An interest rate hedge is a financial strategy designed to reduce or eliminate the risk that changes in benchmark interest rates will hurt your portfolio's value. For currency and forex traders, this isn't an academic exercise—interest rate differentials drive capital flows and exchange rate movements every trading day.

When you hold a position in a currency pair, you're implicitly exposed to the interest rate policies of two central banks. If the Federal Reserve raises rates while the European Central Bank holds steady, the dollar typically strengthens against the euro as investors chase higher yields. But what happens when you're carrying a multi-month position and rates move against you? Without protection, your profit can evaporate or turn into a loss, even if your directional call on the currency was correct.

Interest rate hedging matters because forex positions often involve leverage, magnifying both gains and losses. A 50-basis-point surprise rate hike can trigger a 2–3% move in a major currency pair within hours. For a leveraged position, that translates to double-digit percentage swings in account equity. Hedging allows you to isolate the currency view you want to express while managing the rate risk you'd prefer to avoid.

Currency traders face interest rate exposure through several channels: the carry embedded in spot positions, the forward points in rolling contracts, and the yield differential that determines swap rates on overnight holdings. Professional traders and institutional desks routinely hedge this exposure; retail traders who ignore it often discover the hard way that a correct currency forecast doesn't guarantee a profitable trade.

How Interest Rate Risk Affects Forex and Currency Positions

Interest rates and currency values are joined at the hip. When a country's central bank raises rates, its currency typically attracts inflows from investors seeking higher returns. This relationship—known as interest rate parity in academic literature—means that forex positions are always sensitive to rate changes, even when you're focused purely on technical chart patterns or macroeconomic trends.

The mechanism works through capital flows. Higher rates make a currency more attractive for deposits and bonds. International investors sell their home currency and buy the higher-yielding one, driving up demand. The effect is strongest when rate changes are unexpected or when the differential between two countries widens significantly.

Duration and interest rate sensitivity measure how much a position's value will change when rates move. In forex, this isn't as straightforward as in bond markets, but the principle holds: longer holding periods and larger rate differentials create more exposure. A trader holding a six-month forward contract on EUR/USD is more exposed to Fed and ECB policy shifts than someone trading intraday spot.

Author: Olivia Kensington;

Source: martinskikulis.com

Fixed vs Floating Rate Risk in Currency Portfolios

Fixed rate risk arises when you lock in an exchange rate or yield for a future date. Suppose you enter a forward contract to sell euros and buy dollars in 90 days at a predetermined rate. If U.S. interest rates rise sharply during that period, the dollar strengthens, and your locked-in rate becomes less favorable—you're selling euros at a worse price than the current market would offer. You've crystallized your exposure to the rate environment at the time you entered the contract.

Floating rate risk, by contrast, comes from positions that reprice continuously as rates change. Spot forex positions rolled overnight incur swap charges or credits based on the prevailing interest rate differential. When central banks adjust policy, these daily costs shift immediately. A carry trade that was profitable at a 200-basis-point differential can turn unprofitable if the gap narrows to 50 basis points, even if the exchange rate itself doesn't move.

Currency portfolios typically contain both types of risk. A desk might hold spot positions (floating exposure) alongside options or structured products (fixed exposure). The key difference: floating exposure adjusts automatically but leaves you vulnerable to ongoing volatility, while fixed exposure locks in a rate but creates opportunity cost if conditions improve.

