Modern finance office with a large monitor displaying a currency exchange rate line chart, documents on the desk, and a panoramic city skyline view through the window

Author: Marcus Ellington;Source: martinskikulis.com

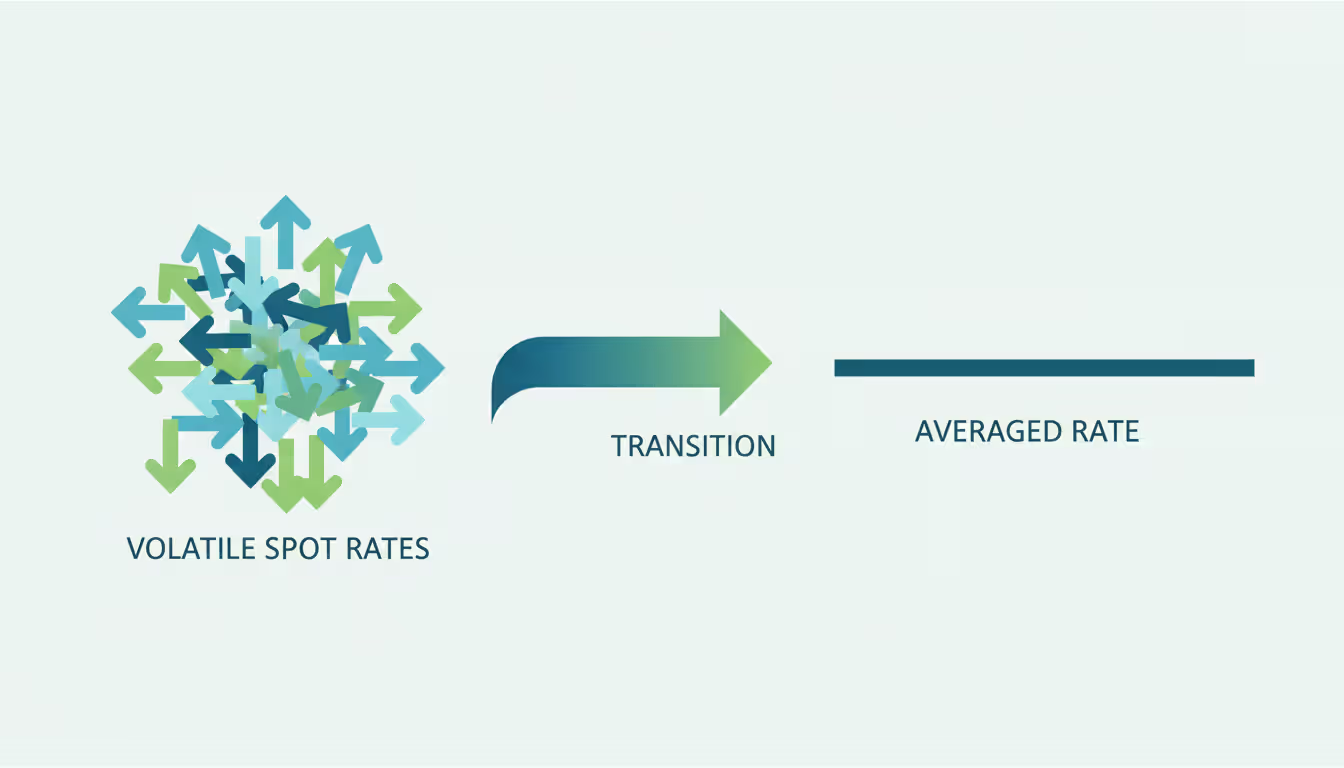

Your finance team just spent three hours tracking down exchange rates for last month's European invoices. Sound familiar? International operations mean currency translation, and if you're converting every transaction at its precise moment's rate, you're burning time that could go toward actual analysis. There's a smarter approach: average exchange rates let you handle foreign currency accounting without obsessing over every pip movement in the forex market.

What Is an Average Exchange Rate?

Take all the exchange rates between two currencies during a specific timeframe—say, every business day in March—and calculate their mean. That's your average exchange rate for the period.

Here's the thing: spot rates (the price of currency right this second) jump around constantly. The EUR/USD might hit 1.0850 at 9 AM, drift to 1.0920 by lunch, and settle at 1.0875 by market close. If you run a subscription software business charging European customers monthly, which rate do you use? The moment each payment processed? The day you recognized the revenue?

