Professional trader analyzing portfolio margin risk scenarios on multiple monitors with options P&L charts and stress test data in a modern trading office

Author: Marcus Ellington;Source: martinskikulis.com

Portfolio margin represents a sophisticated risk-based margining system that calculates your account's margin requirements by analyzing the potential risk across your entire portfolio rather than applying fixed percentages to individual positions. Unlike traditional margin frameworks, this approach can significantly reduce capital requirements for traders who maintain hedged or offsetting positions, freeing up buying power for additional strategies.

Understanding portfolio margin becomes essential as your trading evolves beyond simple directional bets. The system originated from the need to more accurately reflect actual market risk—a hedged position with limited downside shouldn't tie up the same capital as a naked exposure with unlimited risk. For sophisticated traders managing complex option spreads, multi-leg strategies, or diversified portfolios, this distinction translates directly into capital efficiency and strategic flexibility.

Portfolio Margin Explained

Portfolio margin operates on a risk-based methodology that stress-tests your entire account against hypothetical market scenarios. Rather than applying Regulation T's rules-based percentages—50% for stocks, fixed amounts for options—the system runs your positions through the Theoretical Intermarket Margin System (TIMS), which originated at the Options Clearing Corporation.

The core principle: your margin requirement should reflect your portfolio's actual worst-case loss under extreme but plausible market conditions. TIMS simulates price movements ranging from -15% to +15% (for equities) across multiple scenarios, including volatility changes. Your required margin equals the largest potential loss identified across these stress tests, plus a buffer.