Duration and Interest Rate Sensitivity

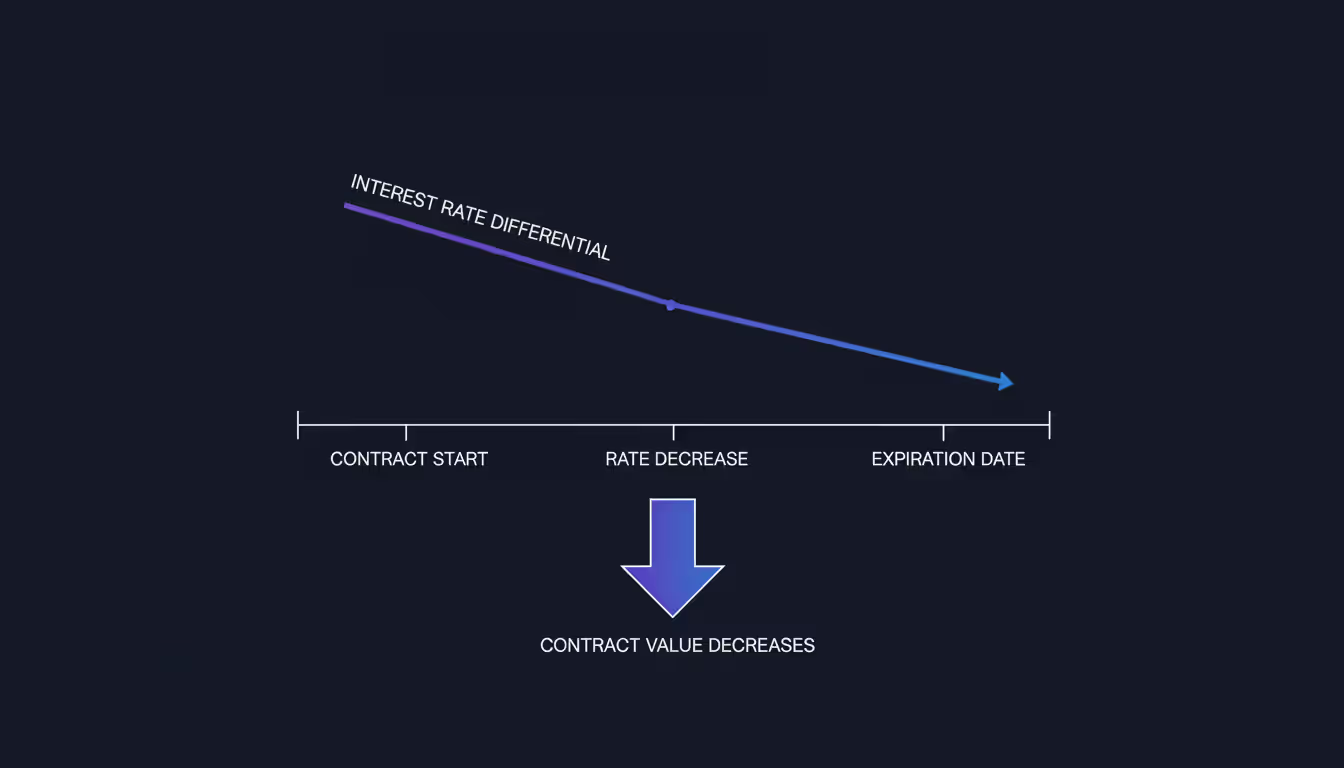

Duration quantifies how sensitive a position is to interest rate changes. In bond markets, duration is measured in years and represents the approximate percentage change in value for a 1% rate move. Forex traders encounter duration risk primarily through forward contracts, swaps, and options with longer maturities.

A three-month currency forward has roughly three months of duration—its value will shift as the interest rate differential evolves over that period. If you're long a forward contract on a high-yielding currency and the central bank cuts rates unexpectedly, the forward premium collapses and your position loses value before the contract even settles.

Practical example: You buy a six-month AUD/USD forward at 0.6800, expecting the Australian dollar to strengthen. The Reserve Bank of Australia was paying 4.25% while the Fed was at 3.50%, giving you a 75-basis-point carry advantage. Two months later, the RBA cuts rates to 3.75% due to slowing growth. The carry advantage shrinks to 25 basis points, the forward premium evaporates, and your contract is now worth less—even if the spot rate hasn't changed. That's duration risk in action.

