Panoramic view of a global financial district with glowing digital currency streams flowing between bank skyscrapers at dusk, symbolizing cross-border settlement flows

When two parties agree to trade currencies, securities, or other financial instruments, they create an obligation: one side delivers cash, the other delivers the asset. Settlement risk emerges in the gap between these two legs of the transaction. If one counterparty fulfills its obligation but the other defaults before reciprocating, the performing party loses both the asset it delivered and the payment it expected to receive.

This risk is not theoretical. Banks, asset managers, hedge funds, and corporations encounter settlement exposure daily, especially in foreign exchange markets where trillions of dollars change hands across borders and time zones. Understanding how settlement risk arises, how it differs from related concepts like credit risk, and which tools exist to contain it has become essential for anyone involved in cross-border finance.

Understanding Settlement Risk in Financial Markets

Settlement risk is the danger that one party in a financial transaction will deliver cash or securities as agreed, but the counterparty will fail to deliver its side of the bargain. The risk crystallizes during the settlement window—the period between when the first leg of a trade is executed and when the second leg completes.

Trades do not settle instantaneously. A typical FX spot transaction agreed on Monday might settle on Wednesday (T+2). During those two days, market prices move, and counterparty credit conditions can deteriorate. But the true settlement risk window is narrower and more acute: it spans the hours or minutes when one party has already made an irrevocable payment but has not yet received the offsetting currency or asset.