Most companies would go crazy tracking that level of detail. You'd need different rates for every transaction, and your month-to-month comparisons would get messy—did revenue really grow, or did favorable timing on invoice processing just make it look that way?

Averages cut through this noise. They give you one representative rate that captures normal conditions across the whole period. Your income statement shows what actually happened to the business, not random fluctuations from whether transactions cleared on lucky versus unlucky days.

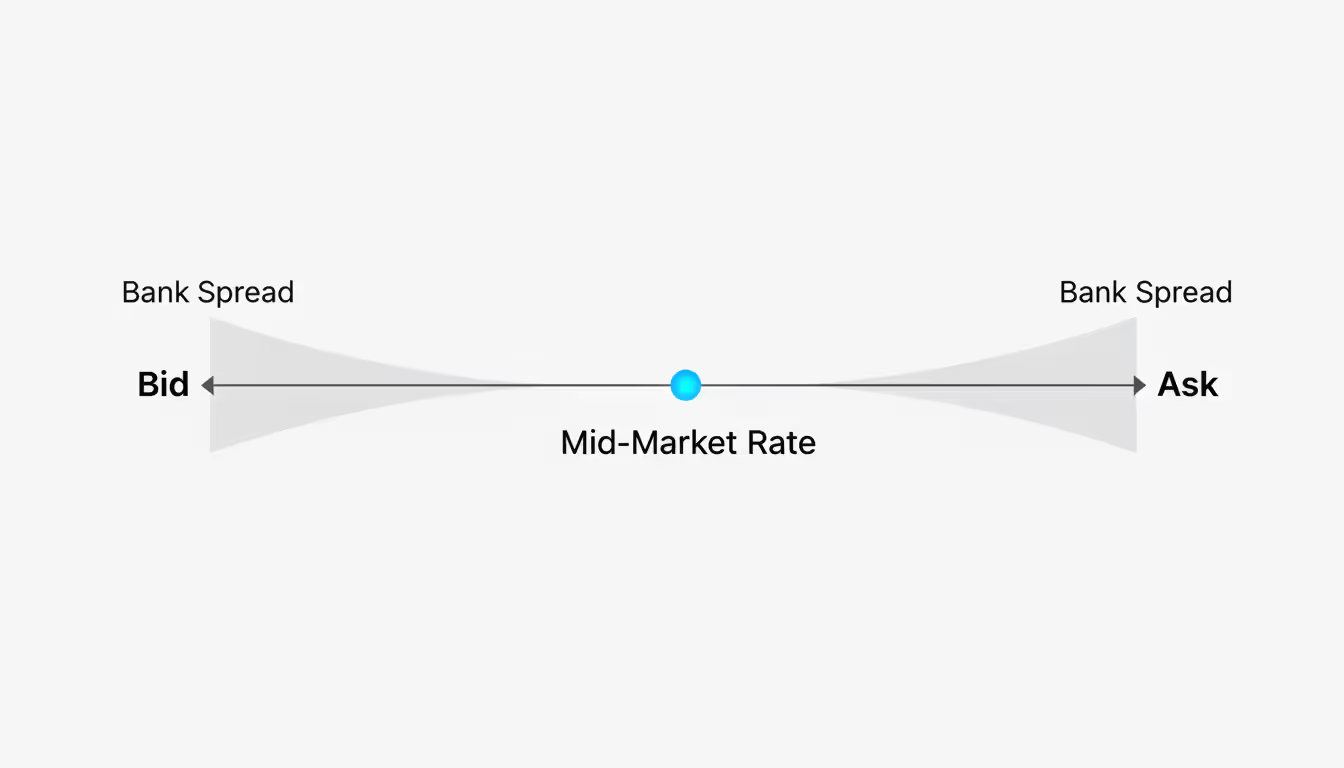

The mid-market rate sits dead center between what dealers pay for currency (the bid) and what they charge to sell it (the ask). Check Bloomberg or Reuters right now for EUR/USD. See 1.0850? That's the mid-market rate—the true wholesale price before anyone adds their spread. Your bank might quote 1.1000 when selling you euros and 1.0700 when buying them back. They're adding roughly 1.4% on each side of that 1.0850 mid-market rate.