Author: Olivia Kensington;

Source: martinskikulis.com

Common Interest Rate Hedging Instruments and Strategies

Forex traders have several tools to manage interest rate exposure, each with distinct mechanics, costs, and applications. The choice depends on your position size, time horizon, and whether you want to eliminate risk entirely or just reduce it.

Instrument

How It Works

Best Use Case

Complexity

Typical Cost

Interest Rate Swaps

Exchange fixed for floating rate payments on a notional amount

Hedging multi-year currency exposure or carry trades

High (requires ISDA documentation)

Bid-offer spread ~2–5 bps

Futures

Standardized contracts on interest rate benchmarks (e.g., SOFR, Eurodollar)

Short-to-medium term hedging with high liquidity

Medium

Commission + bid-offer spread

Options (Caps/Floors)

Buyer pays premium for protection if rates move beyond a threshold

Hedging tail risk while keeping upside potential

Medium to High

Premium ~0.5–2% of notional

Forward Rate Agreements

Lock in a future interest rate for a specific period

Precise hedging of known future cash flows

Medium

Bid-offer spread ~1–3 bps

Hedging Rate Exposure with Interest Rate Swaps

Interest rate swaps are the workhorse of institutional rate hedging. In a plain-vanilla swap, you agree to exchange fixed-rate payments for floating-rate payments (or vice versa) on a notional principal amount. The principal never changes hands—you're only swapping the interest cash flows.

For currency traders, swaps hedge the interest component of forex positions. Suppose you're long 10 million euros against dollars for the next two years, expecting the euro to appreciate. You're exposed to the risk that the ECB raises rates faster than the Fed, which would increase your funding cost (you pay euro interest, receive dollar interest). To hedge, you enter a euro interest rate swap: you pay fixed and receive floating. If euro rates rise, the floating leg of your swap pays you more, offsetting the higher cost of holding your long euro position.

Swaps offer precise customization—you choose the notional, maturity, and fixed rate. The downside is complexity and cost. You need an ISDA master agreement, credit support annex, and often a minimum notional of $1–5 million. Retail traders rarely access swaps directly; institutional desks and hedge funds use them routinely.

One common mistake: failing to match the swap's floating index to your actual exposure. If your forex position incurs costs based on overnight SOFR but your swap references three-month SOFR, you've introduced basis risk—the two rates can diverge, leaving you incompletely hedged.

Using Futures and Options to Manage Rate Risk

Interest rate futures—contracts on benchmarks like SOFR or the Fed Funds rate—offer a standardized, exchange-traded way to hedge. Each contract represents a fixed notional (e.g., $1 million) and settles based on the average interest rate over a specific period.

A forex trader expecting the Fed to hike rates more aggressively than priced in might short SOFR futures to hedge a long dollar position. If rates rise, the futures gain value, offsetting losses on the currency side. Futures are liquid, transparent, and require no bilateral negotiation. The trade-off: standardized maturities and sizes may not align perfectly with your forex exposure, creating some residual risk.

Options on interest rates—caps, floors, and swaptions—provide asymmetric protection. A cap pays you if rates rise above a strike level; a floor pays if they fall below. You pay a premium upfront, but your downside is limited to that cost. This is useful when you want to hedge tail risk without giving up the benefit if rates move in your favor.

Example: You're running a carry trade, long Mexican peso against yen. You're worried the Bank of Mexico might cut rates sharply, collapsing your carry. You buy a cap on Mexican rates at 9.00%. If rates stay above 9%, the option expires worthless and you keep your carry. If rates plunge to 7%, the cap pays you the difference, cushioning the blow to your position.

How to Hedge Against Rising Rates in Forex Portfolios

Hedging isn't a one-size-fits-all process. Effective hedging starts with a clear understanding of your exposure, followed by selecting the right instruments and maintaining discipline in execution.

Author: Olivia Kensington;

Source: martinskikulis.com

Step 1: Quantify your exposure. Map out all positions with interest rate sensitivity. For each currency pair, calculate the net interest differential and the duration of your holding period. A six-month long position in AUD/JPY at 10 million notional with a 3% rate differential means you're exposed to roughly 150,000 in carry over that period—any rate change affects that number.

