity offers a 20 basis point annual return, a 4 basis point round-trip conversion cost claims 20% of your gross profit immediately.

Brokerage fees, custody charges, and wire transfer costs add up quickly. A typical institutional arbitrage trade might incur:

Currency conversion spreads: 3-4 basis points each way

Administrative and compliance costs: 5-15 basis points

Total friction: 25-60 basis points annually. An arbitrage opportunity needs to exceed this threshold just to break even. Real world arbitrage in fx markets therefore requires either large dislocations (which are rare and brief) or massive scale to make the thin margins worthwhile.

Timing mismatches create additional problems. Your borrowed funds might settle in two business days while your investment opportunity requires three-day settlement. This gap exposes you to rate changes and requires bridge financing, adding costs. Holiday calendars differ across countries—U.S. markets close for Thanksgiving while European markets operate normally, creating settlement complications.

Market impact matters for large trades. A $10 million arbitrage might execute at quoted prices, but a $1 billion position will move the market, widening spreads and reducing profitability. This scale constraint limits how much capital can chase any single opportunity.

Regulatory and Capital Constraints

Basel III banking regulations fundamentally changed the arbitrage landscape after 2013. Banks now face higher capital charges for derivative positions and balance sheet usage. A forward contract that previously required minimal capital now ties up regulatory capital, making arbitrage trades less attractive from a return-on-equity perspective.

The Supplementary Leverage Ratio (SLR) in the United States particularly constrains dealer banks. This rule requires banks to hold capital against total assets, including low-risk activities like matched-book arbitrage. When a bank borrows dollars, converts to euros, lends euros, and hedges with forwards, all four positions consume balance sheet space. The resulting capital charge can exceed the arbitrage profit, making the trade uneconomical.

Author: Vanessa Cole;

Source: martinskikulis.com

Capital controls in many emerging markets prevent free movement of funds. China maintains strict limits on capital outflows. India requires regulatory approval for certain forex transactions. Brazil has imposed taxes on foreign capital inflows during various periods. These restrictions either block arbitrage entirely or add costs that eliminate profitability.

Limits to interest rate arbitrage also stem from credit limits and counterparty restrictions. Even if a profitable opportunity exists with a Turkish counterparty, your risk management team might prohibit the trade due to country risk concerns. Credit lines with prime brokers fill up during volatile periods, preventing you from executing otherwise attractive arbitrage trades.

Tax treatment varies across jurisdictions in ways that complicate arbitrage calculations. Interest income might face withholding taxes in one country while capital gains receive preferential treatment in another. Currency gains might be taxed as ordinary income or capital gains depending on holding period and instrument type. These tax frictions require sophisticated structuring and often reduce after-tax returns below the apparent gross opportunity.

Common Mistakes in Currency and Interest Rate Arbitrage

The covered interest parity condition held remarkably well for decades, but since the financial crisis, persistent deviations have emerged even in the most liquid currency pairs. These violations reflect the new reality of banking regulation and balance sheet constraints, fundamentally altering the arbitrage landscape

— Dr. Wenxin Du

Even experienced traders stumble when executing arbitrage strategies. Recognizing these pitfalls helps avoid costly errors.

Ignoring the forward premium: Beginners see a 5% interest differential and assume they can capture the full spread. They forget that the forward rate typically reflects this differential, eliminating most of the apparent profit. Always calculate the net return after hedging costs, not just the gross interest spread.

Underestimating transaction costs: A strategy that looks profitable on paper might lose money after accounting for all frictions. Include every cost: bid-ask spreads, commissions, custody fees, wire charges, and opportunity costs of tied-up capital. Many arbitrage opportunities vanish under realistic cost assumptions.

Mismatching tenors: Borrowing for three months while investing for six months creates rollover risk. When your funding matures, you must refinance at potentially higher rates while your investment remains locked up. Always match the duration of your borrowing and lending as closely as possible.

Overleveraging: Arbitrage opportunities offer thin margins, tempting traders to use excessive leverage to boost returns. A 0.5% arbitrage return becomes 5% with 10:1 leverage—until a small adverse move wipes out your capital. Leverage amplifies both gains and losses, and even "risk-free" arbitrage can suffer from operational errors or market disruptions.

Neglecting tail risks: Covered arbitrage protects against normal exchange rate movements but not against extreme events. Currency pegs can break suddenly (Swiss franc in 2015), capital controls can trap funds (Cyprus in 2013), or counterparties can default (Lehman Brothers in 2008). These tail risks are hard to quantify but can devastate an arbitrage portfolio.

Poor timing: Entering an arbitrage trade just before a central bank announcement or major economic release adds unnecessary risk. Even covered positions can suffer from execution slippage during volatile periods. Wait for calmer conditions when spreads are tighter and execution more predictable.

Forgetting about opportunity cost: Tying up capital for a 0.3% arbitrage return might seem worthwhile until you consider alternative uses. Could that capital earn better risk-adjusted returns elsewhere? Arbitrage trades consume credit lines and balance sheet capacity that might be more profitably deployed in other strategies.

Covered vs Uncovered Interest Arbitrage: Key Differences

Is interest rate arbitrage legal for individual investors?

Yes, interest rate arbitrage is completely legal for retail investors in the United States and most developed markets. You can borrow in one currency through margin accounts at forex brokers and invest in another currency's assets. However, individual investors face higher transaction costs than institutions, making profitable arbitrage opportunities scarce. Regulatory restrictions may apply to certain jurisdictions or account types, and you must comply with tax reporting requirements for foreign currency gains and losses.

How much capital do you need to profit from interest rate arbitrage?