For accounting purposes, you want mid-market rates. Why? Because financial statements should reflect economic reality, not the markup your particular bank charges. The mid-market rate shows what the currency is actually worth in the global market. When determining fair exchange rates for translation, this wholesale benchmark keeps your numbers honest.

Author: Marcus Ellington;

Source: martinskikulis.com

How Average Exchange Rates Are Calculated

Three calculation methods dominate: simple average, weighted average, and time-weighted average. Your choice matters more than you'd think.

A simple arithmetic average just adds up rates and divides by how many you've got. GBP/USD trades at 1.2500 Monday, 1.2550 Tuesday, 1.2600 Wednesday? Add them up (3.7650), divide by three days, and you land at 1.2550.

This works fine when transaction volumes stay relatively consistent. But what if you process tiny amounts on Mondays and Wednesdays, then handle your main weekly transfers on Tuesdays? The simple average treats all three days equally, even though Tuesday's rate affected ten times more money.

Weighted Average Exchange Rate Formula

Weighted averages account for transaction size. Bigger deals get more influence on the final number—exactly as they should, since they represent more of your actual exposure.

Notice the difference? The weighted approach gives that middle transaction—your biggest one at ¥10 million—appropriate influence. You paid 146.50 for more than half your yen, so your effective rate should reflect that reality.

Author: Marcus Ellington;

Source: martinskikulis.com

Daily vs. Monthly Average Rates

Daily averages typically blend a day's high, low, opening, and closing rates. Some data providers sample rates every hour and average those. Either way, you're smoothing intraday volatility into one number per day.

Who needs daily rates? High-frequency operations. Payment processors moving money for thousands of customers daily. Forex trading desks. Import/export businesses dealing in volatile emerging market currencies. If you're processing 500 transactions per day in Turkish lira (which can swing 2-3% in an afternoon), daily averages help you track what's really happening.

Monthly averages smooth out the whole month's movement. Most companies calculate this as the arithmetic mean of daily mid-market rates for all business days in the month. Some weight by transaction volume on each day if they've got the systems to track it.

Monthly averages hit the sweet spot for typical multinationals. You're not chasing daily noise, but you're still capturing meaningful trends. A manufacturing company selling machinery to Latin American distributors probably books a few large orders per month—monthly averages match that operational rhythm while keeping bookkeeping sane.

The tradeoff: daily averages react faster when currencies move sharply, but you'll spend more time calculating and explaining period-to-period changes. Monthly averages simplify your life and make trend analysis clearer, though they might lag a bit during volatile periods.

Rate Type

How Often Updated

Works Best For

Where to Get Data

How It Handles Volatility

Standards Compliance

Daily

Each business day

Payment processors, active traders, emerging market currencies

Central banks, Bloomberg terminals, Reuters feeds

Catches quick moves; minimal smoothing

Fine under GAAP/IFRS when justified

Monthly

Month-end

Standard business accounting, SaaS companies, regular trade flows

Federal Reserve, ECB, XE historical data

Balances stability with responsiveness

Default choice for most companies

Quarterly

Quarter-end

Infrequent transactions, quarterly-only reporters

Built from daily or monthly data

Smooths significantly; can mask trends

Allowed but less common

Annual

Year-end

Tax filings, annual reports, multi-year contracts

IRS publications, central bank annual data

Maximum smoothing; strategic view

Required for some tax calculations

When to Use Average Rates for Currency Translation

U.S. GAAP (specifically ASC 830) and International Financial Reporting Standards (IAS 21) both spell out when averages make sense versus when you need spot rates.