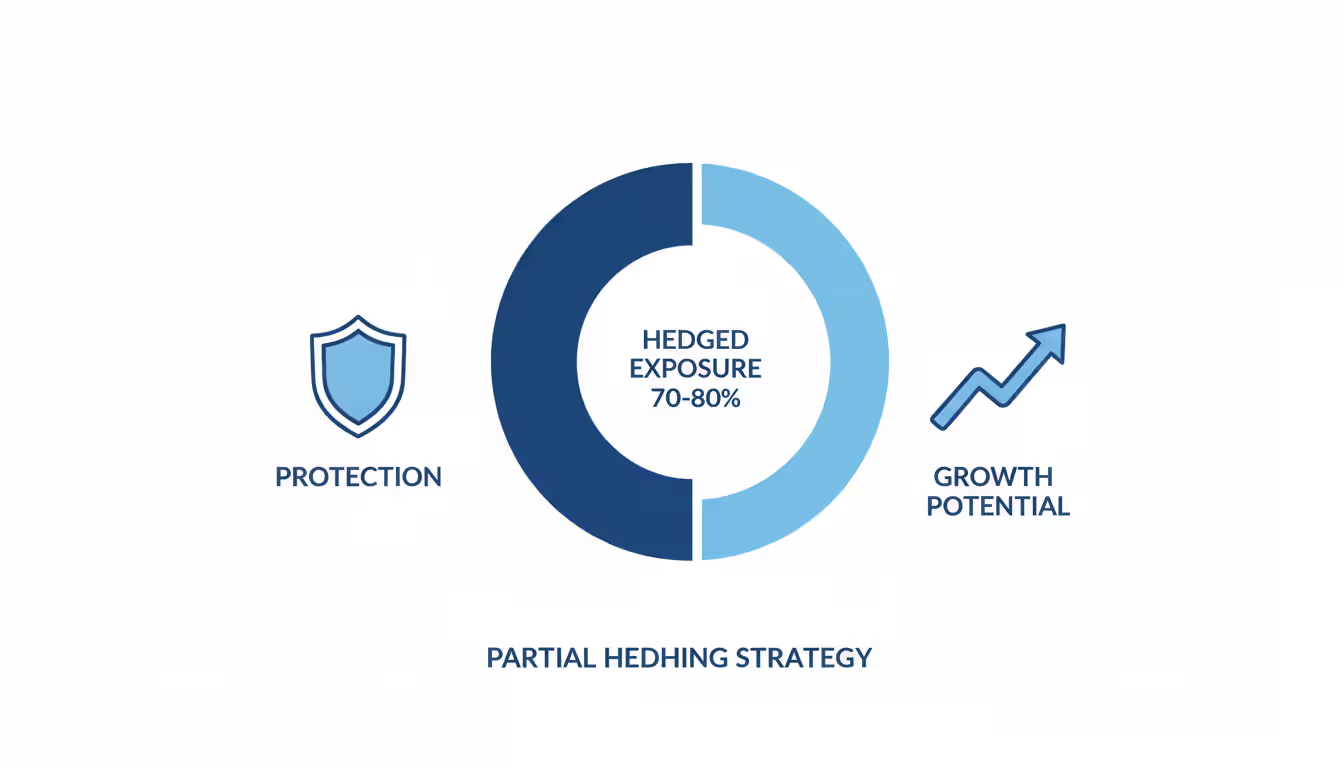

Step 2: Decide what to hedge. You don't have to hedge everything. Many traders hedge the bulk of their rate risk but leave some exposure to benefit from favorable moves. A common approach: hedge 70–80% of the notional, leaving 20–30% unhedged to capture upside if rates move in your favor.

Step 3: Choose your instruments. For short-term exposure (under three months), futures are often the most cost-effective. For longer horizons or large notionals, swaps offer better precision. If you're uncertain about the direction but want protection against extremes, options make sense despite the premium cost.