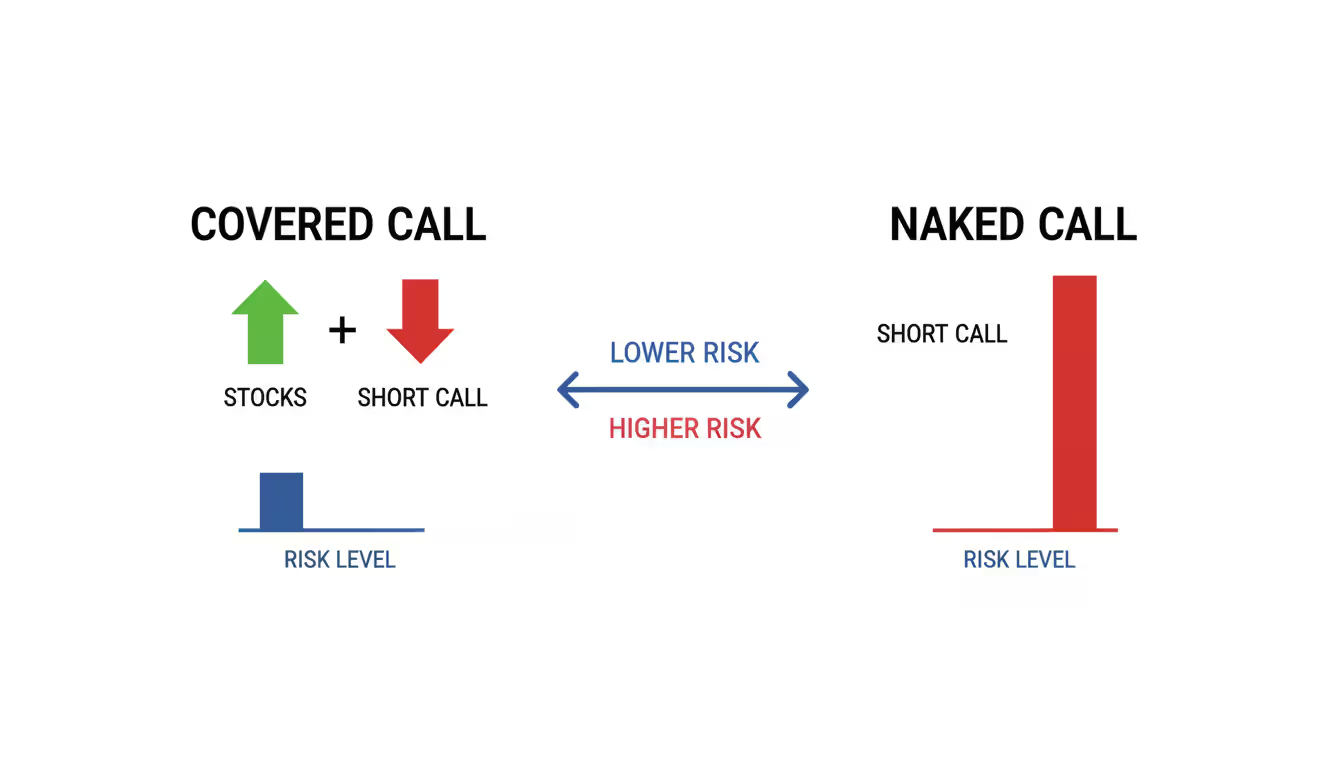

This matters because a covered call—long stock plus short call—faces fundamentally different risk than a naked call. Traditional margin treats them with separate, additive requirements. Portfolio margin recognizes the offsetting nature and charges margin based on the combined position's true exposure. A trader holding 1,000 shares of a $100 stock with 10 sold calls might see margin requirements drop from $50,000 (Reg T) to $15,000-$20,000 under portfolio margin, depending on strike prices and market conditions.

The system recalculates continuously as positions change and markets move. Your margin requirement isn't static—it fluctuates with implied volatility, time decay, and price movements. A position that required $10,000 margin yesterday might need $12,000 today if volatility spikes, even if you haven't traded.

Author: Marcus Ellington;

Source: martinskikulis.com

How Portfolio Margin Risk Calculation Works

Portfolio margin employs a Value-at-Risk (VaR) framework that projects potential losses across standardized stress scenarios. Your broker's system groups related positions—equities, options, and sometimes futures on the same underlying—then applies simultaneous price and volatility shocks.

For equity positions, the standard approach tests price movements in 10 scenarios: the underlying moving up or down by approximately 15%, 10%, and 5%, combined with volatility expanding or contracting. Each scenario generates a theoretical portfolio value. The scenario producing the largest loss determines your margin requirement for that group of positions.

Consider a practical example: You're long 500 shares of XYZ at $80 and long 5 put contracts at the $75 strike. Under Reg T, you'd need $20,000 margin for the stock (50% of $40,000) plus the put premium you paid. Portfolio margin sees a protected position with maximum loss capped at $2,500 (500 shares × $5 decline from $80 to $75, minus put value gains). After stress-testing, your margin requirement might settle around $3,000-$4,000—substantially less than $20,000.

The calculation becomes more nuanced with options. The system considers:

Delta exposure: How much your portfolio moves with the underlying

Gamma risk: How delta changes as prices move

Vega sensitivity: Impact of volatility shifts

Theta decay: Time value erosion

A short iron condor in SPY might show minimal margin requirements because all four legs offset each other, capping maximum loss to the distance between strikes minus net credit. The stress test confirms this limited risk, charging margin accordingly. Contrast this with Reg T, which might treat each short option leg separately, multiplying requirements unnecessarily.