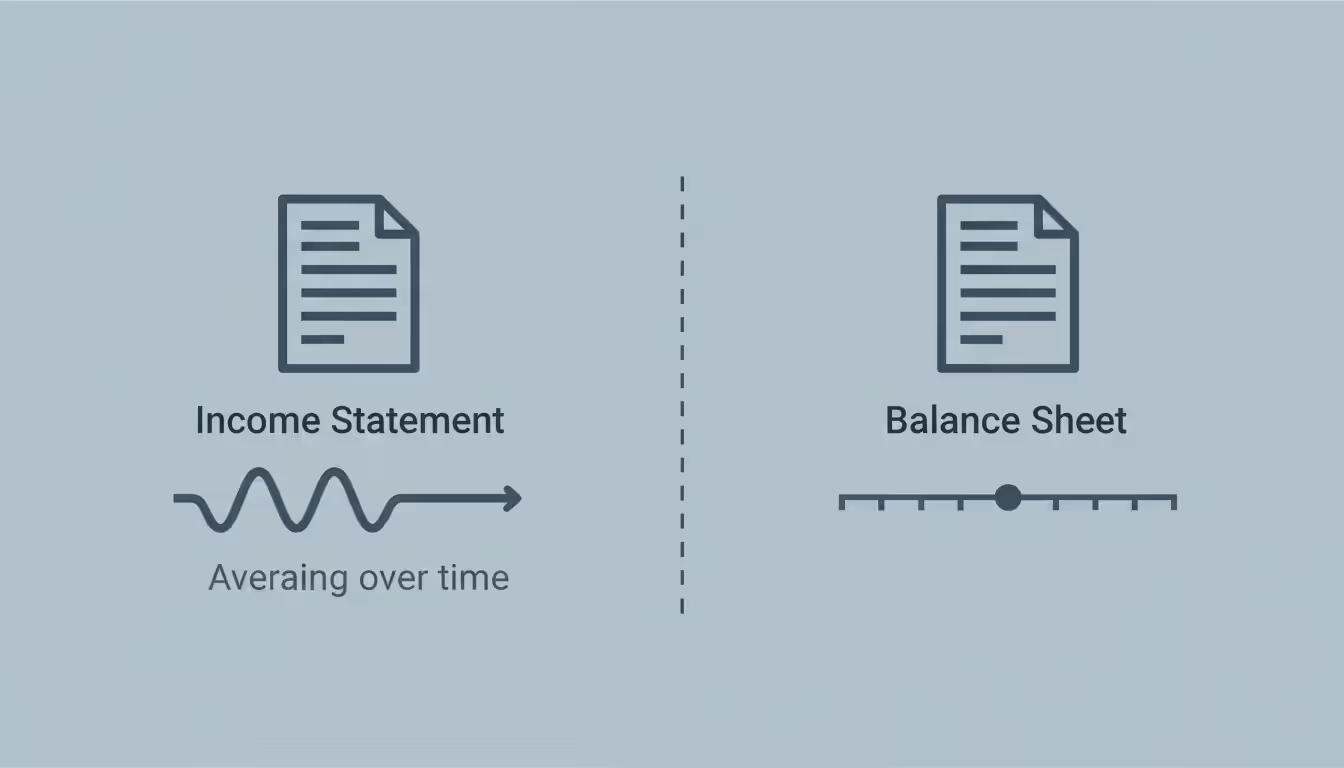

First, understand functional versus reporting currency. Your functional currency is whatever currency dominates your economic environment—where you generate and spend most of your cash. A German subsidiary of a U.S. parent operates in euros (functional currency), but the parent's consolidated statements use dollars (reporting currency).

When translating that German subsidiary's financials into dollars, you'll split the balance sheet and income statement. Revenue, expenses, gains, and losses—basically your entire income statement—generally get translated using average rates for the period. Makes sense, right? Sales happen all month long, so using September's average EUR/USD rate captures the conditions under which those sales occurred.

Author: Marcus Ellington;

Source: martinskikulis.com

But cash, receivables, inventory, payables? Those balance sheet items exist at a specific point in time, so you translate them at the spot rate on that date. Cash sitting in a German bank account on September 30 is worth whatever EUR/USD traded at on September 30, not the monthly average.

Here's a real scenario: Your U.K. subsidiary books £2 million in consulting revenue throughout Q2. Rather than tracking the exact GBP/USD rate for each of the 47 client invoices issued across April, May, and June, you apply Q2's average rate to the total. Maybe that's 1.2650. Multiply £2 million by 1.2650, and you've got $2,530,000 in USD-equivalent revenue for consolidation.

This approach satisfies both GAAP and IFRS while keeping your accounting team's workload reasonable. Standards writers understand that tracking individual transaction rates for ongoing operations would be absurd.

One major exception: significant one-off transactions. If you acquire a foreign business on May 15 for £50 million, use May 15's spot rate for that purchase price. Don't blend it into your monthly average—the acquisition happened at a specific moment, and that moment's economics matter.