Step 4: Execute and document. Enter the hedge and record the rationale, notional, maturity, and expected offset. This isn't bureaucracy—it's risk management. Without documentation, you'll struggle to assess whether the hedge is working as intended or needs adjustment.

Step 5: Monitor and adjust. Interest rate expectations shift constantly. Central banks surprise markets, economic data changes forecasts, and yield curves steepen or flatten. Review your hedge monthly (or weekly for large positions). If your original forex position has been closed or reduced, unwind the corresponding hedge to avoid creating new speculative exposure.

Practical tip: Don't wait for a rate hike to start hedging. By the time the central bank moves, the market has usually priced it in and volatility spikes, making hedges more expensive. Hedge when volatility is low and the cost is reasonable, even if the rate move is months away.

Mistakes to Avoid When Hedging Interest Rate Risk

Over-hedging is the most common error. Traders, anxious about rate moves, hedge 120% or 150% of their exposure. Now they're not hedged—they're speculating in the opposite direction. If rates don't move as feared, the hedge loses money and drags down the entire position. Hedge only the exposure you actually have.

Ignoring basis risk happens when the hedge instrument doesn't match the underlying exposure. You might hedge euro rate risk with a swap tied to EURIBOR, but your forex broker charges swap fees based on a proprietary rate. The two won't move in lockstep, leaving a gap. Always confirm that the hedge's reference rate aligns with your actual cost or revenue stream.

Author: Olivia Kensington;

Source: martinskikulis.com

Poor timing is another pitfall. Some traders hedge after a rate move has already occurred, locking in a loss rather than preventing one. Others remove hedges prematurely when volatility drops, only to be caught by a surprise policy shift. Successful hedging requires patience and discipline—set criteria for when to enter and exit, and stick to them.

Neglecting cost-benefit analysis leads to expensive hedges that eat up more profit than the risk justifies. If you're running a small carry trade with 50 basis points of yield, paying 30 basis points annually to hedge makes little sense. Calculate the hedge cost as a percentage of expected return; if it's more than 20–30%, reconsider whether the trade is worth doing at all.

Finally, failing to stress-test your hedge under extreme scenarios can leave you exposed. Model what happens if rates move 100 or 200 basis points in a month—does your hedge still protect you, or are there gaps? Stress-testing reveals weaknesses before they cost you money.

Currency traders who fail to hedge interest rate exposure are effectively running two bets simultaneously—one on exchange rates, one on monetary policy—often without realizing it. Separating these risks through disciplined hedging is the hallmark of professional portfolio management

— Dr. Markus Brunnermeier

Frequently Asked Questions About Interest Rate Hedging

What is an interest rate hedge and how does it work?

An interest rate hedge is a financial position taken to offset potential losses from changes in interest rates. It works by establishing a second position whose value moves inversely to your primary exposure. For example, if you're long a high-yielding currency and rates fall, reducing your carry income, a hedge—such as an interest rate swap or futures contract—gains value to compensate for that loss. The hedge doesn't eliminate risk entirely but reduces your net exposure to rate fluctuations.

Why do currency traders need to hedge interest rate risk?

Currency values are heavily influenced by interest rate differentials between countries. When you hold a forex position, you're exposed to changes in those differentials. A surprise rate cut by the central bank of the currency you're long can trigger sharp depreciation, wiping out gains. Hedging allows you to focus on the currency trend itself without being blindsided by monetary policy shifts. It's especially important for carry trades, where the entire profit depends on maintaining a favorable rate spread.

What is the difference between fixed and floating rate risk in forex?

Fixed rate risk comes from positions where the interest rate or exchange rate is locked in for a future date, such as forward contracts or options. If market rates move after you lock in, you miss the opportunity to benefit from better pricing. Floating rate risk arises from positions that reprice continuously, like spot forex rolled overnight with swap charges. Floating exposure adjusts in real time but leaves you vulnerable to ongoing rate volatility. Both types require different hedging approaches—swaps and futures for floating, options or offsetting forwards for fixed.