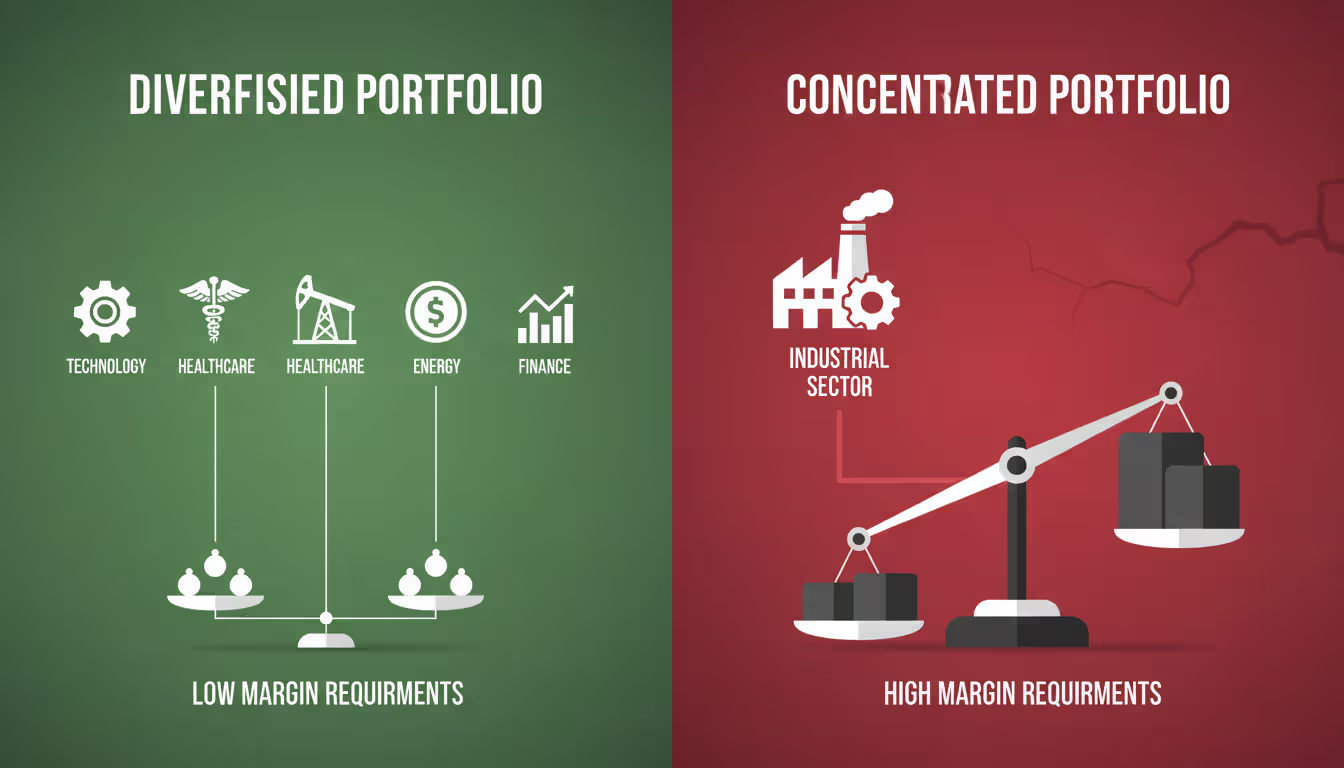

Concentration matters significantly. A portfolio with 80% exposure to one sector will show higher margin requirements than a diversified portfolio with identical dollar value, because sector-specific scenarios generate larger potential losses. The system penalizes concentration risk automatically.

Portfolio Margin vs Reg T Margin

The fundamental difference between these frameworks lies in their philosophical approach to risk measurement. Regulation T applies standardized rules established in 1974, designed for simplicity and broad applicability. Portfolio margin, approved for retail use in 2007, embraces complexity to achieve precision.

Reg T assigns fixed percentages: 50% for long stock, 30% for short stock, and formula-based calculations for options that often ignore hedging benefits. A bull put spread—limited risk by design—still requires margin calculated on the short put as if it stood alone, only partially offset by the long put's value.

Portfolio margin evaluates the actual risk profile. That same bull put spread gets analyzed as a unit. If the spread is $5 wide and you collected $1.50 credit, your maximum loss is $3.50 per share. Portfolio margin charges based on this $350 maximum loss (per contract), not on theoretical naked put exposure that could never materialize given your hedge.