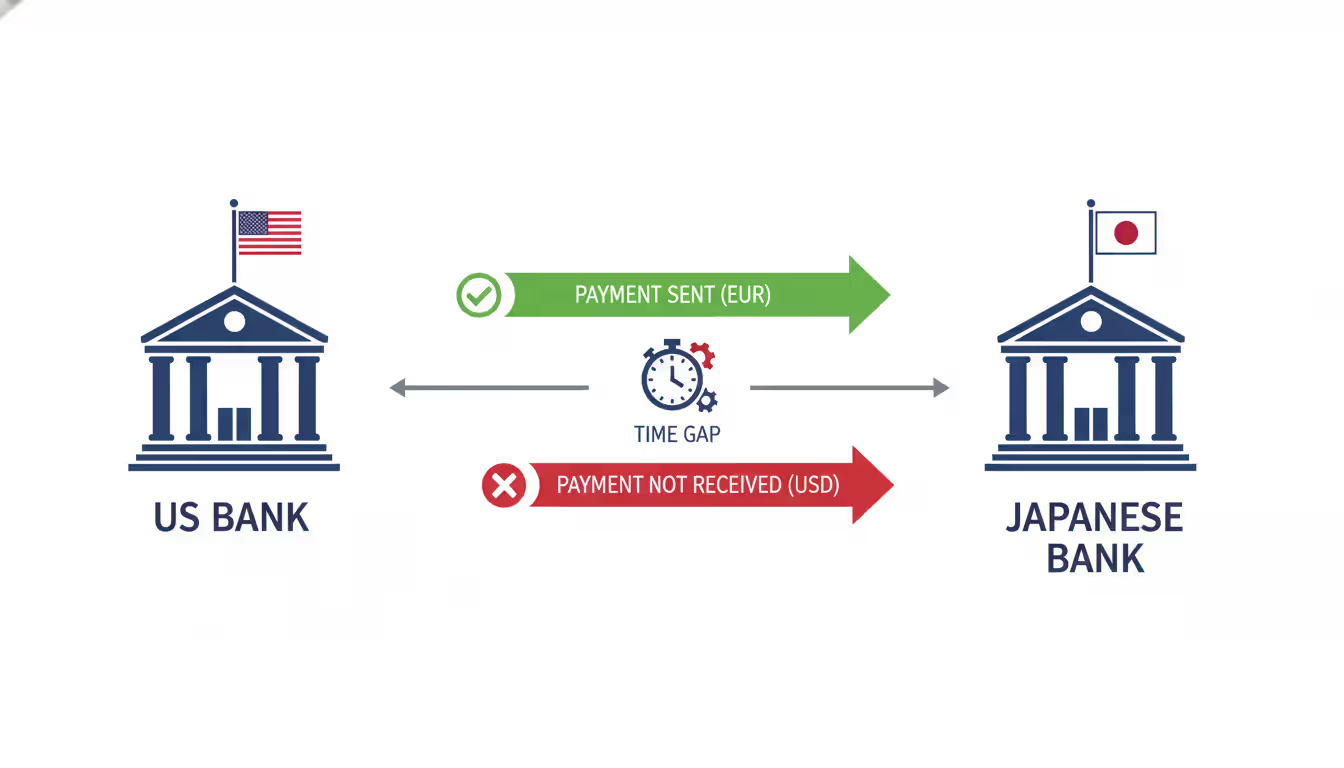

The mechanics are straightforward. Suppose a New York bank sells euros and buys U.S. dollars from a Tokyo bank. The New York bank instructs its European correspondent to transfer euros to the Tokyo bank's account. Once that transfer becomes final, the New York bank has no way to reverse it. If the Tokyo bank then fails before sending dollars, the New York bank has lost the full euro amount. It holds neither euros nor dollars.

Author: Olivia Kensington;

Source: martinskikulis.com

Settlement risk differs from pre-settlement risk, which covers the period between trade execution and the start of settlement. Pre-settlement exposure is typically limited to the change in market value of the contract—if a counterparty defaults before settlement, the non-defaulting party can replace the trade at current market prices and claim the difference. Settlement risk, by contrast, involves principal exposure: the full notional value of the transaction is at stake.

Herstatt Risk and the Origins of Settlement Concern

The term "Herstatt risk" honors—if that is the right word—Bankhaus Herstatt, a mid-sized German bank that collapsed on June 26, 1974. The bank had sold Deutsche marks and purchased U.S. dollars in the foreign exchange market. Its counterparties in New York had already paid dollars into Herstatt's U.S. accounts when German regulators withdrew the bank's license and ordered it into liquidation at 3:30 p.m. Central European Time.

That was 10:30 a.m. in New York, before Herstatt's U.S. accounts could disburse the corresponding Deutsche mark payments. Herstatt's counterparties found themselves out of pocket for the full dollar amounts they had paid, with no immediate prospect of recovering the marks they were owed. The losses were substantial, and the event sent shockwaves through global payment systems.

Author: Olivia Kensington;

Source: martinskikulis.com

Herstatt's failure exposed a fundamental flaw in cross-border settlement: currencies settle in different jurisdictions, on different payment systems, at different times of day. A bank in Asia might irrevocably pay yen during Tokyo business hours, only to discover hours later—when New York opens—that its U.S. dollar counterpart has failed. The time-zone gap creates a window of vulnerability that can span an entire business day.

The 1974 collapse prompted central banks to examine settlement infrastructure more closely. The Bank for International Settlements convened the Committee on Payment and Settlement Systems, which eventually led to the creation of mechanisms designed to close the Herstatt gap. But the risk itself remains inherent to any system where final payments occur at different times.

How Settlement Risk Arises in Forex Transactions

Foreign exchange markets generate the largest settlement exposures in global finance. Daily FX turnover exceeds $7 trillion, and the vast majority of that volume involves spot, forward, and swap transactions that require delivery of one currency against another.

Settlement risk in FX arises because each currency in a pair settles through its own domestic payment system. U.S. dollars clear through Fedwire or CHIPS in New York. Euros settle via TARGET2 in the eurozone. Yen move through the Bank of Japan's systems in Tokyo. Sterling clears in London through CHAPS. These systems operate in different time zones and follow different schedules.