Types of Average FX Rates Used in Business

Matching your averaging period to your business rhythm prevents both unnecessary work and misleading numbers.

Daily averages suit businesses that can't afford to ignore short-term currency moves. A fintech startup facilitating cross-border payments for e-commerce companies might process $5 million across 1,000 transactions daily. Daily averaging lets them track margin impact from currency movement without getting lost in tick-by-tick rate changes. The downside? More data management and noisier period comparisons.

Monthly averages dominate business accounting for good reason. Most companies close their books monthly, have relatively steady international activity, and want to smooth volatility without sacrificing relevance. If you're a consulting firm with retainer clients across Asia-Pacific billing at month-end, monthly averages align perfectly with your revenue cycle. Calculate once per currency pair per month, apply it consistently, move on.

Quarterly averages appeal to companies with genuine quarterly rhythms or lower-volume international operations. A software company licensing products to a dozen European distributors might sign most deals at quarter-end when sales teams hit quota. Quarterly averaging reduces administrative burden versus monthly calculations. Watch out, though—a sharp currency move in week 12 of a 13-week quarter barely registers in the average, potentially hiding important developments.

Annual averages show up mainly in tax reporting and year-end financial statements. The IRS publishes annual average rates that many companies use for tax calculations. Some long-term contracts reference annual averages for pricing adjustments. Just don't rely on annual averages for management reporting—they're too broad to guide operating decisions.

Practical rule of thumb: use the shortest averaging period that doesn't create unnecessary administrative headaches. Got daily euro revenue from hundreds of customers? Monthly averages probably make sense. Quarterly royalty payment from one Japanese partner? A quarterly average does the job.

Finding Fair and Accurate Exchange Rates

Not every exchange rate you encounter reflects real market conditions. Banks and exchange services add profit margins that can reach 3-5% above mid-market rates.

The mid-market rate—sometimes called the interbank rate—represents the true wholesale price where major financial institutions trade with each other. See "1 EUR = 1.0850 USD" on a financial website? That's almost certainly the mid-market rate before any retail markup.

Why does this matter for accounting? Because your financial statements should show economic substance, not the cost of your banking relationships. If you translate using your bank's customer rate of 1.1000 when the market rate is 1.0850, you're understating foreign revenue by about 1.4%. Fine if you're trying to measure transaction costs, but not appropriate for basic financial reporting.

Author: Marcus Ellington;

Source: martinskikulis.com

Where do you find reliable mid-market rates?

Central banks publish official reference rates. The European Central Bank posts daily euro rates against 30+ currencies. The Federal Reserve provides noon buying rates for major pairs. These carry official weight useful during audits.

Financial data terminals like Bloomberg and Reuters offer the most comprehensive rate data, including historical averages. They're expensive, though—primarily for companies that trade currencies actively or need extensive historical analysis.

Specialized currency platforms (XE.com, OANDA, Wise) provide free access to current and historical mid-market rates. They've built businesses around transparency, so rate accuracy matters to their reputation. For monthly average calculations, these sources work fine for most companies.

The Federal Reserve Bank of New York publishes monthly average rates for major currency pairs, which many U.S. companies use as an authoritative benchmark. If you calculate your own monthly EUR/USD average and want to verify it, check it against the NY Fed's published figure.

Here's a critical verification step: cross-check rates from multiple sources. You calculated a monthly average AUD/USD rate of 0.6450, but the Reserve Bank of Australia's published monthly average shows 0.6725? Something went wrong—maybe you accidentally mixed up bid and ask rates, or grabbed rates from different time zones. Always validate against at least one authoritative source before booking entries.

Avoid a common mistake: using your bank's transaction confirmation rates for financial statement translation. That confirmation showing they converted your euros at 1.1050 reflects their retail pricing, not market rates. Perfect for reconciling what actually hit your account, inappropriate for translating your P&L.

Common Mistakes When Applying Average Exchange Rates

Even seasoned controllers stumble on currency translation. Here's what goes wrong most often.

Inconsistent rate types across related transactions creates artificial distortions. Imagine recognizing Japanese revenue at monthly average rates but recording related commission expenses at daily spot rates. If the yen strengthens throughout the month, your average rate might be 145.00 while several daily rates hit 148.00. Suddenly your margins look worse—not because business performance changed, but because you mixed calculation methods.