Feature

Portfolio Margin

Reg T Margin

Calculation Method

Risk-based stress testing across portfolio

Rules-based fixed percentages per position

Minimum Equity Requirement

$125,000 (initially); $100,000 (maintenance)

$2,000 standard; $25,000 for pattern day trading

Typical Buying Power Increase

3-6× for hedged strategies; minimal for naked positions

Standard 2:1 for stocks; varies for options

Margin Call Triggers

Portfolio loss exceeds risk-based threshold

Position value drops below fixed percentage

Best Suited For

Sophisticated traders using spreads, hedges, and multi-leg strategies

Beginning to intermediate traders; simple directional positions

Regulatory Framework

FINRA Rule 4210(g); exchange-specific rules

Federal Reserve Regulation T

The buying power difference proves dramatic for options traders. A portfolio of short vertical spreads might require 15-25% of notional value under portfolio margin versus 40-60% under Reg T. This isn't "free money"—it reflects accurate risk measurement. Your actual risk hasn't changed; the margin system finally recognizes it properly.

One critical trade-off: portfolio margin can trigger faster margin calls during volatile markets. Because requirements adjust dynamically, a volatility spike might increase your margin needs by 30-50% overnight, even without trading. Reg T requirements stay relatively stable unless you change positions. Traders accustomed to predictable margin usage face adjustment challenges.

Eligibility Requirements for Portfolio Margin Accounts

Brokers enforce strict thresholds before granting portfolio margin approval. The baseline requirement: $125,000 in account equity at the time of application, though you can maintain the account with $100,000 minimum. These figures represent regulatory minimums; individual brokers often set higher standards—$150,000 or $175,000 isn't uncommon.

Beyond capital requirements, brokers assess trading experience and sophistication. Expect questions about:

Years actively trading options

Familiarity with multi-leg strategies

Understanding of margin mechanics and liquidation risk

Most brokers require existing options approval at the highest level (typically "Level 4" or "Level 5"), permitting naked options and complex spreads. You can't jump directly to portfolio margin as a novice—it's a graduated privilege.

Account type matters. Portfolio margin applies only to margin accounts; IRAs generally don't qualify due to regulatory restrictions on certain strategies. Some brokers offer limited portfolio margin for IRAs on defined-risk spreads, but full portfolio margin remains restricted to taxable accounts.

Regulatory oversight adds another layer. Your broker must ensure you understand the risks, particularly accelerated liquidation during volatile markets. Some firms require a phone conversation with a margin specialist or completion of an educational module before approval.

Account Setup and Application Process

The application process typically unfolds over several days. You'll start by completing a portfolio margin agreement through your broker's platform, acknowledging specific risks including dynamic margin requirements and potential rapid liquidation.

Documentation requirements include:

Current account statements proving minimum equity

Trading history demonstrating options experience

Sometimes: net worth verification or income documentation

Signed risk disclosure forms specific to portfolio margin

After submission, the broker's margin department reviews your profile. They're evaluating whether you can handle volatile margin swings and understand the system's mechanics. Approval isn't automatic even if you meet numerical thresholds—brokers maintain discretion to decline applications.

Timeline varies by broker: 2-5 business days for straightforward approvals, longer if the margin team requests additional information or documentation. Some brokers offer provisional approval, monitoring your early portfolio margin usage closely before granting permanent status.

Once approved, the transition happens immediately. Your existing positions get recalculated under portfolio margin rules. Most traders see margin requirements drop significantly, freeing up buying power. However, concentrated or naked positions might show increased requirements—the system penalizes unhedged risk that Reg T's blunt calculations missed.

Benefits and Risks of Using Portfolio Margin

The primary advantage centers on capital efficiency. Traders employing defined-risk strategies can deploy the same capital across more positions, potentially enhancing returns without increasing actual risk. A trader with $200,000 who previously maintained 10 iron condors under Reg T might manage 25-30 under portfolio margin, assuming consistent risk per trade.

This efficiency compounds for sophisticated strategies. Calendar spreads, butterflies, and ratio spreads all benefit from margin calculations that recognize their limited risk profiles. A trader selling premium through multiple small positions across various underlyings can diversify more effectively when each position requires less capital.