Consider a euro/dollar transaction. The euro leg typically settles early in the European day, while the dollar leg settles during New York hours. If a European bank sends euros at 9:00 a.m. Frankfurt time (3:00 a.m. New York time), it will not know whether it will receive dollars until the U.S. payment system opens and processes the counterparty's instruction—potentially six hours later. During that window, the European bank has full principal exposure.

The risk is not symmetrical. The party that pays first bears the entire notional amount at risk. The party that pays second has no settlement risk at all, because it can simply refuse to pay if it learns that its counterparty has failed. This asymmetry creates an incentive to delay payment as long as possible, which can lead to gridlock if all participants adopt the same strategy.

Certain currency pairs and trade structures amplify the exposure. Exotic currency pairs that settle in emerging-market time zones can create extended windows when one leg has settled but the other jurisdiction's payment system is closed. Long-dated forwards and non-deliverable forwards introduce additional complexity, although the settlement risk window itself remains concentrated around the value date.

Counterparty Settlement Risk Explained

Counterparty settlement risk is the exposure to a specific counterparty's failure during the settlement process. It combines two elements: the probability that the counterparty will default, and the loss given default if that failure occurs during the settlement window.

The distinction between pre-settlement and settlement-stage exposure matters. Pre-settlement exposure is a mark-to-market concept. If a counterparty defaults before settlement, the non-defaulting party replaces the trade and recovers the market value difference. The loss is limited to the unrealized gain on the contract.

Settlement exposure, by contrast, is a principal-at-risk concept. Once payment is made, the full notional is at risk until the offsetting payment arrives. If the counterparty defaults after receiving payment but before reciprocating, the loss equals the entire principal amount, not merely the market value change.

The timing is critical. A counterparty might be solvent when a trade is executed, remain solvent throughout the pre-settlement period, and then fail precisely during the few hours when settlement is underway. Regulators and risk managers sometimes refer to this as "wrong-way risk"—the possibility that counterparty creditworthiness deteriorates just as exposure peaks.

Banks manage counterparty settlement risk through credit limits, but those limits must account for the concentration of exposure during settlement windows. A bank might have dozens or hundreds of FX trades with a single counterparty settling on the same day, creating a brief but massive peak in exposure that far exceeds the pre-settlement exposure measured by value-at-risk models.

Settlement Risk vs Credit Risk

Settlement risk is a species of credit risk, but the two concepts differ in important ways. Credit risk broadly describes the danger that a borrower or counterparty will fail to meet its obligations. Settlement risk is the subset of credit risk that arises specifically during the settlement of a financial transaction.

The timing distinction is the most obvious difference. Credit risk on a loan extends over months or years. Pre-settlement credit risk on a derivative lasts from trade date to maturity. Settlement risk compresses into hours or, at most, a few days. The brevity does not make it less dangerous; in fact, the short duration and high principal amounts can make settlement risk more acute than other forms of credit exposure.

Recovery prospects also differ. When a borrower defaults on a loan, creditors enter a bankruptcy or restructuring process and eventually recover some portion of the claim. Recovery rates on senior unsecured bank debt have historically averaged 40–60 percent. Settlement risk, however, often results in total loss. The defaulting party has received the asset or cash but provided nothing in return. The non-defaulting party holds an unsecured claim in a bankruptcy proceeding, with no collateral and no guarantee of recovery.

Risk measurement approaches diverge as well. Credit risk models estimate probability of default over a time horizon, loss given default, and exposure at default, then combine these into an expected loss figure. Settlement risk models focus on peak intraday exposure, the timing of payment flows, and the operational controls that govern when payments become irrevocable. The probability of default during a single settlement window is low, but the loss given default is 100 percent of the notional amount.

Regulatory capital requirements reflect these differences. Under Basel III, banks must hold capital against credit valuation adjustment risk and counterparty credit risk on derivatives, but settlement risk receives separate treatment. Exposures that remain unsettled beyond a standard settlement period attract higher capital charges, incentivizing banks to settle promptly and use risk-mitigation mechanisms.