Minimum capital requirements vary by strategy. Covered arbitrage through institutional channels typically requires $1-10 million to achieve economies of scale that overcome transaction costs. Retail carry trades can start with $10,000-25,000 in margin accounts, though profitability remains challenging at smaller scales. The thin margins in arbitrage—often 0.2-1.0% annually after costs—mean you need substantial capital for absolute dollar profits to be meaningful. A 0.5% return on $50,000 yields just $250 annually, barely worth the effort and risk.

Can interest rate arbitrage still work in low-rate environments?

Arbitrage opportunities persist even when absolute rate levels are low, as long as differentials exist between currencies. During 2020-2021, when U.S. rates fell near zero, differentials with emerging markets like Turkey (17%), Brazil (12%), and Russia (6%) remained substantial. By 2026, with developed market rates generally higher, the opportunity set has shifted. Smaller differentials between major currencies (dollar, euro, yen) make covered arbitrage less attractive, while emerging market carry trades still offer potential—albeit with higher risk. The strategy adapts to the environment rather than disappearing entirely.

What is the relationship between interest rate parity and arbitrage?

Interest rate parity represents the theoretical equilibrium condition where arbitrage opportunities cease to exist. Covered interest parity states that interest differentials should equal forward premiums, eliminating covered arbitrage profits. Uncovered interest parity suggests expected exchange rate changes should offset interest differentials. In reality, both parity conditions are frequently violated, creating arbitrage opportunities. These violations stem from transaction costs, regulatory constraints, risk premiums, and market imperfections. Arbitrageurs profit by exploiting parity deviations, and their trading activity pushes markets back toward equilibrium—though perfect parity rarely holds for long.

How quickly do arbitrage opportunities disappear in forex markets?

In highly liquid major currency pairs, obvious arbitrage opportunities vanish within seconds to minutes as algorithmic trading systems detect and exploit them. High-frequency trading firms monitor covered interest parity deviations continuously, executing trades at microsecond speeds when profitable dislocations appear. For less liquid currency pairs or during market stress, opportunities might persist for hours or even days. The 2020 COVID market disruption created covered interest parity violations that lasted weeks as dealer balance sheets became constrained. Generally, larger and more obvious arbitrages disappear faster, while small, complex opportunities requiring specialized knowledge or access may last longer.

Do central bank policies affect interest rate arbitrage opportunities?

Central bank policies are the primary driver of arbitrage opportunities. When the Federal Reserve raises rates while the European Central Bank holds steady, the dollar-euro interest differential widens, creating carry trade opportunities. Forward guidance also matters—if the Bank of Japan signals sustained low rates while other central banks tighten, yen-funded carry trades become more attractive. Unconventional policies like quantitative easing can distort covered interest parity by affecting demand for government bonds and currency hedging. By 2026, central bank balance sheet normalization and varied policy stances across jurisdictions continue to create the interest differentials that make arbitrage possible, though regulatory constraints limit the ability to exploit them fully.

Interest rate arbitrage remains a fundamental force in global currency markets, exploiting interest differentials between countries to generate returns. While covered strategies using forward contracts offer near risk-free profits in theory, real-world frictions—transaction costs, regulatory constraints, and operational risks—significantly limit practical opportunities. Uncovered approaches and carry trades provide higher potential returns but expose investors to substantial currency risk.

The landscape has evolved considerably since the 2008 financial crisis. Basel III regulations, increased capital charges, and sophisticated algorithmic trading have compressed arbitrage margins and shortened opportunity windows. Yet interest differentials persist as central banks pursue divergent policies, ensuring that arbitrage strategies continue to play a role in portfolio management and market efficiency.

Success in interest rate arbitrage requires understanding not just the theoretical framework but the practical constraints that separate textbook examples from profitable trades. Transaction costs must be meticulously calculated, risks properly hedged or consciously accepted, and positions sized appropriately for the thin margins involved. For institutional investors with scale, expertise, and low-cost execution capabilities, arbitrage opportunities still exist. For retail investors, the challenges are substantial but not insurmountable, particularly in carry trade strategies where longer holding periods and higher risk tolerance can compensate for execution disadvantages.

As global capital markets continue to evolve, interest rate arbitrage adapts rather than disappears. Understanding both the opportunities and limitations of these strategies provides essential insight into how exchange rates are determined and how sophisticated investors generate returns in currency markets.

Swap rates represent the interest cost or credit applied when forex traders hold positions past the daily rollover time. Understanding how these overnight fees work, when you pay or earn them, and their cumulative impact is essential for swing traders and anyone implementing carry trade strategies in 2026

Spread betting lets you speculate on market moves without owning the asset. This guide walks through real examples—long and short positions, forex pairs, margin calculations—showing exactly how profits and losses accumulate, how to size stakes responsibly, and what happens when trades go wrong

An overnight index swap is a derivative where parties exchange fixed and floating interest payments based on compounded overnight rates. These instruments have become the standard for derivatives discounting and provide key insights into central bank policy expectations and market stress levels

Interest rate movements can transform profitable loans into financial burdens overnight. Companies with floating-rate debt and bond investors face the same challenge: protecting against adverse rate shifts without sacrificing upside. This guide explains hedging instruments, duration strategies, and how to match protection to your specific exposure

The content on this website is provided for general informational and educational purposes only. It is intended to explain concepts related to Forex (FX) trading, currency markets, leverage, hedging, and risk management.

All information on this website, including articles, guides, and examples, is presented for general educational purposes. Forex trading carries significant risk, and outcomes may vary depending on market conditions, leverage, and individual decisions.

This website does not provide financial, investment, or trading advice, and the information presented should not be used as a substitute for consultation with qualified financial professionals.

The website and its authors are not responsible for any errors or omissions, or for any outcomes resulting from decisions made based on the information provided on this website.