Margin reduction with portfolio margin proves especially powerful for hedged equity positions. Long stock protected by puts, covered calls, or collars all show substantially lower requirements than naked stock positions. An investor holding $500,000 in equities with protective puts might reduce margin needs from $250,000 (Reg T) to $75,000-$100,000, freeing $150,000-$175,000 for additional investments.

Author: Marcus Ellington;

Source: martinskikulis.com

The system rewards portfolio diversification. Unlike Reg T's position-by-position approach, portfolio margin recognizes that losses in one sector might offset gains elsewhere. A balanced portfolio spanning technology, healthcare, energy, and financials shows lower margin requirements than concentrated exposure—the stress tests reveal reduced worst-case scenarios.

However, risks intensify in several ways:

Dynamic margin requirements create unpredictability. A market event that spikes volatility can double your margin needs within hours. The 2020 pandemic volatility surge saw some traders facing 100-150% margin increases overnight. If you're fully deployed, you'll face margin calls despite not trading.

Liquidation happens faster and more aggressively. Brokers don't wait politely when portfolio margin accounts approach minimums. They'll liquidate positions rapidly, often starting with the most liquid holdings rather than the positions you'd prefer to close. This forced liquidation frequently occurs at unfavorable prices during volatile markets.

Complexity breeds mistakes. Traders accustomed to predictable Reg T calculations sometimes misunderstand their actual risk exposure. Adding a position that seems innocuous might trigger substantial margin increases if it concentrates risk or removes offsetting exposure.

The buying power increase tempts overtrading. Just because you can manage 30 positions doesn't mean you should. Transaction costs, monitoring burden, and execution risk all scale with position count. Some traders, intoxicated by increased buying power, over-deploy capital and face catastrophic losses when markets move against them.

Portfolio Margin and Options Strategies

Options traders gain the most substantial benefits from portfolio margin. The system's risk-based approach finally accounts for the mathematical limits inherent in spreads, condors, butterflies, and other defined-risk structures.