Risk Type

Definition

Timing of Loss

Typical Duration

Mitigation Tools

Measurement Approach

Settlement Risk

Loss if counterparty defaults after receiving payment but before delivering the offsetting asset

During settlement window

Hours to 2 days

CLS, DVP, netting, PvP

Peak intraday exposure, notional principal at risk

Cash flow forecasting, liquidity coverage ratio, net stable funding ratio

Methods for Reducing Settlement Exposure

Financial institutions and market infrastructure providers have developed several mechanisms to reduce settlement risk. None eliminates the risk entirely, but each narrows the window of exposure or reduces the amount at stake.

Delivery versus payment (DVP) links the transfer of securities to the transfer of cash, ensuring that one occurs if and only if the other does. DVP systems are standard in securities markets. When a buyer purchases a bond, the securities depository does not release the bond to the buyer's account until it confirms receipt of cash in the seller's account. The two legs settle simultaneously, or the trade does not settle at all. DVP eliminates principal risk, though it does not eliminate liquidity risk—if one party cannot fund its side of the trade, settlement fails, but neither party loses principal.

Payment versus payment (PvP) applies the same logic to foreign exchange. In a PvP system, the final transfer of one currency occurs if and only if the final transfer of the other currency occurs. CLS Bank, discussed below, is the most prominent PvP mechanism in FX markets.