Solution: document which rate type applies to which transaction category, then stick to it religiously. Revenue, cost of sales, and operating expenses should generally use the same averaging period.

Ignoring extreme volatility makes averages misleading. Say GBP/USD trades quietly between 1.2500-1.2550 for 27 days, then the Bank of England surprises markets with an emergency rate hike, and the pound rockets to 1.3100 over the final three days of the month. Your simple monthly average lands around 1.2650, suggesting stable conditions when reality involved a dramatic regime change.

In volatile periods, consider whether a simple average truly captures your exposure. You might segment the month into pre-event and post-event periods for management reporting, or use weighted averages based on when transactions actually occurred.

Wrong weighting approaches defeat the purpose of weighted averages. Common errors include weighting by transaction count (treating 100 small transactions the same as one large one) or weighting by transaction days while excluding non-business days when currencies still trade.

A distribution company once weighted its monthly average by shipment days only—they didn't ship on weekends, so they excluded Saturday and Sunday rates. Seemed logical until a major geopolitical event moved currencies 4% over a weekend. Excluding those days skewed their average away from economic reality.

Compliance misunderstandings trip up companies that don't fully grasp what standards actually require. Some teams think GAAP mandates using identical averaging periods for all income statement items. Actually, standards allow different approaches for different transaction types, as long as you're consistent and reasonable.

Another compliance trap: applying average rates to transactions that require spot rate treatment. Purchased a building in Mexico on June 15? That fixed asset gets translated at June 15's spot rate, not the monthly or quarterly average. Large capital transactions need point-in-time treatment.

Inadequate documentation causes audit headaches. Your external auditors need to understand your methodology: which averaging method, which data source, which period, and why you chose that approach. A simple policy memo stating "We translate euro-denominated revenue using monthly arithmetic averages of daily mid-market rates from the European Central Bank" prevents hours of Q&A during fieldwork.

I've watched companies twist themselves into knots over exchange rate methodology, convinced they need sophisticated weighted calculations when simple monthly averages would better reflect their business. The most important thing isn't picking the theoretically perfect method—it's choosing one that makes sense for your operations and applying it consistently. I've also seen the opposite problem: teams who thought 'consistency' meant never adjusting their approach, even when their business model changed fundamentally. Smart currency accounting matches your methodology to your reality, then documents why you made that choice

— Jennifer Martinez

FAQ: Average Exchange Rates

What is the difference between spot rate and average exchange rate?

Spot rates show what currency trades for at one specific moment—right now, or on a particular date like December 31. Average rates take multiple spot rates across a period and calculate their mean. Use spot rates for balance sheet items that exist at a point in time (cash, payables, receivables). Use average rates for income statement items that accumulate across the period (revenue, expenses). Example: your year-end cash balance gets translated at the December 31 spot rate, but your annual sales revenue uses the full year's average rate.

How do you calculate a weighted average exchange rate?

Multiply each rate by the dollar value (or volume) of transactions that occurred at that rate. Add up all those products, then divide by total transaction value. Here's the math: Σ(Rate × Transaction Value) ÷ Σ(Transaction Value). If you bought Australian dollars three times—A$200,000 at 0.6500, A$500,000 at 0.6550, and A$100,000 at 0.6480—your weighted average is [(0.6500 × 200K) + (0.6550 × 500K) + (0.6480 × 100K)] ÷ 800K = 0.6531. Notice this gives your largest transaction (A$500K) appropriate influence on the result.

What is a cross rate and how is it calculated?

Cross rates express the exchange rate between two currencies by using their rates against a third currency (usually the U.S. dollar). Need the EUR/GBP rate but only have EUR/USD (1.0850) and GBP/USD (1.2650)? Calculate: EUR/GBP = EUR/USD ÷ GBP/USD = 1.0850 ÷ 1.2650 = 0.8577. This means one euro equals roughly 0.86 British pounds. Cross rates matter when you can't find direct quotes for currency pairs or when you're verifying consistency across multiple currencies in your system.

Should I use daily or monthly average rates for accounting?