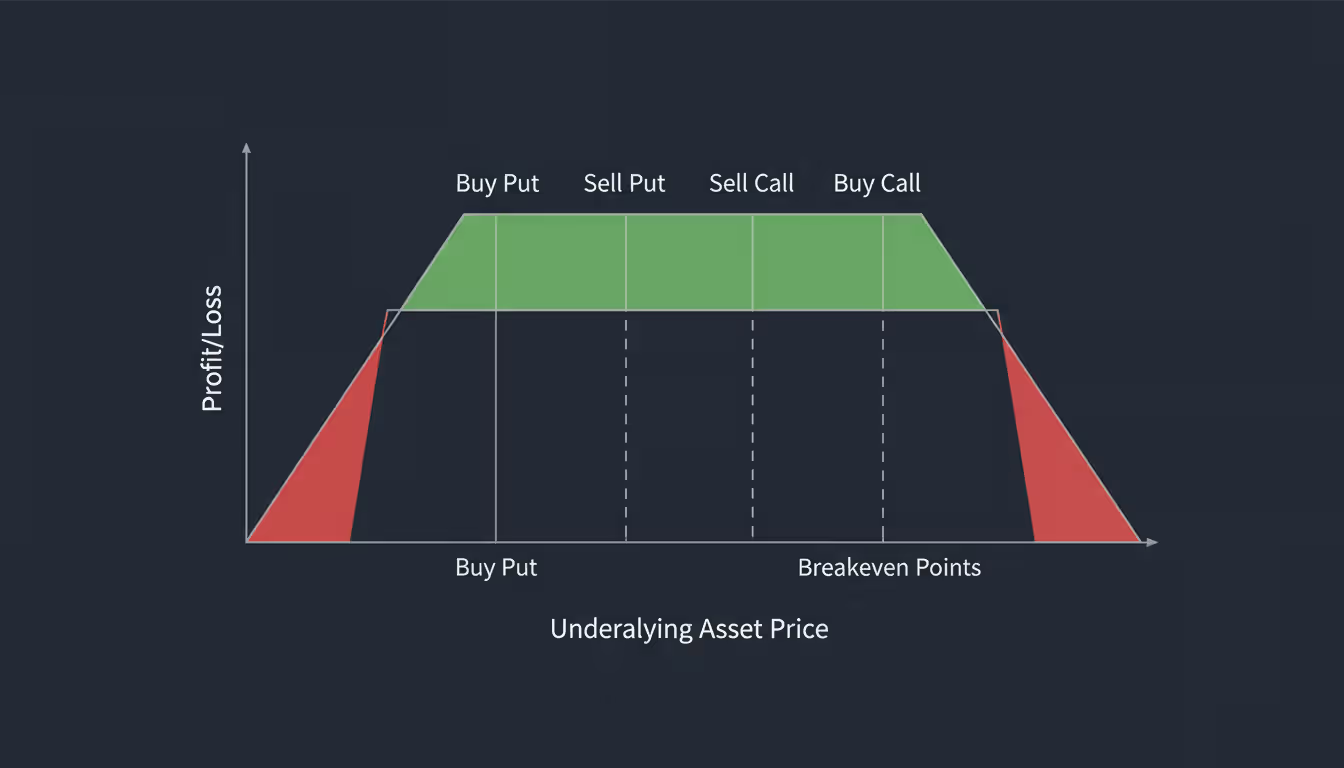

Consider a short iron condor: sell the $95 put, buy the $90 put, sell the $105 call, buy the $110 call on a $100 stock. Maximum loss is $500 per contract (the $5 spread width minus credit received). Under Reg T, margin requirements might reach $1,000-$1,500 per contract because the system partially treats each short leg independently. Portfolio margin recognizes the $500 maximum loss and charges accordingly—typically $500-$700 per contract, reflecting the actual risk plus buffer.

This efficiency scales beautifully. A trader managing 50 iron condors across different underlyings might need $75,000 margin under portfolio margin versus $150,000+ under Reg T. The capital savings enable either increased diversification or reduced account size requirements.

Author: Marcus Ellington;

Source: martinskikulis.com

Vertical spreads—bull puts, bear calls, credit spreads, debit spreads—all benefit similarly. A $5-wide credit spread might require $500 margin (the maximum loss) rather than $1,000-$2,000 under Reg T. This 50-70% reduction in capital requirements directly improves return on capital for consistently profitable traders.

Calendar spreads and diagonal spreads show even more dramatic improvements. These strategies involve buying longer-dated options and selling shorter-dated options at different strikes. The offsetting nature—long and short options on the same underlying—results in minimal margin under portfolio margin, often just 10-20% of the notional value. Reg T calculations, treating each leg more independently, charge substantially more.

One underappreciated benefit: portfolio margin enables more sophisticated hedging. A trader long 1,000 shares might sell out-of-the-money calls and buy out-of-the-money puts, creating a collar. Portfolio margin recognizes this three-legged structure as a unit with defined risk parameters, charging minimal margin. Under Reg T, the calculations treat components separately, requiring more capital for equivalent protection.

The system does penalize truly risky options positions. Naked calls—unlimited risk—show higher margin requirements under portfolio margin than traders expect, sometimes exceeding Reg T. The stress tests identify the theoretically unlimited loss potential and charge accordingly. Portfolio margin isn't a free pass for dangerous strategies; it's a precision tool that rewards defined risk and punishes undefined risk.

Is Portfolio Margin Right for Your Trading Strategy?

Portfolio margin suits traders who consistently employ defined-risk strategies across multiple positions. If your typical approach involves iron condors, vertical spreads, butterflies, or hedged equity positions, the capital efficiency gains justify the complexity and risks.