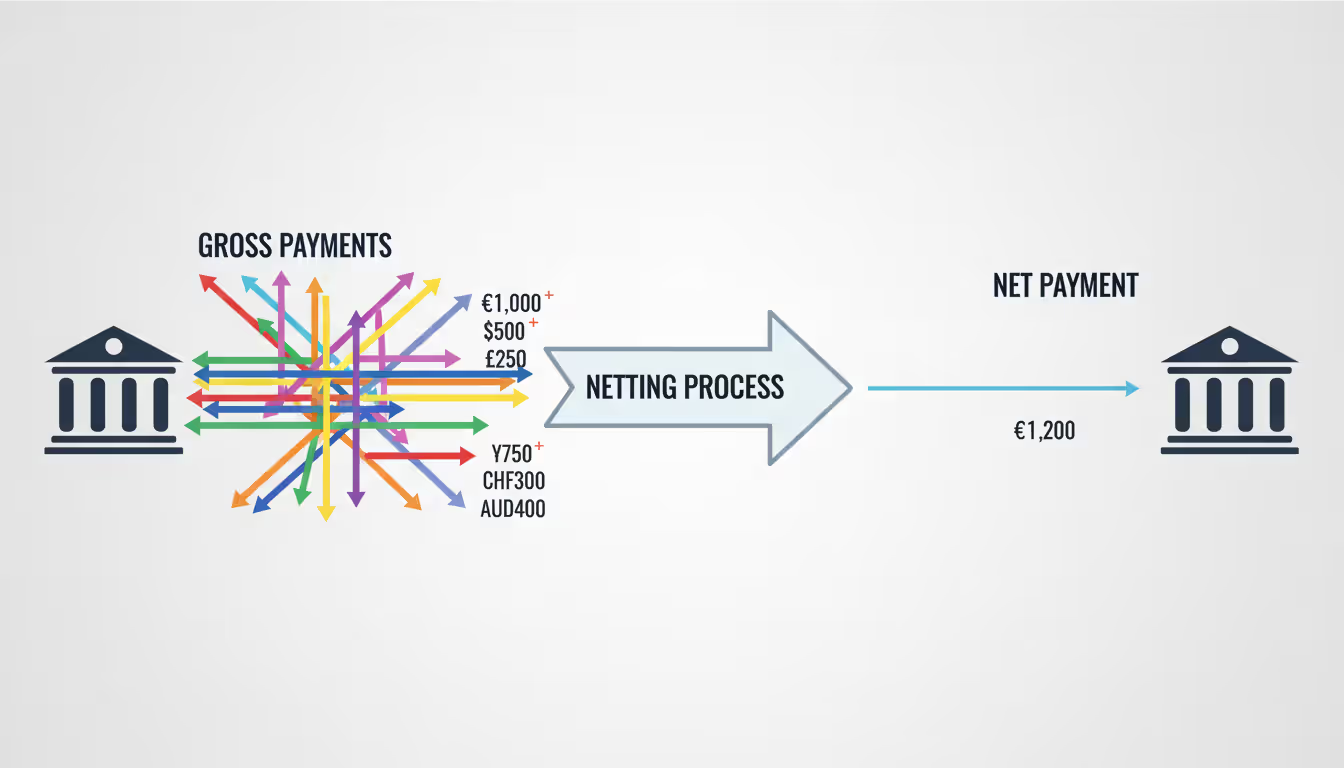

Settlement netting reduces gross settlement obligations to a single net amount. If two banks have multiple trades with each other settling on the same day, netting calculates the net amount owed in each currency and settles only that net figure. For example, if Bank A owes Bank B $100 million and €80 million, while Bank B owes Bank A $90 million and €85 million, netting reduces the settlements to a single $10 million payment from A to B and a single €5 million payment from B to A. This reduces both settlement risk and liquidity demands.

Netting can be bilateral or multilateral. Bilateral netting applies between two counterparties. Multilateral netting, used by central counterparties and systems like CLS, calculates net positions across all participants, further compressing settlement volumes.

Author: Olivia Kensington;

Source: martinskikulis.com

Collateral arrangements require one or both parties to post assets that can be seized if settlement fails. Variation margin on centrally cleared derivatives and initial margin on uncleared swaps are examples. While collateral does not prevent settlement risk, it provides a recovery mechanism that reduces loss given default.

Bilateral risk limits cap the settlement exposure a bank is willing to accept with any single counterparty. Limits are typically set as a percentage of the counterparty's capital or credit rating and are monitored intraday. If a counterparty approaches its limit, the bank stops accepting new trades or requires the counterparty to settle existing trades before adding new ones.

How CLS Bank Mitigates Settlement Risk

CLS Bank International, established in 2002, is the most significant infrastructure innovation for managing FX settlement risk. CLS operates a PvP settlement system for foreign exchange transactions, eliminating Herstatt risk for the currencies and participants within its network.

CLS settles 18 currencies, including all the major currencies (U.S. dollar, euro, yen, pound sterling, Swiss franc, Canadian dollar, Australian dollar) and several emerging-market currencies. Member banks submit their FX trades to CLS, which calculates each bank's net position in each currency for the settlement day.

Settlement occurs during a five-hour window that overlaps the operating hours of all relevant real-time gross settlement systems. CLS maintains accounts at each central bank for the currencies it settles. Member banks fund their net pay-in positions in each currency at the start of the window. CLS then makes simultaneous pay-ins and pay-outs across all currencies, ensuring that no bank receives a currency until CLS has confirmed receipt of all currencies that bank owes.

The simultaneity is the key. If a bank cannot fund its pay-in obligation in one currency, CLS does not release any payments to or from that bank in any currency. The defaulting bank's trades are unwound, but no other participant suffers a principal loss. The risk is contained.

CLS membership is tiered. Settlement members hold accounts at CLS and settle directly. Third-party members settle through a settlement member but benefit from the same PvP protection. As of 2026, CLS settles an average of $6.5 trillion per day, covering roughly half of global FX settlement volumes.

CLS does not eliminate all FX settlement risk. Transactions in currencies outside the CLS network, trades between non-members, and certain exotic products still settle bilaterally. But for the currencies and participants it covers, CLS has effectively closed the Herstatt gap.

FX Settlement Risk Management Best Practices

Even with infrastructure like CLS, banks and corporations must manage residual settlement risk through operational discipline and sound risk governance.