Monthly averages suit most businesses—they smooth daily noise while matching typical accounting cycles. You'll spend less time calculating rates and get cleaner period-to-period comparisons. Switch to daily averages only if you've got high transaction volumes, deal in volatile currencies, or have automated systems that make daily calculations painless. Quarterly averages work for infrequent international activity but might hide important trends. Whatever you choose, apply it consistently to similar transactions every period. Your business rhythm should drive the decision, not theoretical perfection.

Where can I find reliable mid-market exchange rates?

Central banks (Federal Reserve, European Central Bank, Bank of England) publish daily reference rates with official authority. The Federal Reserve Bank of New York posts monthly averages that many U.S. companies use for accounting. Financial platforms like OANDA and XE.com provide free access to current and historical mid-market rates accurate enough for most business needs. Bloomberg and Reuters terminals offer the most comprehensive data but cost thousands annually. Always cross-check your calculated averages against at least one authoritative source—if your monthly EUR/USD average differs materially from the Fed's published number, investigate why.

Do GAAP and IFRS require average exchange rates?

Both frameworks encourage (and in most cases effectively require) average rates for income statement translation, but neither mandates a specific averaging period. GAAP's ASC 830 and IFRS's IAS 21 focus on principles: translate items that accumulate over time (revenue, expenses) using rates that reflect conditions during that period. You can use daily, monthly, quarterly, or annual averages—whatever reasonably represents your economics. Balance sheet monetary items must use spot rates as of the balance sheet date under both standards. The key is consistency and reasonableness, not following a prescribed formula.

Currency translation doesn't have to be the monthly headache that keeps your accounting team late at the office. Average exchange rates turn a potentially unmanageable tracking exercise into a systematic process that produces meaningful financial statements without overwhelming administrative burden.

Match your averaging period to how your business actually operates internationally. Process thousands of small transactions daily? Monthly averages probably hit the sweet spot between accuracy and sanity. Handle a few large quarterly deals? Quarterly averages might work fine. The right methodology reflects your operational reality, not someone else's theoretical ideal.

Source your rates from mid-market benchmarks published by central banks or reputable financial data providers. Document which sources you use, which calculation method you've chosen, and why that approach makes sense for your business. This documentation serves your accounting team (ensuring consistent application) and your auditors (providing the paper trail they need).

Then stick with it. Consistency matters more than perfection. Switching calculation methods every quarter because you read about a theoretically superior approach creates more problems than it solves. Your stakeholders need to compare periods meaningfully, which requires stable methodology.

Exchange rates will keep bouncing around—that's the nature of currency markets. But with solid averaging practices, those movements inform your analysis instead of obscuring your actual business performance. Start by documenting what you're doing now, verify it against authoritative sources, and make sure everyone on your team understands the approach. That foundation keeps your international financials accurate, defensible, and useful for decision-making.

The pound to dollar exchange rate reflects economic health, central bank policy, and political stability. This guide explains what drives Cable, historical context, purchasing power parity, seasonal patterns, and expert forecasts for 2026 to help Americans make informed currency decisions

Non-Farm Payroll releases create dramatic currency market swings on the first Friday of most months. Learn what NFP means for forex traders, how employment data drives USD volatility, and proven strategies for trading this high-impact economic event safely and profitably

The British pound has traded within 1.2450-1.2850 against the dollar through early 2026, reflecting balanced fundamentals. Interest rate differentials, inflation dynamics, and Brexit's lasting impact shape the pair's outlook, with major banks forecasting modest weakness toward 1.2400 over 12 months

Forex volatility describes the rate and magnitude of price changes in currency pairs. This guide covers measurement methods like ATR and historical volatility, explores factors driving volatility including news events and VIX correlation, and provides practical strategies for trading both high and low volatility conditions

The content on this website is provided for general informational and educational purposes only. It is intended to explain concepts related to Forex (FX) trading, currency markets, leverage, hedging, and risk management.

All information on this website, including articles, guides, and examples, is presented for general educational purposes. Forex trading carries significant risk, and outcomes may vary depending on market conditions, leverage, and individual decisions.

This website does not provide financial, investment, or trading advice, and the information presented should not be used as a substitute for consultation with qualified financial professionals.

The website and its authors are not responsible for any errors or omissions, or for any outcomes resulting from decisions made based on the information provided on this website.