Traders managing $150,000-$300,000 in capital often find portfolio margin transformative. This range provides sufficient buffer above the $100,000 minimum to weather volatility-driven margin increases while being small enough that capital efficiency materially impacts strategy implementation. You can diversify more effectively or reduce the capital committed to trading.

Risk comes from not knowing what you're doing

— Warren Buffett

Active options sellers benefit disproportionately. If you're selling premium through multiple small positions, the margin reduction per position compounds across your portfolio. A trader maintaining 20-40 concurrent positions might free up 40-60% of previously required capital.

However, portfolio margin proves inappropriate for several trader profiles:

Directional traders using simple long stock or long options positions gain minimal benefit. If you're buying calls or puts without offsetting positions, portfolio margin offers little advantage—you're paying premium, not posting margin. Long stock positions show modest margin reduction, but not enough to justify the complexity.

Traders near the $125,000 minimum face dangerous exposure. A 20% market decline combined with volatility spike could push margin requirements above your account value, triggering forced liquidation at the worst possible time. You need substantial buffer—ideally $175,000+ in equity—to safely handle dynamic margin swings.

Part-time traders who can't monitor positions continuously risk catastrophic margin calls. The dynamic nature of portfolio margin means requirements change throughout the day. If you check your account once daily, you might miss margin warnings until it's too late.

Traders uncomfortable with forced liquidation should avoid portfolio margin. Brokers will close positions aggressively and without consultation when accounts approach minimum requirements. If you prefer controlling exit timing and selection, the risk of automated liquidation outweighs capital efficiency benefits.

Consider your trading psychology honestly. Does increased buying power tempt you toward overtrading? Do you struggle with position sizing discipline? Portfolio margin amplifies both gains and losses through leverage—it's a tool that rewards discipline and punishes impulsiveness.

A practical middle ground: apply for portfolio margin but don't maximize buying power usage. If portfolio margin calculations show you could deploy $400,000 in positions, consider limiting yourself to $250,000-$300,000. This approach captures capital efficiency benefits while maintaining substantial safety buffer for volatility-driven margin increases.

Frequently Asked Questions About Portfolio Margin

What is the minimum account size for portfolio margin?

You need $125,000 in equity to open a portfolio margin account, though the maintenance requirement drops to $100,000 once approved. Individual brokers often set higher minimums—$150,000 or $175,000. Practically, you should maintain $175,000+ to handle volatility-driven margin increases without forced liquidation risk. Approaching the minimum too closely leaves insufficient buffer when market stress increases requirements by 30-50% overnight.

How much buying power does portfolio margin provide?

The increase varies dramatically based on your strategy. Traders using defined-risk spreads, iron condors, and hedged positions typically see 3-6× buying power compared to Reg T margin. A portfolio of vertical spreads might require only 15-20% of the capital needed under Reg T. However, naked positions or simple long stock show minimal improvement—portfolio margin isn't magic, it's precision. Concentrated portfolios gain less than diversified ones because stress testing reveals higher risk.

Can I use portfolio margin for stock trading only?

Yes, but benefits prove modest. Long stock positions under portfolio margin require roughly 15-20% margin for diversified holdings versus 50% under Reg T. A $100,000 equity position might need $15,000-$20,000 margin instead of $50,000. However, you'll face dynamic requirements—that $15,000 could jump to $25,000 during volatility spikes. Most traders find portfolio margin most valuable when combining equities with options for hedging, not for stock-only portfolios.

What happens during a margin call with portfolio margin?

Margin calls under portfolio margin are faster and less forgiving than Reg T. When your account equity drops below required margin, brokers typically provide minimal time—sometimes just hours—to deposit funds or reduce positions. If you don't act quickly enough, the broker will liquidate positions automatically, usually starting with the most liquid holdings regardless of your preferences. During extreme volatility, liquidation might occur immediately without warning. This aggressive approach reflects the dynamic nature of portfolio margin—risk can escalate rapidly, requiring immediate action.

Is portfolio margin available at all brokers?