Counterparty due diligence begins before the first trade. Credit teams assess the financial strength, operational capability, and settlement practices of potential counterparties. Due diligence includes reviewing audited financials, understanding the counterparty's own settlement risk controls, and confirming that the counterparty uses CLS or other risk-mitigation mechanisms where available.

Limit setting translates credit assessments into quantitative constraints. Banks establish settlement limits that cap the peak intraday exposure to each counterparty. Limits are lower for counterparties that do not use CLS, for currencies that settle in distant time zones, and for counterparties with weaker credit ratings. Limits are reviewed regularly and adjusted when credit conditions change.

Author: Olivia Kensington;

Source: martinskikulis.com

Use of central counterparties and CLS should be mandatory policy, not optional. For currencies covered by CLS, banks should route all eligible trades through the system. For securities, DVP settlement through a central securities depository should be standard. Exceptions require senior approval and additional risk controls.

Operational controls govern the timing and irrevocability of payments. Payment instructions should be released only after confirming that the counterparty has the operational capability to settle. Banks use real-time monitoring systems to track the status of incoming and outgoing payments throughout the settlement window. If an expected payment does not arrive on schedule, escalation procedures halt further outgoing payments to that counterparty until the issue is resolved.

Monitoring tools provide intraday visibility into settlement exposures. Banks aggregate exposures across all asset classes and counterparties, comparing real-time positions against limits. Dashboards flag approaching limits, late payments, and counterparties for which settlement volumes have increased sharply. Risk committees review settlement exposures daily, and any breach of limits triggers immediate investigation.

Corporations face similar challenges, particularly those with large FX hedging programs. A multinational company might execute dozens of FX forwards each month with multiple bank counterparties. Settlement dates cluster around month-end, when the company converts foreign revenues to its home currency. Corporate treasurers should diversify settlement counterparties, insist on CLS settlement where possible, and maintain backup liquidity to cover settlement fails.

Settlement risk is unique in that it combines large exposures with very short time horizons. The fact that the probability of loss is low does not mean the risk is small—when settlement failures occur, the losses can be total and immediate. This is why payment-versus-payment systems like CLS are not merely convenient; they are essential to the stability of the global financial system

— Benoît Cœuré

FAQ

What is the main difference between settlement risk and credit risk?

Settlement risk is a specific type of credit risk that arises during the settlement window of a transaction, when one party has made an irrevocable payment but has not yet received the offsetting asset or currency. Credit risk is broader and covers any situation where a counterparty might fail to meet an obligation. Settlement risk involves principal-at-risk exposure—the full notional amount—while other forms of credit risk often involve only the mark-to-market value of a position.

Can settlement risk be completely eliminated?

No, but it can be reduced to very low levels. Payment-versus-payment systems like CLS eliminate principal risk for transactions within their network, but they do not cover all currencies or all market participants. Trades in non-CLS currencies, exotic instruments, and transactions with non-members still carry settlement risk. Operational failures, cyberattacks, and force majeure events can also disrupt settlement systems, creating residual risk even in well-controlled environments.

What happens if one party fails during the settlement process?

If a counterparty fails after receiving payment but before delivering the offsetting currency or asset, the non-defaulting party loses the full amount it paid. It becomes an unsecured creditor in the bankruptcy or resolution process, with uncertain recovery prospects. In a CLS settlement, the system unwinds all trades involving the failed party without executing any payments, so other participants do not suffer principal losses. In bilateral settlement, the non-defaulting party must file a claim and wait for the resolution process to conclude, which can take months or years.

Is settlement risk higher in certain currency pairs?

Yes. Currency pairs involving time zones far apart create longer settlement windows and higher risk. For example, a trade pairing an Asian currency with a Latin American currency might involve a settlement gap of 12 hours or more. Pairs involving currencies not covered by CLS carry higher risk because they must settle bilaterally. Emerging-market currencies with less robust payment infrastructure or higher counterparty default risk also present elevated settlement exposure.