How do interest rate swaps help manage rate exposure?

Interest rate swaps allow you to exchange fixed-rate payments for floating-rate payments (or vice versa) on a notional amount. If you're long a currency with floating funding costs and rates rise, your costs increase. By entering a swap where you receive floating and pay fixed, the rising floating payments from the swap offset your higher funding costs. Swaps are highly customizable, making them ideal for precise hedging of large or long-dated positions, though they require institutional access and legal agreements.

When should I hedge against rising interest rates?

Hedge when you have a clear, quantified exposure to rate moves and the cost of hedging is reasonable relative to your potential loss. Don't wait for a rate hike announcement—by then, the market has priced it in and hedge costs spike. Hedge proactively when volatility is low and you can lock in protection cheaply. Also hedge when your position size is large enough that a rate surprise would materially impact your capital. For small speculative trades, the hedge cost may outweigh the benefit.

What are the costs of hedging interest rate risk?

Hedging costs include the bid-offer spread on swaps or futures (typically 1–5 basis points), option premiums (0.5–2% of notional for caps or floors), and opportunity cost if rates move in your favor and the hedge becomes a drag. For exchange-traded futures, add commission fees. Swaps may require margin or collateral, tying up capital. The total cost varies by instrument, maturity, and market conditions, but expect to pay 10–50 basis points annually for a straightforward hedge. Weigh this against the potential loss from an unhedged position to determine if it's worthwhile.

Interest rate hedging isn't optional for serious currency traders—it's a core component of risk management. Exchange rates and interest rates move together, and ignoring one while trading the other is a recipe for unexpected losses. Whether you're running a carry trade, holding multi-month forward positions, or managing a diversified forex portfolio, rate risk is present and measurable.

The tools exist to manage that risk: swaps for precision and customization, futures for liquidity and transparency, options for asymmetric protection. Each has trade-offs in cost, complexity, and fit. The key is to match the hedge to your actual exposure, avoid over-hedging, and monitor positions as conditions evolve.

Start by quantifying your exposure. Calculate the interest differential on your positions, estimate the duration, and model what happens if central banks surprise the market. Then choose a hedge that fits your time horizon and budget. Hedging won't guarantee profits, but it will ensure that when you lose, it's because your currency view was wrong—not because you were blindsided by a rate move you could have protected against.

Unsystematic risk represents investment uncertainty tied to specific companies or assets rather than broad market forces. Unlike systematic risks affecting all securities, firm-specific risks can be substantially reduced through proper diversification across 20-30 uncorrelated positions

Markets don't just move—they accelerate, decelerate, and shift gears. Volatility risk is the danger that unexpected changes in price swing intensity will damage your positions. Unlike directional risk, it strikes when market pace changes, hurting options traders, currency speculators, and leveraged investors alike

Volatility clustering describes how large price changes tend to follow large changes, and calm periods extend—one of the most consistent patterns in financial markets. Understanding this phenomenon transforms risk management and trading strategy across forex, equities, and other assets

Systematic risk affects entire markets simultaneously—no diversification can eliminate it. Through concrete examples from interest rate changes to geopolitical events, understand how market-wide forces impact portfolios and learn practical measurement and management strategies using beta and asset allocation

The content on this website is provided for general informational and educational purposes only. It is intended to explain concepts related to Forex (FX) trading, currency markets, leverage, hedging, and risk management.

All information on this website, including articles, guides, and examples, is presented for general educational purposes. Forex trading carries significant risk, and outcomes may vary depending on market conditions, leverage, and individual decisions.

This website does not provide financial, investment, or trading advice, and the information presented should not be used as a substitute for consultation with qualified financial professionals.

The website and its authors are not responsible for any errors or omissions, or for any outcomes resulting from decisions made based on the information provided on this website.