No. Major brokers like Interactive Brokers, TD Ameritrade (now Charles Schwab), E*TRADE, and Fidelity offer portfolio margin, but many smaller brokers don't. The infrastructure required to calculate real-time risk-based margin across thousands of accounts is substantial. Some brokers restrict portfolio margin to their most active clients or those meeting enhanced criteria beyond regulatory minimums. Before assuming access, verify your broker's specific portfolio margin policies, minimum requirements, and approval process.

How does portfolio margin affect options trading strategies?

Portfolio margin transforms options trading by recognizing the mathematical risk limits in spreads and hedged positions. A short vertical spread with $500 maximum loss might require $500-$700 margin instead of $1,500+ under Reg T. Iron condors, butterflies, calendars, and other multi-leg strategies all show 40-70% margin reductions. This efficiency enables greater diversification—managing 30 small positions instead of 10 large ones—or reduces capital requirements for equivalent exposure. However, the system penalizes naked options and undefined-risk strategies with higher margin than traders expect, reflecting actual unlimited loss potential.

Portfolio margin represents a powerful tool for sophisticated traders who understand both its capital efficiency benefits and its amplified risks. By calculating margin requirements based on actual portfolio-wide risk rather than arbitrary position-by-position rules, the system enables traders to deploy capital more effectively across hedged and defined-risk strategies.

The advantages prove most compelling for options traders managing multiple spread positions, hedged equity portfolios, or diversified books of defined-risk trades. Capital requirements often drop by 40-70% compared to Regulation T, freeing resources for additional diversification or reducing the total capital needed to implement your strategy.

However, these benefits come with meaningful trade-offs. Dynamic margin requirements fluctuate with market volatility, potentially doubling overnight during stress periods. Forced liquidation happens faster and more aggressively than under Reg T. The complexity demands continuous monitoring and deep understanding of how positions interact to affect overall risk calculations.

Success with portfolio margin requires discipline, substantial capital buffer above minimums, and honest assessment of your ability to handle volatile margin swings. Traders who maximize buying power usage or operate near minimum requirements face elevated risk of catastrophic margin calls during market turbulence.

For the right trader—experienced, well-capitalized, focused on defined-risk strategies, and capable of active monitoring—portfolio margin unlocks meaningful capital efficiency. For others, the complexity and dynamic risk outweigh the benefits. The decision ultimately depends not just on meeting eligibility requirements, but on whether your trading approach, capital base, and risk management discipline align with portfolio margin's unique characteristics.

Unsystematic risk represents investment uncertainty tied to specific companies or assets rather than broad market forces. Unlike systematic risks affecting all securities, firm-specific risks can be substantially reduced through proper diversification across 20-30 uncorrelated positions

Markets don't just move—they accelerate, decelerate, and shift gears. Volatility risk is the danger that unexpected changes in price swing intensity will damage your positions. Unlike directional risk, it strikes when market pace changes, hurting options traders, currency speculators, and leveraged investors alike

Volatility clustering describes how large price changes tend to follow large changes, and calm periods extend—one of the most consistent patterns in financial markets. Understanding this phenomenon transforms risk management and trading strategy across forex, equities, and other assets

Systematic risk affects entire markets simultaneously—no diversification can eliminate it. Through concrete examples from interest rate changes to geopolitical events, understand how market-wide forces impact portfolios and learn practical measurement and management strategies using beta and asset allocation

The content on this website is provided for general informational and educational purposes only. It is intended to explain concepts related to Forex (FX) trading, currency markets, leverage, hedging, and risk management.

All information on this website, including articles, guides, and examples, is presented for general educational purposes. Forex trading carries significant risk, and outcomes may vary depending on market conditions, leverage, and individual decisions.

This website does not provide financial, investment, or trading advice, and the information presented should not be used as a substitute for consultation with qualified financial professionals.

The website and its authors are not responsible for any errors or omissions, or for any outcomes resulting from decisions made based on the information provided on this website.