How does settlement netting reduce exposure?

Settlement netting reduces the gross value of payments between counterparties to a net amount. If two parties have multiple trades settling on the same day, netting calculates the net amount owed in each currency and settles only that figure. This reduces the notional principal at risk. For example, if Party A owes Party B $100 million on one trade and Party B owes Party A $90 million on another, netting reduces the settlement to a single $10 million payment. The settlement risk falls from $100 million to $10 million.

Do retail forex traders face settlement risk?

Retail forex traders using margin accounts with brokers generally do not face settlement risk in the same way institutional participants do. Retail FX platforms typically operate on a contract-for-difference (CFD) or margin-trading model, where the trader does not take physical delivery of currencies. The broker acts as counterparty and nets all positions internally. The trader faces counterparty credit risk—the risk that the broker fails and cannot return the trader's margin—but not settlement risk in the traditional sense. However, if a retail trader executes a physical delivery FX transaction through a bank, settlement risk does apply.

Settlement risk occupies a unique and dangerous position in the landscape of financial risk. It compresses large principal exposures into brief windows measured in hours, not days or months. The 1974 Herstatt collapse demonstrated that settlement failures can cascade across borders and destabilize markets. The response—decades of infrastructure investment, the creation of CLS Bank, and the adoption of delivery-versus-payment and payment-versus-payment mechanisms—has substantially reduced the risk, but not eliminated it.

Foreign exchange markets remain the epicenter of settlement risk because currencies settle in different jurisdictions, on different systems, at different times. Time zones create unavoidable gaps, and the sheer scale of FX turnover means that even a small failure can generate losses in the hundreds of millions or billions of dollars.

Effective settlement risk management requires a combination of infrastructure, policy, and discipline. Institutions should route all eligible transactions through CLS or equivalent PvP systems, enforce strict counterparty limits, and maintain real-time monitoring of settlement exposures. Corporate treasurers and fund managers must understand the settlement mechanics of their FX transactions and insist on risk-mitigation tools as a condition of trading.

The difference between settlement risk and credit risk is not academic. Credit risk allows for recovery and restructuring. Settlement risk often results in total loss. The brevity of the exposure does not make it less dangerous—it makes it more acute and harder to manage. As cross-border finance continues to grow, and as new currencies and digital assets enter the settlement ecosystem, the lessons of Herstatt remain as relevant in 2026 as they were half a century ago.

Unsystematic risk represents investment uncertainty tied to specific companies or assets rather than broad market forces. Unlike systematic risks affecting all securities, firm-specific risks can be substantially reduced through proper diversification across 20-30 uncorrelated positions

Markets don't just move—they accelerate, decelerate, and shift gears. Volatility risk is the danger that unexpected changes in price swing intensity will damage your positions. Unlike directional risk, it strikes when market pace changes, hurting options traders, currency speculators, and leveraged investors alike

Volatility clustering describes how large price changes tend to follow large changes, and calm periods extend—one of the most consistent patterns in financial markets. Understanding this phenomenon transforms risk management and trading strategy across forex, equities, and other assets

Systematic risk affects entire markets simultaneously—no diversification can eliminate it. Through concrete examples from interest rate changes to geopolitical events, understand how market-wide forces impact portfolios and learn practical measurement and management strategies using beta and asset allocation

The content on this website is provided for general informational and educational purposes only. It is intended to explain concepts related to Forex (FX) trading, currency markets, leverage, hedging, and risk management.

All information on this website, including articles, guides, and examples, is presented for general educational purposes. Forex trading carries significant risk, and outcomes may vary depending on market conditions, leverage, and individual decisions.

This website does not provide financial, investment, or trading advice, and the information presented should not be used as a substitute for consultation with qualified financial professionals.

The website and its authors are not responsible for any errors or omissions, or for any outcomes resulting from decisions made based on the information provided on this website.